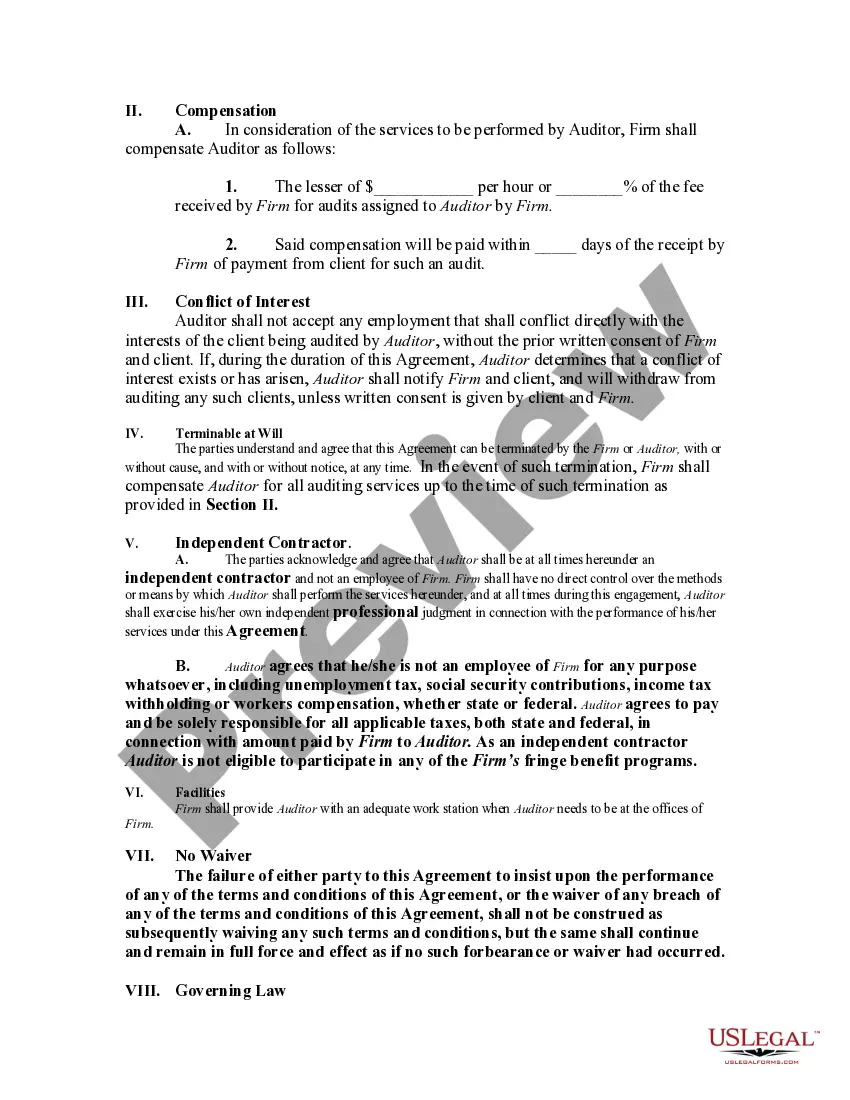

Although no definite rule exists for determining whether one is an independent contractor or an employee, certain indicia of the status of an independent contractor are recognized, and the insertion of provisions embodying these indicia in the contract will help to insure that the relationship reflects the intention of the parties. These indicia generally relate to the basic issue of control. The general test of what constitutes an independent contractor relationship involves which party has the right to direct what is to be done, and how and when. Another important test involves the method of payment of the contractor.

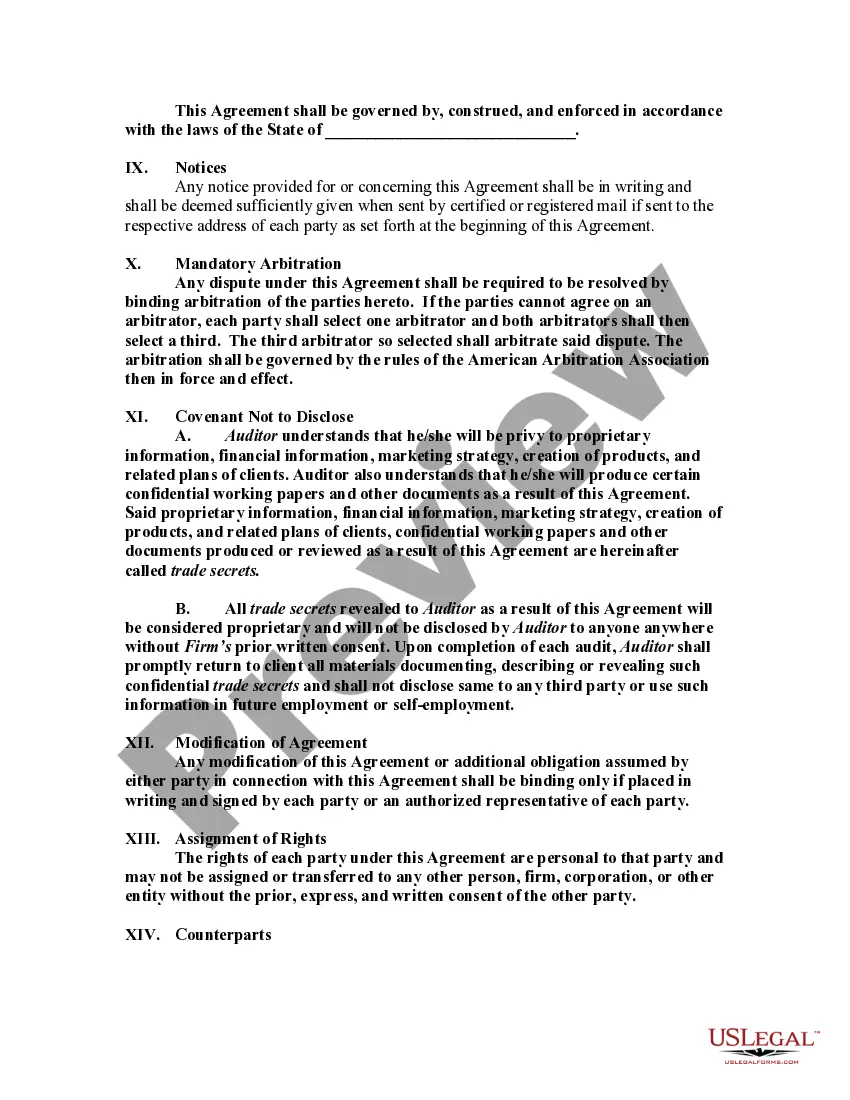

New Jersey Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: Keywords: New Jersey, agreement, accounting firm, employ, auditor, self-employed, independent contractor. 1. Introduction to the New Jersey Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: In the state of New Jersey, accounting firms often enter into agreements to employ auditors as self-employed independent contractors. This legally binding document outlines the terms and conditions governing the working relationship between the accounting firm and the auditor. By entering into this agreement, both parties acknowledge and agree to abide by the laws and regulations of New Jersey pertaining to self-employment and independent contractors. 2. General Provisions: This section of the agreement outlines the basic details of the contract, including the effective date, duration, and termination procedures. It also specifies that the auditor will work as a self-employed independent contractor, not as an employee of the accounting firm, and will be responsible for their own taxes, benefits, and insurance. 3. Scope of Work and Services: The agreement details the specific responsibilities and scope of work to be undertaken by the auditor. It may include conducting financial audits, providing accounting advice, preparing financial statements, and other related tasks as agreed upon by both parties. The agreement outlines the expected deliverables, timelines, and any constraints on the services to be performed. 4. Compensation and Payment Terms: This section covers the compensation structure for the auditor's services. It specifies the hourly rate, project-based fees, or any other agreed-upon payment model. Additionally, the agreement clarifies how and when payments will be made, ensuring prompt and accurate remuneration to the auditor. 5. Confidentiality and Non-Disclosure: In this section, the agreement highlights the importance of maintaining confidentiality and non-disclosure regarding the accounting firm's sensitive information, trade secrets, and client data. Both parties agree to protect and not disclose any confidential information obtained through their working relationship. 6. Intellectual Property: If the auditor creates or contributes to any intellectual property during the course of their engagement, this section outlines the ownership rights and any licensing or usage agreements. It ensures that the accounting firm has the appropriate rights to utilize and protect any intellectual property resulting from the auditor's work. 7. Dispute Resolution and Arbitration: In case of any disputes arising from this agreement, a section on dispute resolution outlines the process to be followed, which may involve negotiation, mediation, or arbitration. This provision aims to resolve conflicts amicably, ensuring the smooth continuation of the working relationship. Types of New Jersey Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: 1. General New Jersey Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor. 2. Project-Specific New Jersey Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor. 3. Long-Term New Jersey Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor. Note: The actual names of the agreement types may vary based on the accounting firm's preferences or specific circumstances.New Jersey Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: Keywords: New Jersey, agreement, accounting firm, employ, auditor, self-employed, independent contractor. 1. Introduction to the New Jersey Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: In the state of New Jersey, accounting firms often enter into agreements to employ auditors as self-employed independent contractors. This legally binding document outlines the terms and conditions governing the working relationship between the accounting firm and the auditor. By entering into this agreement, both parties acknowledge and agree to abide by the laws and regulations of New Jersey pertaining to self-employment and independent contractors. 2. General Provisions: This section of the agreement outlines the basic details of the contract, including the effective date, duration, and termination procedures. It also specifies that the auditor will work as a self-employed independent contractor, not as an employee of the accounting firm, and will be responsible for their own taxes, benefits, and insurance. 3. Scope of Work and Services: The agreement details the specific responsibilities and scope of work to be undertaken by the auditor. It may include conducting financial audits, providing accounting advice, preparing financial statements, and other related tasks as agreed upon by both parties. The agreement outlines the expected deliverables, timelines, and any constraints on the services to be performed. 4. Compensation and Payment Terms: This section covers the compensation structure for the auditor's services. It specifies the hourly rate, project-based fees, or any other agreed-upon payment model. Additionally, the agreement clarifies how and when payments will be made, ensuring prompt and accurate remuneration to the auditor. 5. Confidentiality and Non-Disclosure: In this section, the agreement highlights the importance of maintaining confidentiality and non-disclosure regarding the accounting firm's sensitive information, trade secrets, and client data. Both parties agree to protect and not disclose any confidential information obtained through their working relationship. 6. Intellectual Property: If the auditor creates or contributes to any intellectual property during the course of their engagement, this section outlines the ownership rights and any licensing or usage agreements. It ensures that the accounting firm has the appropriate rights to utilize and protect any intellectual property resulting from the auditor's work. 7. Dispute Resolution and Arbitration: In case of any disputes arising from this agreement, a section on dispute resolution outlines the process to be followed, which may involve negotiation, mediation, or arbitration. This provision aims to resolve conflicts amicably, ensuring the smooth continuation of the working relationship. Types of New Jersey Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: 1. General New Jersey Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor. 2. Project-Specific New Jersey Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor. 3. Long-Term New Jersey Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor. Note: The actual names of the agreement types may vary based on the accounting firm's preferences or specific circumstances.