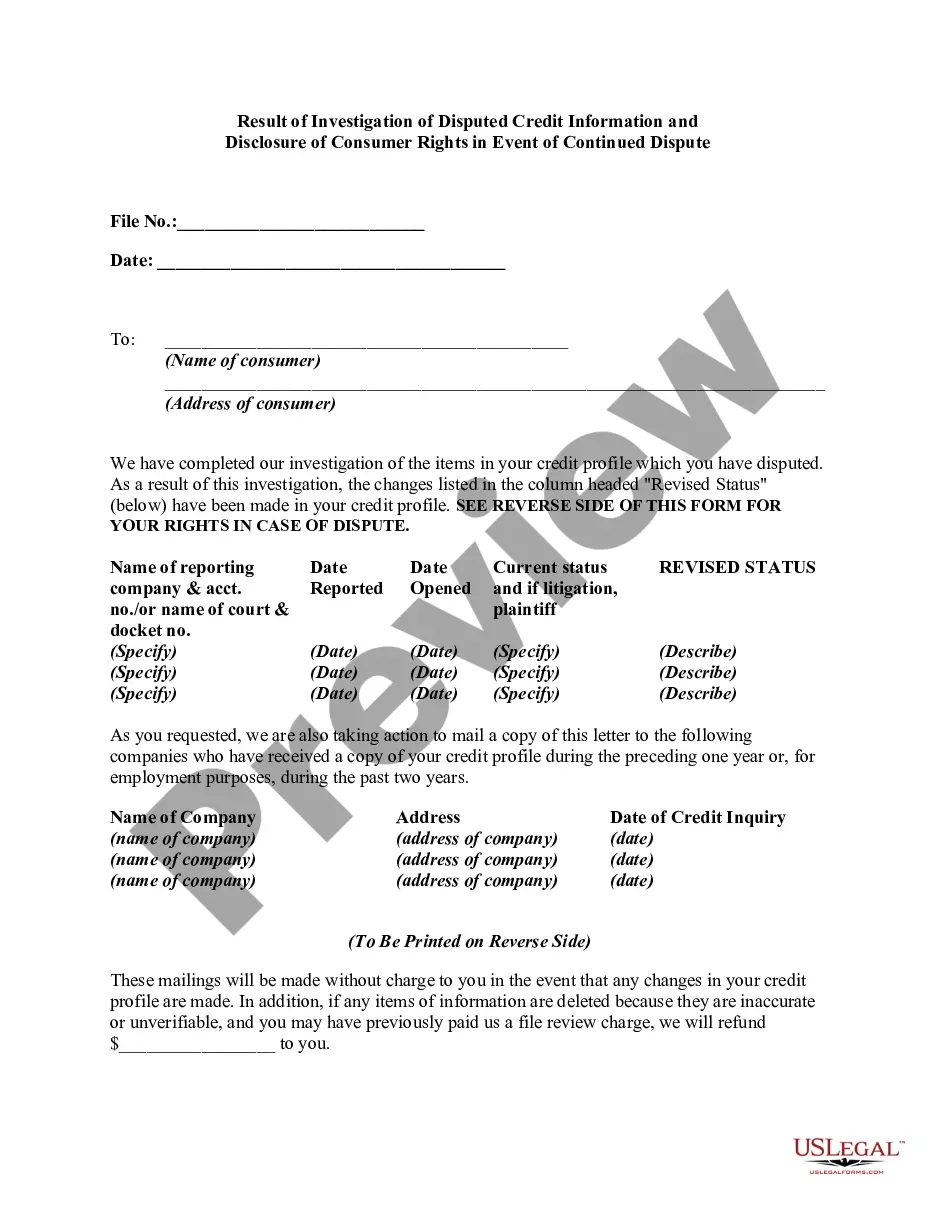

Under the Fair Credit Reporting Act, if a consumer disputes the completeness or accuracy of any item of information in the consumer's file, and the dispute is directly conveyed to the consumer reporting agency by the consumer, the reporting agency must, free of charge, conduct a reasonable reinvestigation to determine whether the disputed information is inaccurate, unless it has reasonable grounds to believe that the dispute is frivolous or irrelevant. If the information is erroneous, inaccurate, or can no longer be verified, the credit reporting agency must promptly correct or delete it and refrain from reporting the information in subsequent consumer reports.

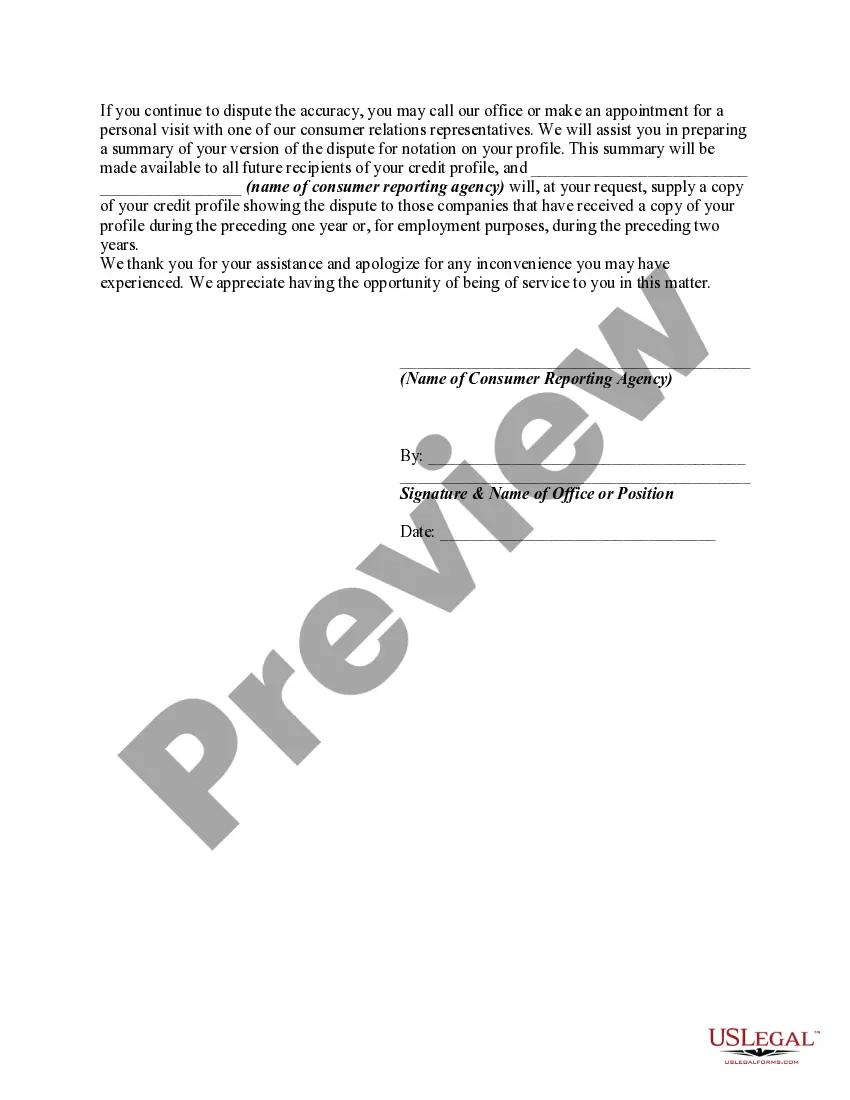

Following any deletion of information or notation as to disputed information, the agency, on request of the consumer, must furnish to certain persons either: (1) notification of the deletion; or (2) the consumer's statement of the dispute or the agency's summary of the statement. The consumer reporting agency must clearly and conspicuously disclose the consumer's rights to make such a request, such disclosure to be made at or prior to the time the information is deleted or the consumer's statement regarding the disputed information is received.

Title: Understanding the Result of Investigation of Disputed Credit Information in New Jersey: Disclosing Consumer Rights in Ongoing Disputes Introduction: In New Jersey, consumers have the right to dispute inaccurate or incomplete credit information on their credit reports. The investigation process conducted by credit bureaus and lenders plays a significant role in resolving these disputes and ensuring the accuracy of credit information. This article aims to provide a detailed description of the result of investigations into disputed credit information in New Jersey, while also addressing the disclosure of consumer rights in the event of a continued dispute. Keywords: New Jersey, result of investigation, disputed credit information, consumer rights, disclosure, ongoing disputes. 1. Investigation of Disputed Credit Information: When a consumer files a dispute regarding their credit information, the credit reporting agencies (Crash) initiate an investigation process. The Crash gather relevant documentation and reach out to the information provider (e.g., lenders, collection agencies) to verify the accuracy of the disputed information. 2. Resolution of Disputed Credit Information: Upon completion of the investigation, the Crash typically communicate the result to the consumer, often in writing. The results can be categorized into: — Verified: If the disputed credit information is found to be accurate, the result will reflect that the information has been verified during the investigation. This means that the credit bureaus will continue to report the information as shown on the consumer's credit report. — Deleted: If the disputed information is found to be inaccurate, incomplete, or unverifiable, the result will indicate that the information has been deleted from the consumer's credit report. This deletion helps ensure the accuracy of the credit information. — Updated: In some cases, the outcome of the investigation may lead to the correction or update of the disputed credit information. The result will reflect that the information has been modified to its accurate status, reflecting the resolution of the dispute. 3. Consumer Rights in the Event of Continued Dispute: If a consumer is not satisfied with the result of the investigation, they have rights outlined by federal law, including the Fair Credit Reporting Act (FCRA). These rights include: — Reinvestigation: Consumers can ask the Crash to conduct a reinvestigation of the disputed credit information if they find the initial investigation to be incomplete or inaccurate. — Free Credit Reports: Consumers are entitled to one free credit report annually from each of the three major Crash — Equifax, Experian, and TransUnion. This provides an opportunity to review their credit information regularly, ensuring accuracy and detecting potential errors. — Dispute Statement: If a consumer disagrees with the result of the investigation, they have the right to request the inclusion of a statement in their credit file disputing the accuracy of specific credit information. This statement is typically limited to 100 to 200 words and will be visible to future credit report users. Conclusion: In New Jersey, the result of an investigation into disputed credit information plays a crucial role in determining the accuracy of a consumer's credit report. It is vital for consumers to understand their rights during ongoing disputes and the steps they can take to ensure the accuracy of their credit information. By leveraging their legal rights, consumers can protect themselves and maintain the integrity of their credit history.