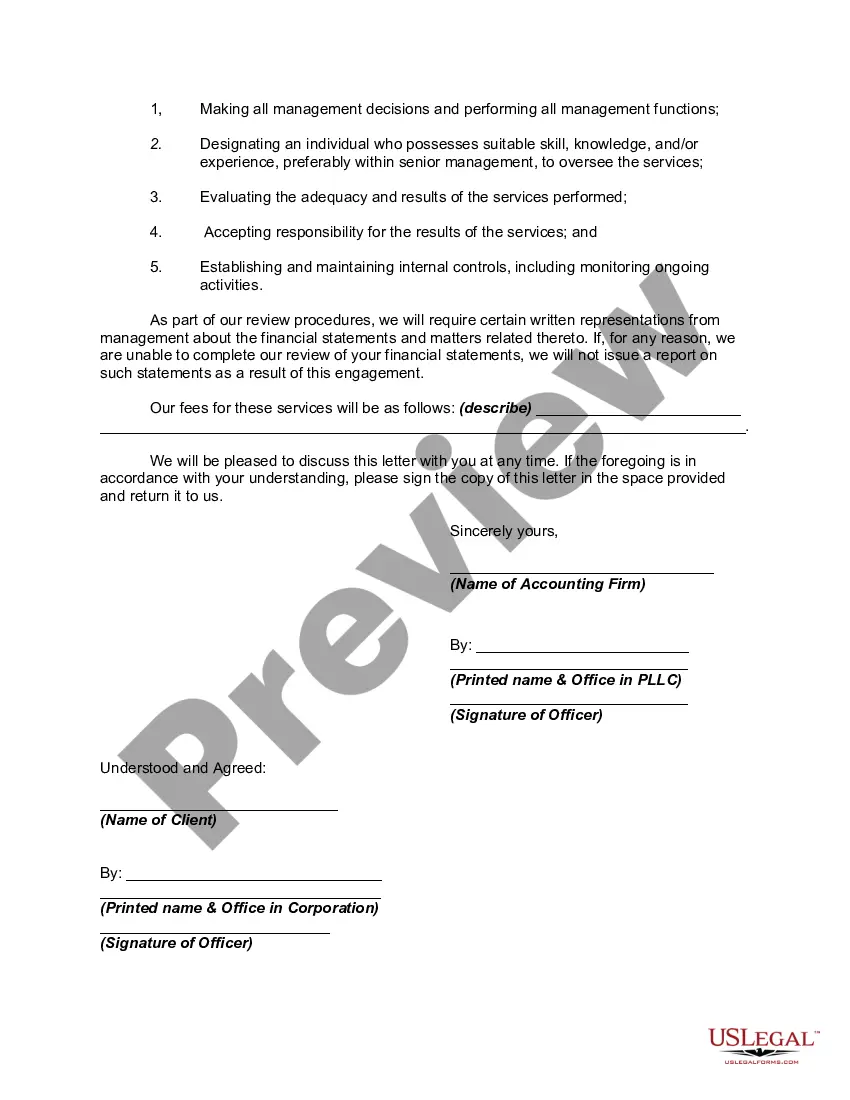

A limited review of financial statements is an audit restricted to an examination either for a limited period or of a limited part of the records. A review does not contemplate obtaining an understanding of the entity's internal control; assessing fraud risk; tests of accounting records by obtaining sufficient appropriate audit evidence through inspection, observation, confirmation, or the examination of source documents (for example, cancelled checks or bank images); and other procedures ordinarily performed in an audit. Accordingly, a review does not provide assurance that we will become aware of all significant matters that would be disclosed in an audit. Therefore, a review provides only limited assurance that there are no material modifications that should be made to the financial statements in order for the statements to be in conformity with generally accepted accounting principles.

The definition of nonattest services is very inclusive. It includes, for example, preparation of the client's depreciation schedule and preparation of journal entries even if management has approved the journal entries. I have confirmed these examples directly with the AICPA ethics division. The definition of nonattest services includes preparation of tax returns.

New Jersey Engagement Letter for Review of Financial Statements by Accounting Firm is a formal document that outlines the terms and conditions under which an accounting firm will conduct a review of financial statements for a client based in New Jersey. This letter serves as a contract between the client and the accounting firm, establishing the scope of the engagement, the responsibilities of both parties, and the fee arrangement. The engagement letter includes several key components to ensure a clear understanding of the review process. It outlines the purpose of the review, which is to provide limited assurance that the financial statements are free from material misstatements. It specifies that the review will be performed in accordance with the standards established by the American Institute of Certified Public Accountants (AICPA) and any additional requirements set by the New Jersey State Board of Accountancy. Furthermore, the engagement letter details the specific financial statements that will be reviewed, such as the balance sheet, income statement, statement of cash flows, and footnotes. It also specifies the period covered by the review and the expected timeline for completion. The letter will also mention the responsibilities of both the client and the accounting firm. The client is responsible for providing accurate and complete financial records, granting access to relevant personnel, and ensuring compliance with applicable laws and regulations. On the other hand, the accounting firm is responsible for conducting the review in an objective and professional manner, adhering to ethical guidelines, and exercising due care in performing their procedures. In terms of fees, the engagement letter outlines the basis for billing, such as hourly rates or a fixed fee arrangement. It also mentions any additional expenses that may be incurred during the review process, such as travel expenses or data analysis software costs. Depending on the specific circumstances, there may be different types of New Jersey Engagement Letters for Review of Financial Statements by Accounting Firm: 1. Standard Engagement Letter: This is the most common type of engagement letter, used for regular review engagements conducted by accounting firms in New Jersey. It covers the basic requirements and responsibilities involved in the review process. 2. Limited Scope Engagement Letter: In some cases, a client may request a review of specific elements of their financial statements, rather than a comprehensive review. In such instances, a limited scope engagement letter would be used to outline the specific areas to be reviewed and the associated scope limitations. 3. Agreed-Upon Procedures Engagement Letter: Instead of providing assurance on the financial statements as a whole, an accounting firm may be engaged to perform specified procedures on certain elements of the financial statements. This type of engagement letter identifies the specific procedures to be performed and the reporting format of the findings. In conclusion, the New Jersey Engagement Letter for Review of Financial Statements by Accounting Firm is a crucial document that clarifies the expectations, responsibilities, and scope of the review process between a client and an accounting firm. It ensures transparency, establishes a professional relationship, and provides a clear roadmap for the review engagement.