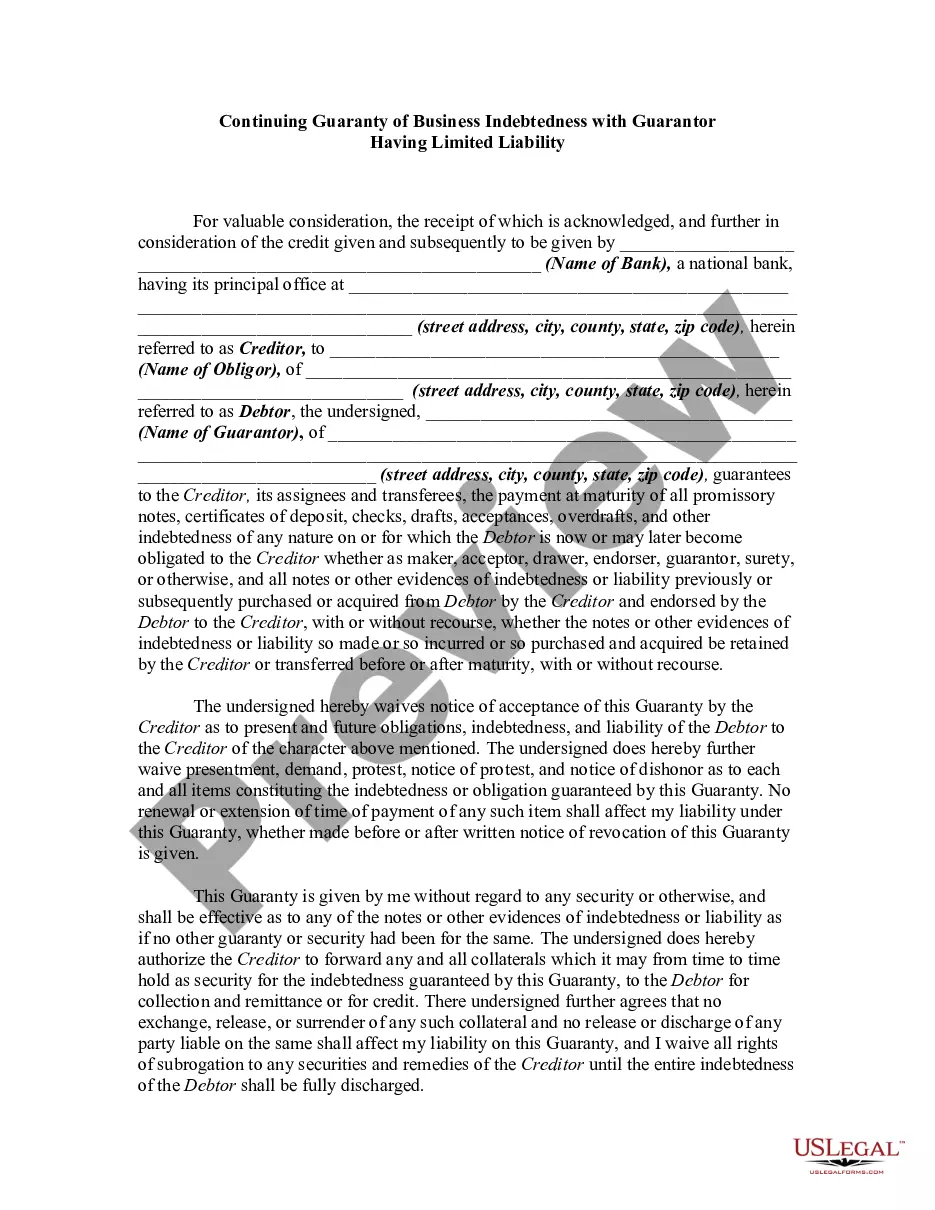

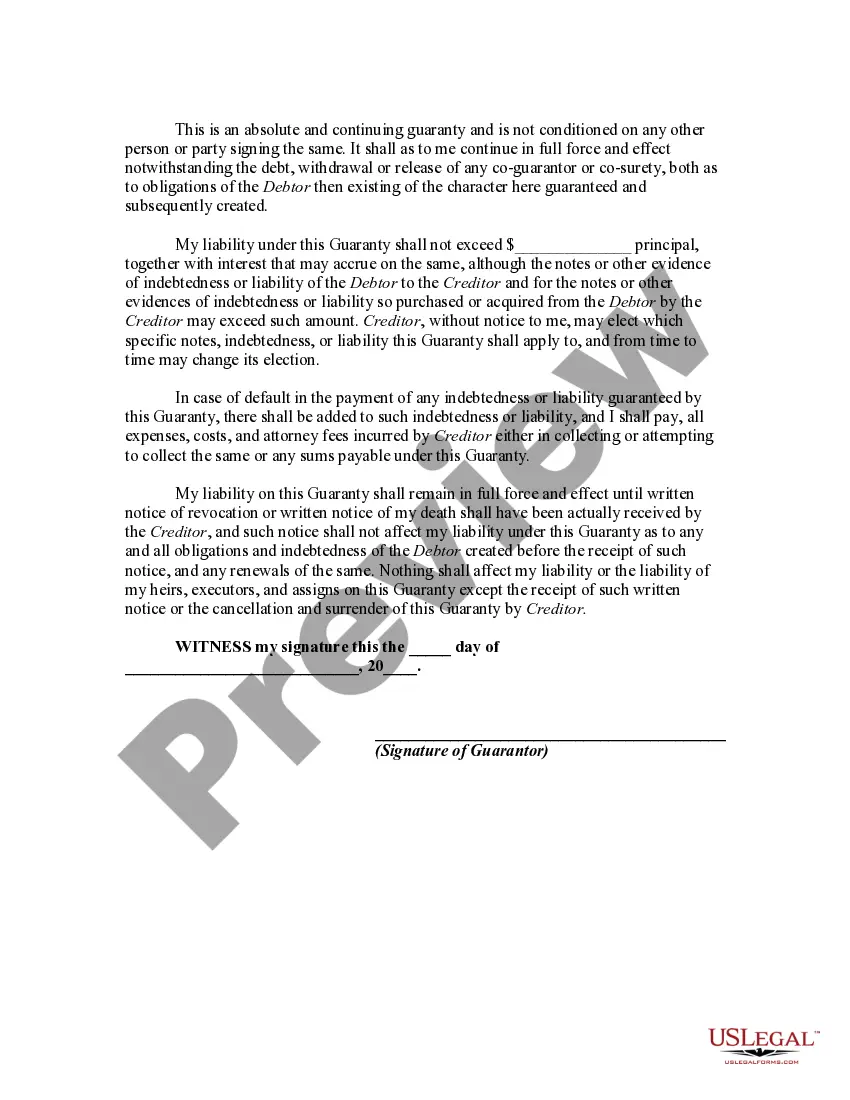

A guaranty is an undertaking on the part of one person (the guarantor) that is collateral to an obligation of another person (the debtor or obligor), and which binds the guarantor to performance of the obligation in the event of default by the debtor or obligor. A guaranty agreement is a type of contract. Thus, questions relating to such matters as validity, interpretation, and enforceability of guaranty agreements are decided in accordance with basic principles of contract law.

The New Jersey Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability is a legal document that outlines the responsibilities and obligations of a guarantor in relation to a business's outstanding debts. This type of guaranty is commonly used in the state of New Jersey to provide additional security for lenders, ensuring that business debts will be repaid even if the business becomes insolvent or struggles financially. The primary purpose of this type of guaranty is to grant the lender the right to pursue the guarantor's personal assets or resources in case the business fails to satisfy its debts. By agreeing to be a limited liability guarantor, individuals can safeguard their personal assets and minimize potential financial risks associated with business debts. There are several variations of the New Jersey Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability, including: 1. Full Recourse Guarantee: In this scenario, the guarantor is held fully responsible for the entire outstanding debt amount if the business fails to fulfill its obligations. The lender has the right to seek compensation from the guarantor's personal assets without any limitation. 2. Limited Recourse Guarantee: With this type of guaranty, the guarantor's liability is restricted to a predetermined amount or percentage of the outstanding debt. The lender can pursue compensation only up to the specified limit, thereby protecting the guarantor's personal assets beyond that threshold. 3. Continuing Guaranty: This refers to a guaranty that extends beyond a single transaction or loan. It covers present and future business indebtedness, ensuring that the guarantor's liability remains in effect until released by the lender. 4. Unconditional Guaranty: An unconditional guaranty imposes no conditions or requirements on the lender regarding the enforcement of the guarantor's liabilities. Once the business fails to meet its obligations, the guarantor becomes immediately responsible for the debt. 5. Limited Liability Guaranty: This type of guaranty aims to shield the guarantor from complete liability by creating limitations on the lender's claim against the guarantor's personal assets. It helps protect the guarantor's financial interests while still offering some assurances to the lender. 6. Specific Performance Guaranty: In certain cases, a guarantor may agree to provide specific assets or collateral to satisfy the business's debts in case of default. This additional level of security ensures the lender has a defined recourse in the event of non-payment by the business. When considering a New Jersey Continuing Guaranty of Business Indebtedness with Guarantor Having Limited Liability, it is crucial to consult with legal professionals experienced in business law to fully understand the implications and requirements imposed by this type of legal agreement.