A secured transaction is created when a buyer or borrower (debtor) grants a seller or lender (creditor or secured party) a security interest in personal property (collateral). A security interest allows a creditor to repossess and sell the collateral if a debtor fails to pay a secured debt.

The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use or business purposes.

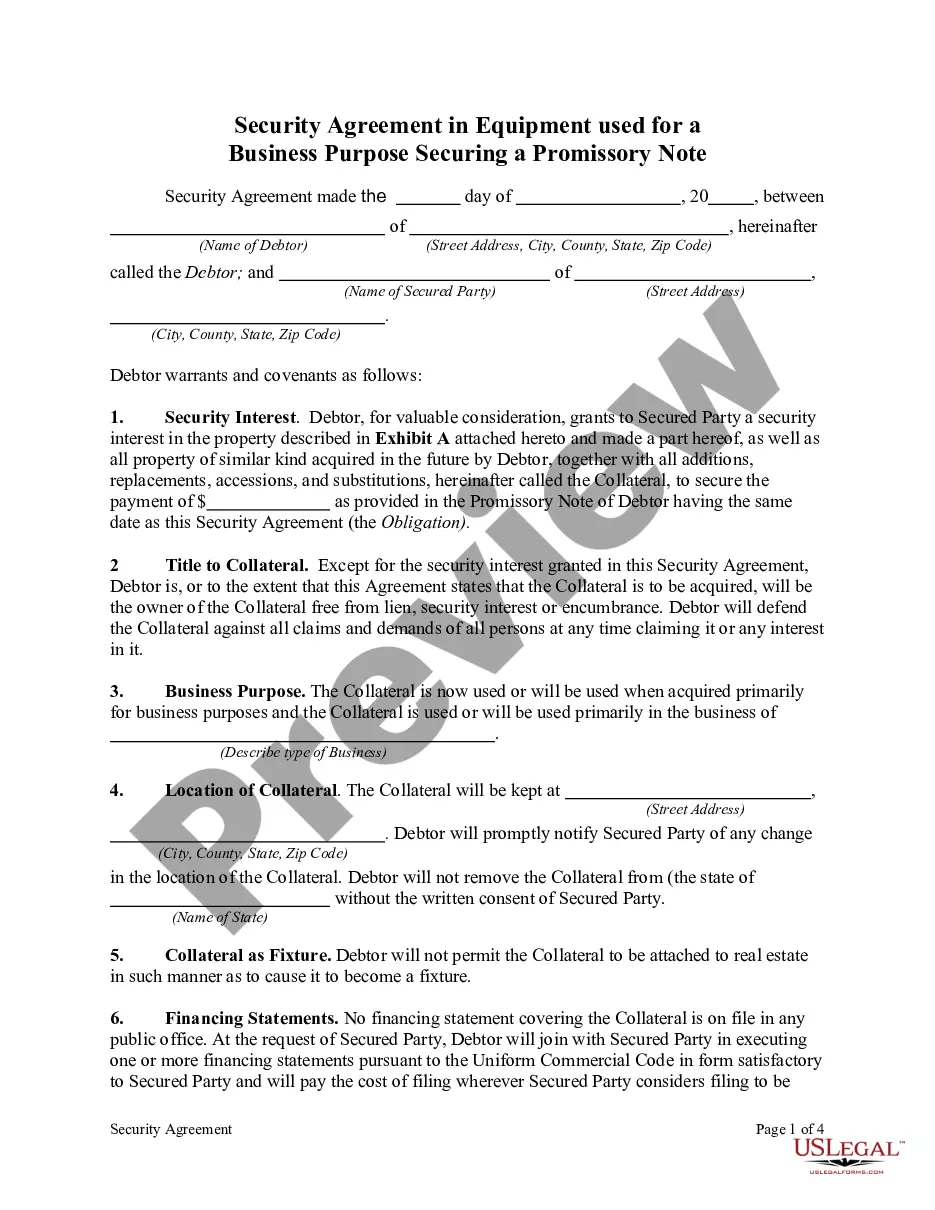

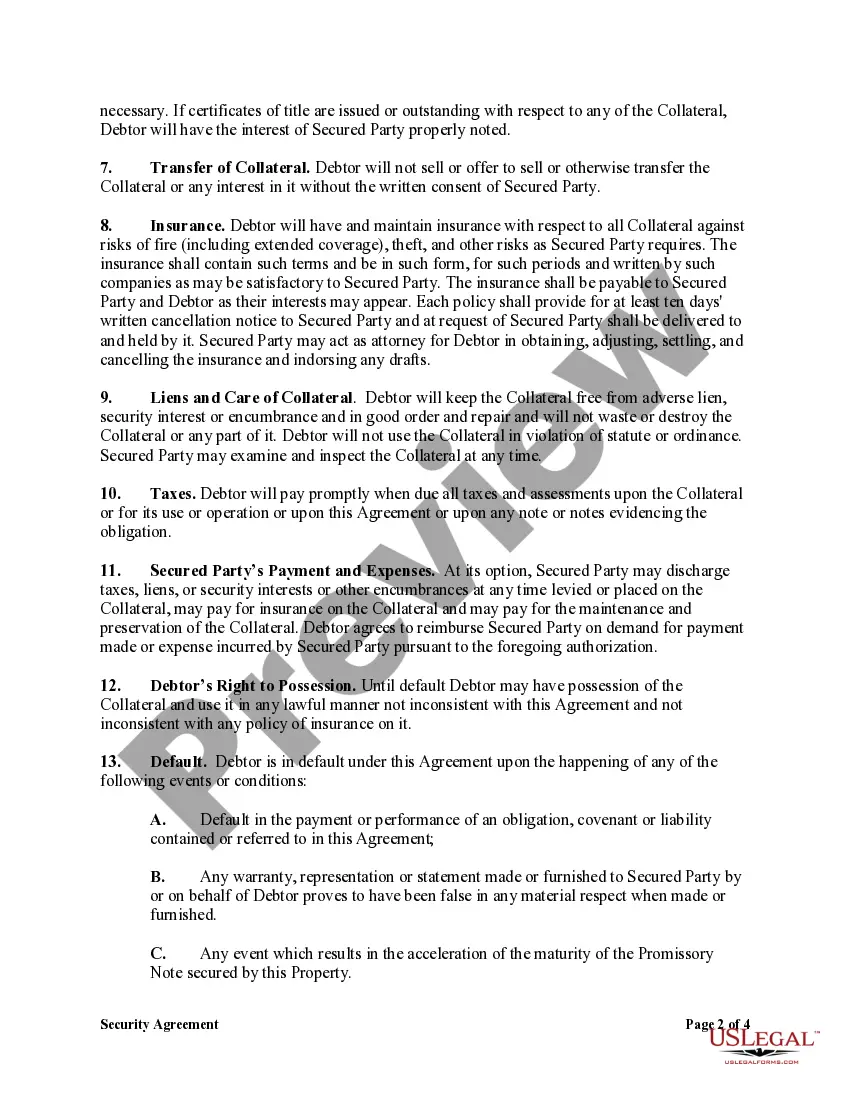

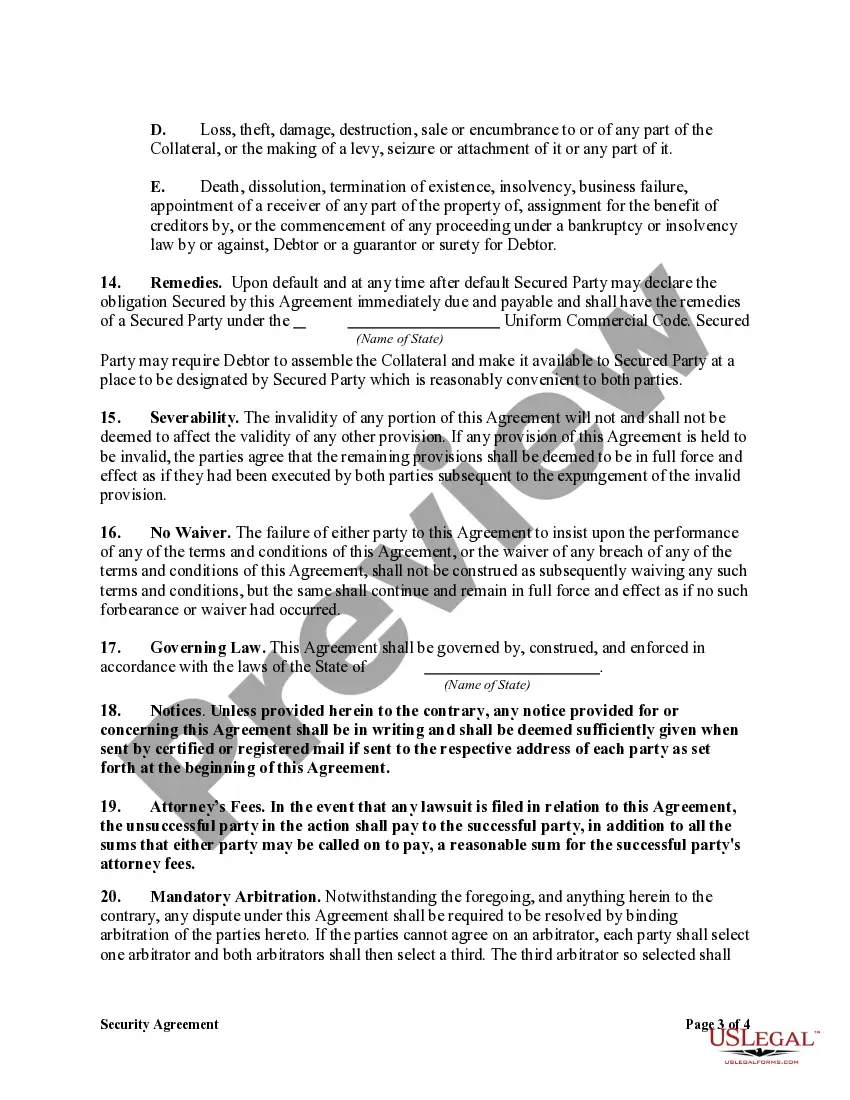

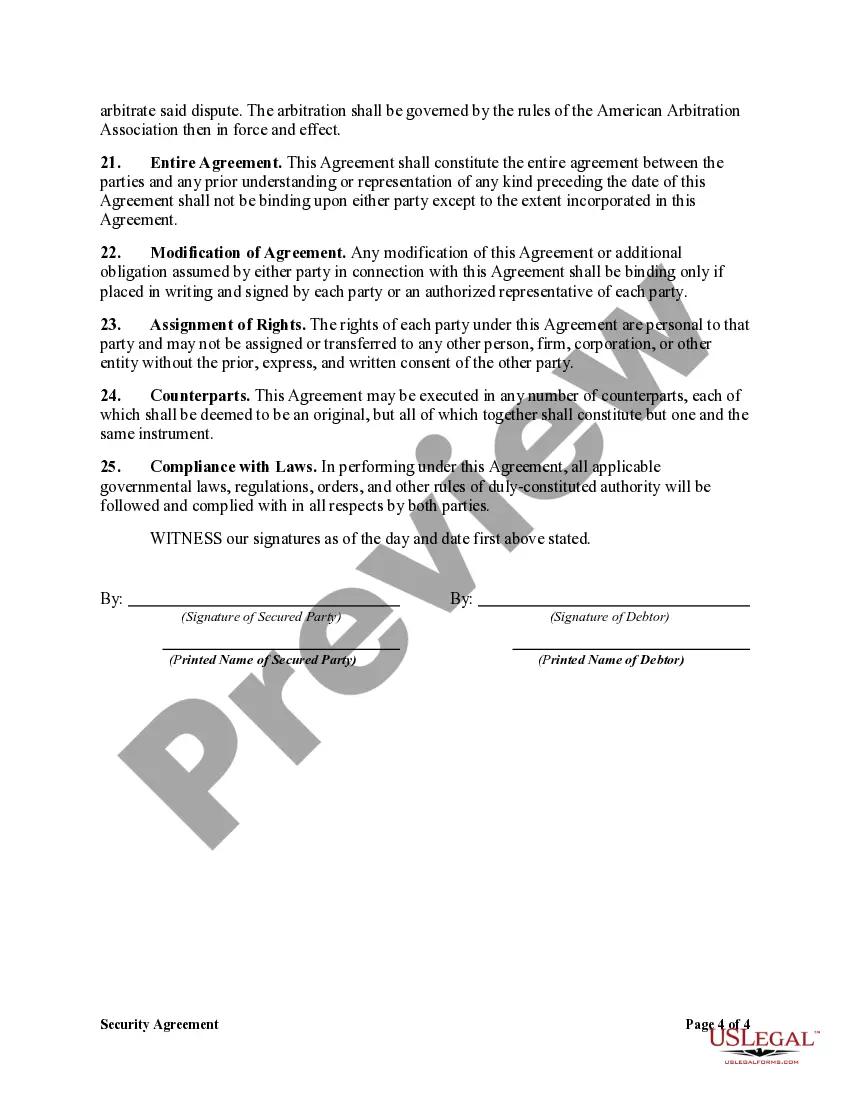

A New Jersey Security Agreement in Equipment for Business Purposes — Securing Promissory Note is a legal document that outlines an agreement between two parties involved in a loan transaction for business purposes. This agreement serves as collateral for the borrower's promissory note, providing the lender with security in case of default or non-payment. The New Jersey Security Agreement in Equipment for Business Purposes — Securing Promissory Note specifies the following essential details: 1. Parties Involved: It identifies the borrower (also known as the debtor) and the lender (also known as the secured party) involved in the agreement. Both parties must be mentioned clearly, along with their legal names and addresses. 2. Equipment Description: The agreement should list the specific equipment or assets that are being used as collateral. This includes a detailed description of each item, including make, model, serial numbers, and any unique identifiers. 3. Promissory Note: The security agreement references the promissory note and attaches it as an exhibit. The promissory note contains the terms and conditions of the loan, including the repayment schedule, interest rate, and any additional fees. 4. Security Interest: It establishes a security interest in the equipment, meaning that the lender has the right to take possession and sell the equipment if the borrower defaults on the loan. 5. Perfection of Security Interest: The agreement outlines the steps necessary to perfect the security interest, typically by filing a UCC-1 financing statement with the New Jersey Secretary of State. This ensures that the lender's claim on the equipment takes priority over other creditors. 6. Default and Remedies: The agreement describes the events and circumstances that constitute a default, such as non-payment or violation of any terms outlined in the promissory note. It also specifies the remedies available to the lender in case of default, which may include repossession, sale of the equipment, or legal action. Different types of New Jersey Security Agreements in Equipment for Business Purposes — Securing Promissory Note can vary based on the specific terms and conditions negotiated between the borrower and lender. The content may differ depending on factors such as the loan amount, repayment period, interest rate, and the nature of the business involved. In conclusion, a New Jersey Security Agreement in Equipment for Business Purposes — Securing Promissory Note is a vital legal document that protects the lender's interests by allowing the seizure and sale of equipment in case the borrower defaults. This agreement ensures that both parties have a clear understanding of their rights and responsibilities, promoting transparency and accountability in business loan transactions.A New Jersey Security Agreement in Equipment for Business Purposes — Securing Promissory Note is a legal document that outlines an agreement between two parties involved in a loan transaction for business purposes. This agreement serves as collateral for the borrower's promissory note, providing the lender with security in case of default or non-payment. The New Jersey Security Agreement in Equipment for Business Purposes — Securing Promissory Note specifies the following essential details: 1. Parties Involved: It identifies the borrower (also known as the debtor) and the lender (also known as the secured party) involved in the agreement. Both parties must be mentioned clearly, along with their legal names and addresses. 2. Equipment Description: The agreement should list the specific equipment or assets that are being used as collateral. This includes a detailed description of each item, including make, model, serial numbers, and any unique identifiers. 3. Promissory Note: The security agreement references the promissory note and attaches it as an exhibit. The promissory note contains the terms and conditions of the loan, including the repayment schedule, interest rate, and any additional fees. 4. Security Interest: It establishes a security interest in the equipment, meaning that the lender has the right to take possession and sell the equipment if the borrower defaults on the loan. 5. Perfection of Security Interest: The agreement outlines the steps necessary to perfect the security interest, typically by filing a UCC-1 financing statement with the New Jersey Secretary of State. This ensures that the lender's claim on the equipment takes priority over other creditors. 6. Default and Remedies: The agreement describes the events and circumstances that constitute a default, such as non-payment or violation of any terms outlined in the promissory note. It also specifies the remedies available to the lender in case of default, which may include repossession, sale of the equipment, or legal action. Different types of New Jersey Security Agreements in Equipment for Business Purposes — Securing Promissory Note can vary based on the specific terms and conditions negotiated between the borrower and lender. The content may differ depending on factors such as the loan amount, repayment period, interest rate, and the nature of the business involved. In conclusion, a New Jersey Security Agreement in Equipment for Business Purposes — Securing Promissory Note is a vital legal document that protects the lender's interests by allowing the seizure and sale of equipment in case the borrower defaults. This agreement ensures that both parties have a clear understanding of their rights and responsibilities, promoting transparency and accountability in business loan transactions.