The Fair Credit Reporting Act (FCRA) is designed to help ensure that credit bureaus furnish correct and complete information to businesses to use when evaluating your application. Your rights include:

The right to receive a copy of your credit report. The copy of your report must contain all of the information in your file at the time of your request.

The right to know the name of anyone who received your credit report in the last year for most purposes or in the last two years for employment purposes.

Any company that denies your application must supply the name and address of the credit bureau they contacted, provided the denial was based on information given by the credit bureau.

The right to a free copy of your credit report when your application is denied because of information supplied by the credit bureau. Your request must be made within 60 days of receiving your denial notice.

If you contest the completeness or accuracy of information in your report, you should file a dispute with the credit bureau and with the company that furnished the information to the bureau. Both the credit bureau and the furnisher of information are legally obligated to investigate your dispute.

A right to add a summary explanation to your credit report if your dispute is not resolved to your satisfaction.

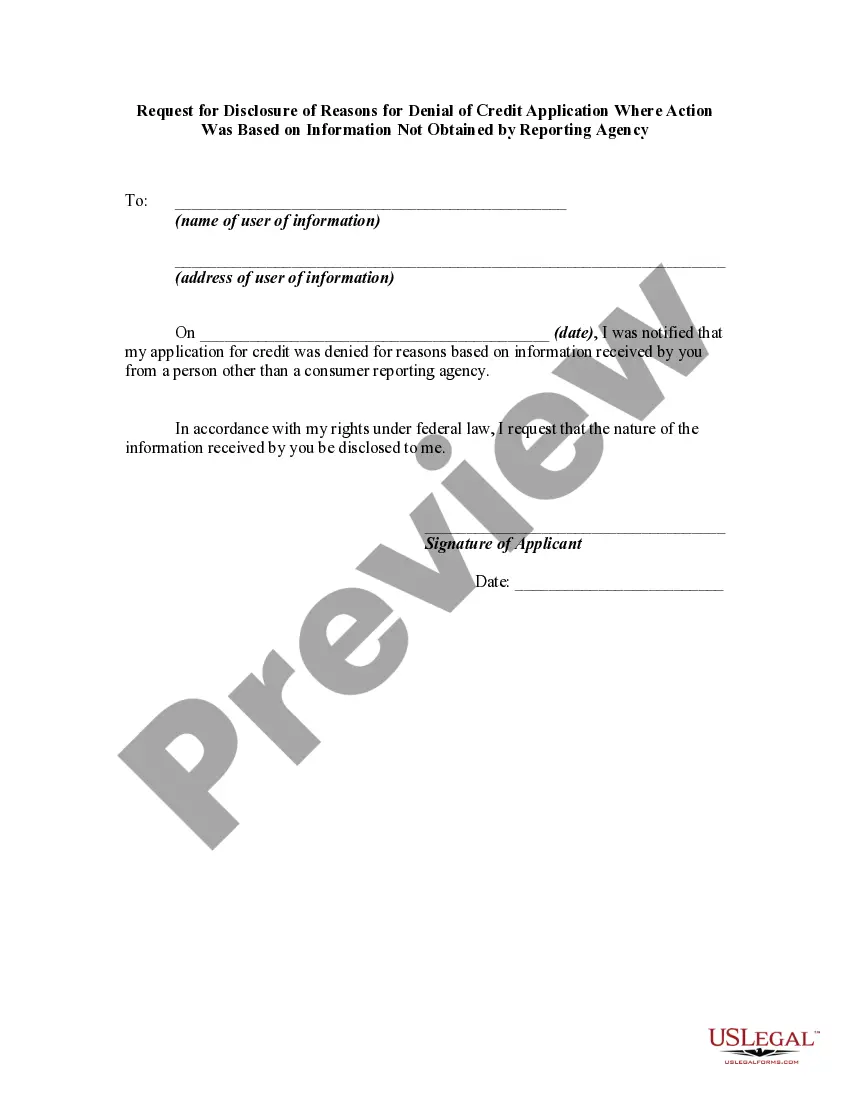

Keywords: New Jersey, request for disclosure, denial of credit application, reasons, action, information, not obtained, reporting agency, types Title: New Jersey Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency Introduction: The state of New Jersey allows individuals to request disclosure of the reasons behind the denial of their credit applications, particularly when the denial was based on information not obtained by the reporting agency. This article will provide a detailed description of the process, requirements, and potential types of New Jersey request for disclosure in such cases. 1. Understanding the New Jersey Request for Disclosure: — In New Jersey, consumers have the right to know the reasons behind the denial of their credit application. — This particular request for disclosure focuses on situations where the denial was based on information not obtained by the reporting agency. — The goal is to ensure transparency and fairness in the credit evaluation process. 2. Process for Requesting Disclosure: — To initiate the request, individuals need to obtain the denial notice from the creditor. — The request for disclosure must be made within 60 days of receiving the denial notice. — It is essential to gather all necessary information to support the request, such as copies of credit reports, application materials, and any relevant correspondence. 3. Required Information for the Request: The New Jersey request for disclosure should include the following details: — Personal information: Full name, address, contact information. — Denial notice: Attach a copy of the notice received from the creditor. — Supporting documents: Include relevant credit reports, application materials, and correspondence related to the credit application. 4. Submitting the Request: — The request for disclosure should be submitted in writing. — It is recommended to send the request via certified mail or use a delivery service that provides proof of delivery. — Keep a copy of the request, along with all supporting documents, for your records. 5. Possible Types of New Jersey Request for Disclosure: While the main focus is on denials based on information not obtained by the reporting agency, there can be variations of this request, such as: — Request for denial reasons based on outdated information. — Request for denial reasons due to identity theft concerns. — Request for denial reasons resulting from incorrect information provided by creditor. Conclusion: The New Jersey request for disclosure of reasons for denial of credit application, where the action was based on information not obtained by the reporting agency, serves as a vital tool for consumers to seek transparency in credit evaluation. By following the proper process and providing the necessary information, individuals can better understand the grounds on which their credit applications were denied and take appropriate actions to rectify any inaccuracies or discrepancies.