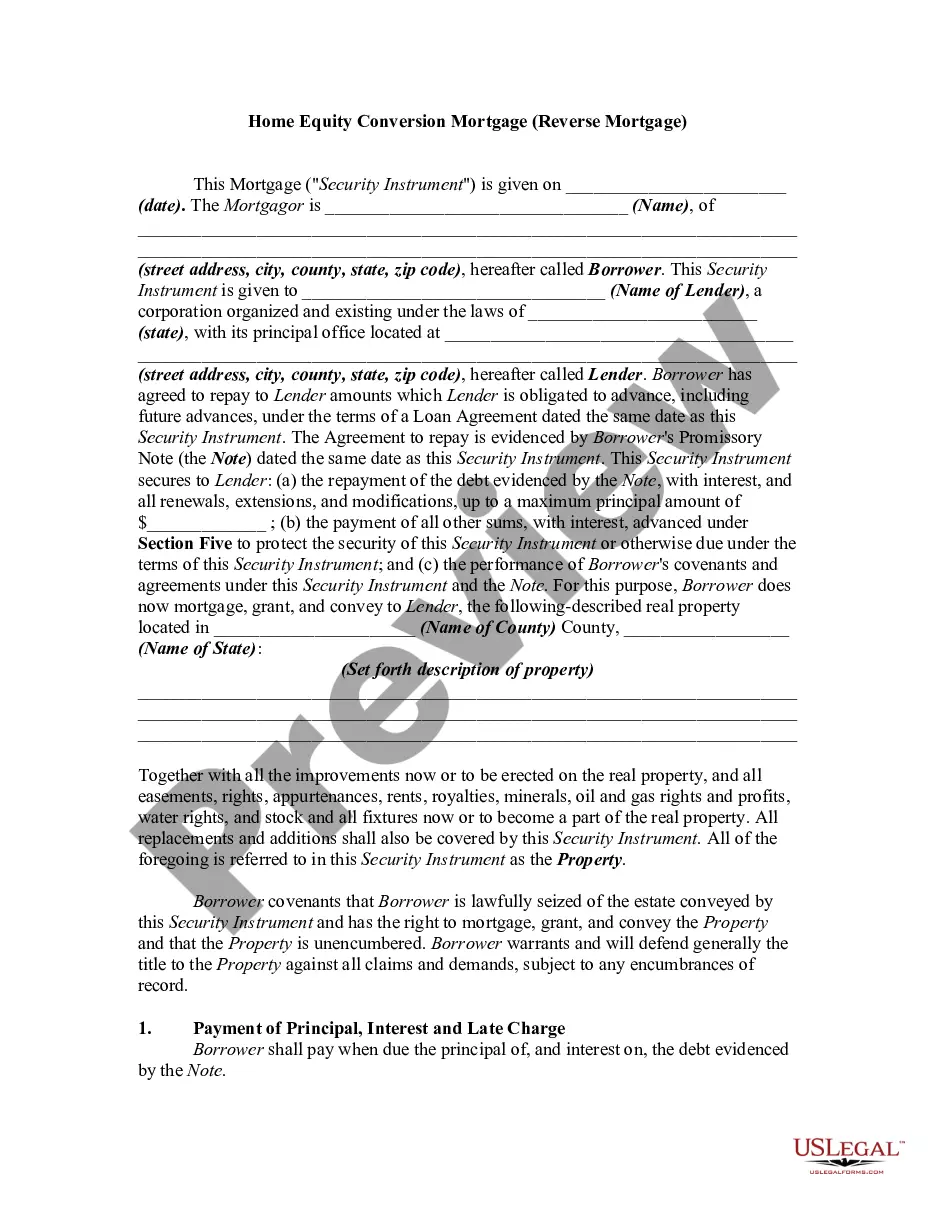

A reverse mortgage is a loan from the U.S. Government for 50% to 75% of the value of a home owned by a homeowner aged 62 and older. Instead of making monthly payments to a lender, as with a regular mortgage, a lender makes payments to the homeowner. The funds from a reverse mortgage are tax-free. The loan doesn't have to be repaid in the homeowner's lifetime, however, when the homeowner dies, the money received plus approximately 4% interest is repaid by their estate. The loan is repaid when the homeowner ceases to occupy the home as a principal residence, due to the homeowner (the last remaining spouse, in cases of couples) passing away, selling the home, or permanently moving out.

A Home Equity Conversion Mortgage (HELM), more commonly known as a reverse mortgage, is a financial product available to homeowners in New Jersey who are aged 62 or older. It allows eligible homeowners to convert a portion of their home equity into tax-free cash without the need to sell or move out of their home. In New Jersey, there are several types of Home Equity Conversion Mortgages that homeowners can consider: 1. Standard Reverse Mortgage: This is the most common type of HELM in New Jersey. Homeowners can borrow against their home equity, either as a lump sum, a line of credit, fixed monthly payments, or a combination of these options. 2. Home Purchase Reverse Mortgage: This type of HELM is designed for seniors who want to purchase a new home. It allows eligible homeowners to use a reverse mortgage to finance the purchase of a new primary residence, while still benefiting from no monthly mortgage payments. 3. HELM for Purchase (H4P): Similar to the home purchase reverse mortgage, this option specifically caters to those looking to downsize or move to a different home while utilizing a reverse mortgage. This enables homeowners to buy a new home without needing to pay a large down payment from their own savings. 4. HELM Line of Credit: Homeowners in New Jersey can also opt for a reverse mortgage line of credit, which allows them to access funds as needed. The unused portion of the line of credit can also grow over time, providing additional financial security. 5. HELM Refinance: This option enables homeowners with an existing mortgage to pay off their traditional mortgage using a reverse mortgage. This allows them to eliminate monthly mortgage payments and access additional cash. New Jersey homeowners considering a Home Equity Conversion Mortgage should be aware of a few key keywords and concepts in order to make informed decisions. These keywords include: — Home equity: The market value of a homeowner's property minus any outstanding mortgage balance. — Reverse mortgage counseling: Seniors applying for a reverse mortgage are typically required to undergo counseling by an approved counseling agency. This counseling session provides important information about the loan terms, costs, and potential implications. — Non-recourse loan: A reverse mortgage is a non-recourse loan, meaning that the homeowner or their heirs will never owe more than the appraised value of the home when it is sold. — Principal limit: The maximum amount of funds that a homeowner can receive from a reverse mortgage, which is determined based on factors such as the homeowner's age, the home's value, and current interest rates. — Loan origination fee: A fee charged by lenders to cover the administrative costs associated with originating a reverse mortgage. It is usually a percentage of the loan amount. — Mortgage insurance premium (MIP): A fee required for all Helms, which provides insurance protection to the lender against potential loan losses. — FHA-insured: Reverse mortgages in New Jersey are backed by the Federal Housing Administration (FHA), which offers additional consumer protections and ensures that lenders are compliant with applicable regulations. By understanding these keywords and the different types of Home Equity Conversion Mortgages available in New Jersey, homeowners can make informed decisions about their financial future and take advantage of the benefits this flexible financial product offers.A Home Equity Conversion Mortgage (HELM), more commonly known as a reverse mortgage, is a financial product available to homeowners in New Jersey who are aged 62 or older. It allows eligible homeowners to convert a portion of their home equity into tax-free cash without the need to sell or move out of their home. In New Jersey, there are several types of Home Equity Conversion Mortgages that homeowners can consider: 1. Standard Reverse Mortgage: This is the most common type of HELM in New Jersey. Homeowners can borrow against their home equity, either as a lump sum, a line of credit, fixed monthly payments, or a combination of these options. 2. Home Purchase Reverse Mortgage: This type of HELM is designed for seniors who want to purchase a new home. It allows eligible homeowners to use a reverse mortgage to finance the purchase of a new primary residence, while still benefiting from no monthly mortgage payments. 3. HELM for Purchase (H4P): Similar to the home purchase reverse mortgage, this option specifically caters to those looking to downsize or move to a different home while utilizing a reverse mortgage. This enables homeowners to buy a new home without needing to pay a large down payment from their own savings. 4. HELM Line of Credit: Homeowners in New Jersey can also opt for a reverse mortgage line of credit, which allows them to access funds as needed. The unused portion of the line of credit can also grow over time, providing additional financial security. 5. HELM Refinance: This option enables homeowners with an existing mortgage to pay off their traditional mortgage using a reverse mortgage. This allows them to eliminate monthly mortgage payments and access additional cash. New Jersey homeowners considering a Home Equity Conversion Mortgage should be aware of a few key keywords and concepts in order to make informed decisions. These keywords include: — Home equity: The market value of a homeowner's property minus any outstanding mortgage balance. — Reverse mortgage counseling: Seniors applying for a reverse mortgage are typically required to undergo counseling by an approved counseling agency. This counseling session provides important information about the loan terms, costs, and potential implications. — Non-recourse loan: A reverse mortgage is a non-recourse loan, meaning that the homeowner or their heirs will never owe more than the appraised value of the home when it is sold. — Principal limit: The maximum amount of funds that a homeowner can receive from a reverse mortgage, which is determined based on factors such as the homeowner's age, the home's value, and current interest rates. — Loan origination fee: A fee charged by lenders to cover the administrative costs associated with originating a reverse mortgage. It is usually a percentage of the loan amount. — Mortgage insurance premium (MIP): A fee required for all Helms, which provides insurance protection to the lender against potential loan losses. — FHA-insured: Reverse mortgages in New Jersey are backed by the Federal Housing Administration (FHA), which offers additional consumer protections and ensures that lenders are compliant with applicable regulations. By understanding these keywords and the different types of Home Equity Conversion Mortgages available in New Jersey, homeowners can make informed decisions about their financial future and take advantage of the benefits this flexible financial product offers.