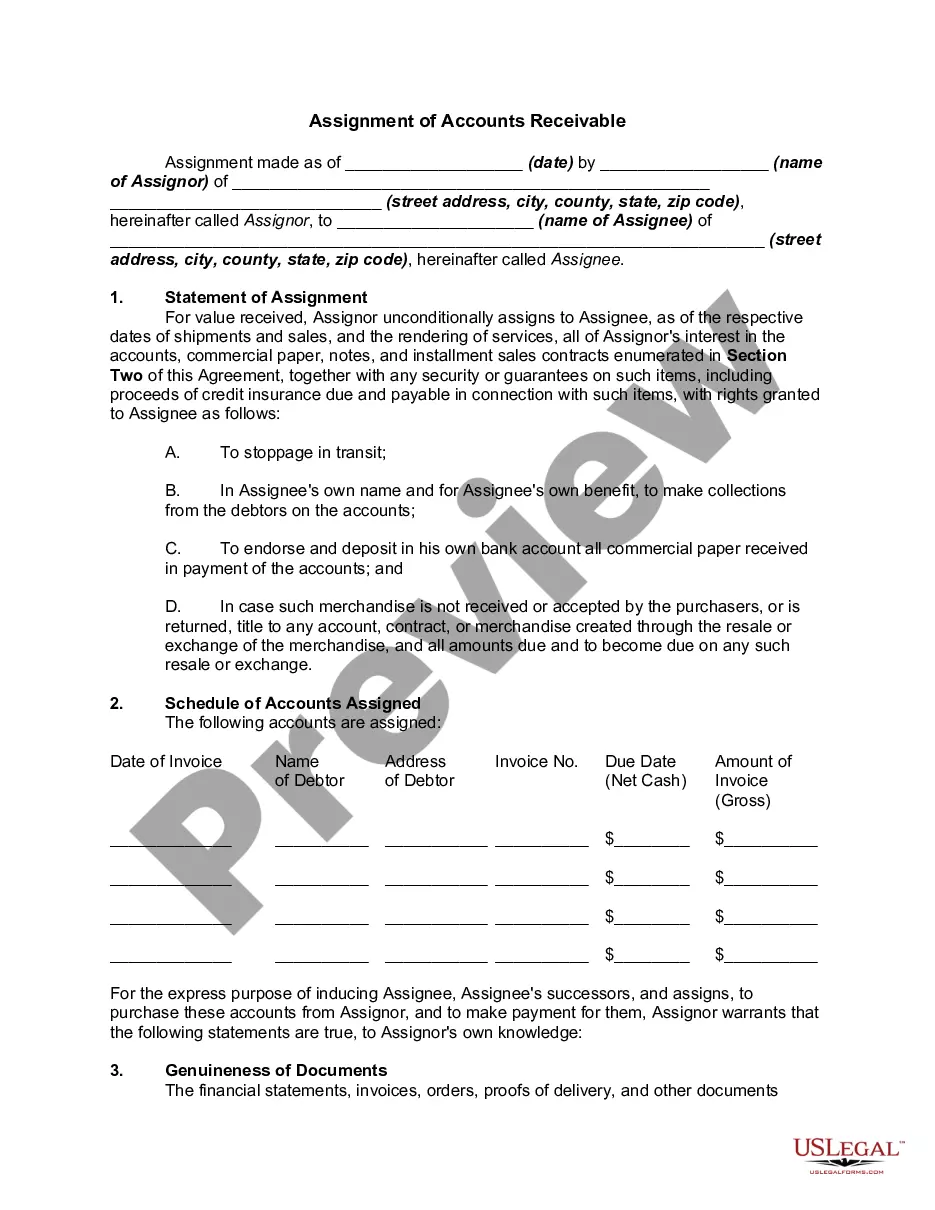

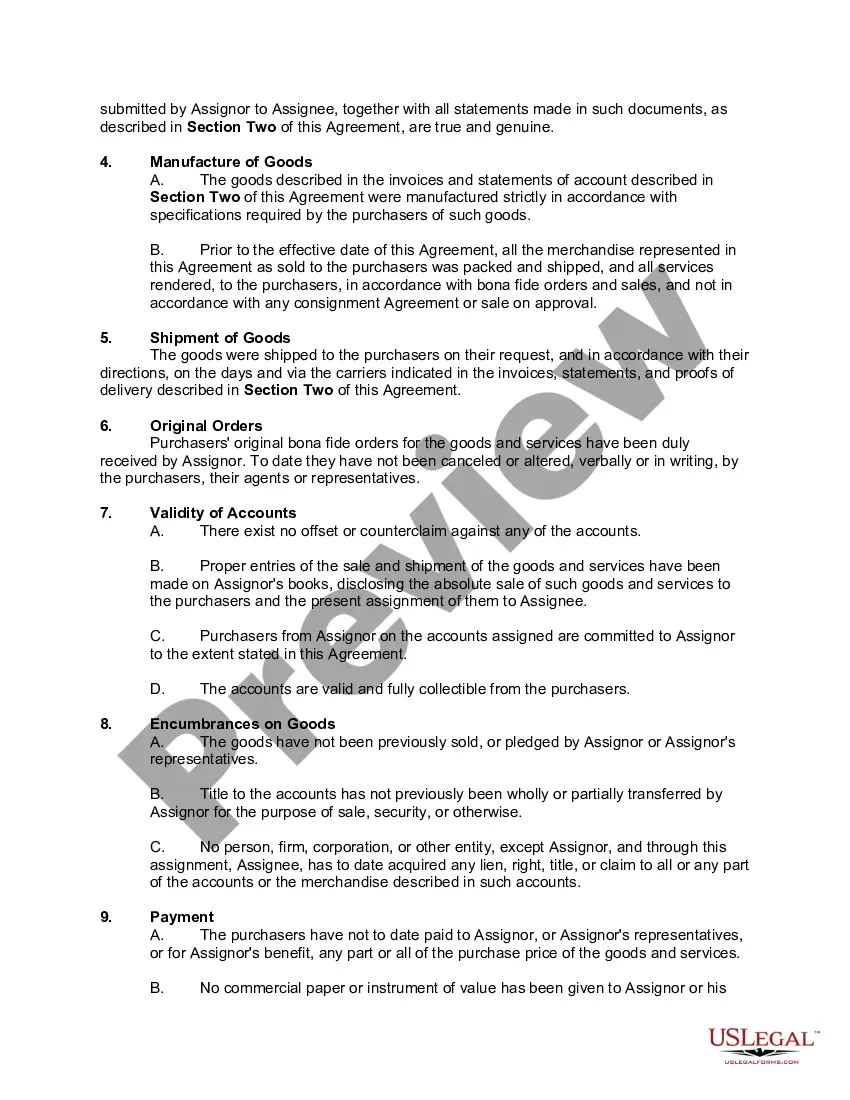

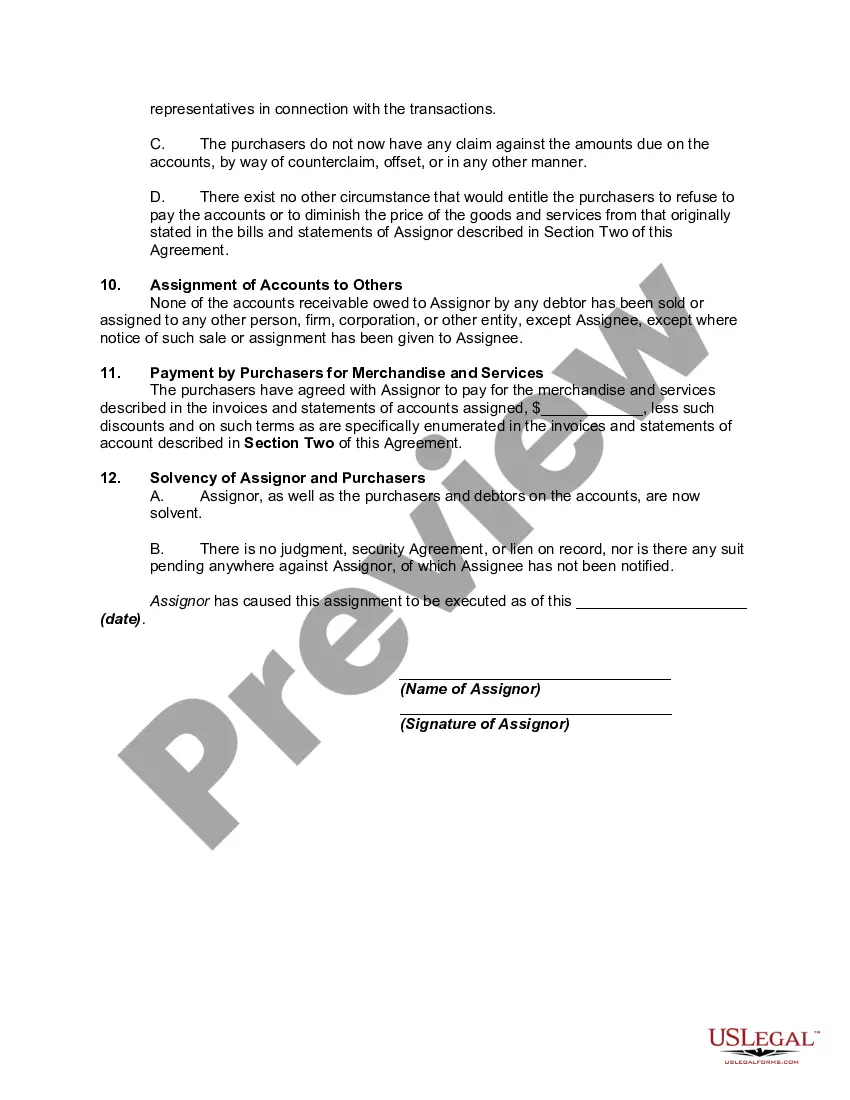

New Jersey Assignment of Accounts Receivable refers to a legal process where a business transfers its right to receive payment from its customers to another entity, often a financial institution or a factoring company. This enables businesses to access immediate cash flow by selling their accounts receivable at a discounted rate. Here is a detailed description of what New Jersey Assignment of Accounts Receivable entails, along with the different types that exist: 1. New Jersey Assignment of Accounts Receivable Process: The process of New Jersey Assignment of Accounts Receivable begins with a business (assignor) deciding to sell its outstanding invoices to a third party (assignee). This process is governed by state laws, including the Uniform Commercial Code (UCC), which provides a framework for regulating such transactions. To initiate the assignment, the assignor and the assignee enter into a written agreement, outlining the terms and conditions of the transaction. The agreement typically includes details such as the fee charged by the assignee, the duration of the assignment, and any guarantees or recourse options available. Once the assignment agreement is in place, the assignor transfers its accounts receivable to the assignee. The assignee now assumes the right to collect payment directly from the customers of the assignor. This allows the assignor to receive immediate cash for its outstanding invoices, improving its liquidity and working capital. 2. Different Types of New Jersey Assignment of Accounts Receivable: a) Recourse Assignment: In a recourse assignment, the assignor retains the risk of non-payment. If the assigned accounts become uncollectible, the assignee has the right to demand the assignor repurchases those accounts or compensates for any losses. b) Non-Recourse Assignment: In a non-recourse assignment, the assignee assumes the risk of non-payment. If customers fail to pay the assigned accounts, the assignee cannot seek compensation from the assignor. This type of assignment often involves higher fees to account for the increased risk borne by the assignee. c) Notification Assignment: A notification assignment involves notifying the customers of the business about the assignment of accounts receivable. The assignee sends a written notice to inform the customers that future payments should be made directly to the assignee rather than the assignor. d) Non-Notification Assignment: In a non-notification assignment, the assignor does not notify its customers about the assignment. The assignee collects payment directly without informing the customers of the transfer of rights. This type of assignment is typically confidential, preserving the business relationship between the assignor and its customers. 3. Benefits of New Jersey Assignment of Accounts Receivable: The New Jersey Assignment of Accounts Receivable offers several advantages to businesses, including: — Immediate cash flow: Assignors can access immediate working capital by selling their invoices, ensuring smooth business operations. — Reduced collection efforts: Assignors no longer need to spend time and resources on collecting payment from customers, as the assignee takes over this responsibility. — Risk mitigation: Assignors can shift the risk of non-payment to the assignee, depending on the type of assignment chosen. — Improved creditworthiness: By converting accounts receivable into cash, businesses can enhance their creditworthiness and may be able to secure better financing terms. The New Jersey Assignment of Accounts Receivable provides businesses in the state with a flexible financing option and a means to overcome cash flow challenges. By understanding the different types and benefits of this process, businesses can make informed decisions regarding their financial management strategies.

New Jersey Assignment of Accounts Receivable

Description

How to fill out New Jersey Assignment Of Accounts Receivable?

If you want to complete, download, or printing authorized file layouts, use US Legal Forms, the largest selection of authorized types, which can be found on-line. Make use of the site`s easy and convenient search to obtain the files you need. Various layouts for business and specific functions are categorized by groups and claims, or search phrases. Use US Legal Forms to obtain the New Jersey Assignment of Accounts Receivable within a number of click throughs.

In case you are presently a US Legal Forms consumer, log in in your accounts and then click the Acquire option to have the New Jersey Assignment of Accounts Receivable. You may also accessibility types you formerly delivered electronically in the My Forms tab of your respective accounts.

If you use US Legal Forms the very first time, refer to the instructions beneath:

- Step 1. Ensure you have selected the form for that correct area/region.

- Step 2. Use the Preview choice to examine the form`s content. Never overlook to read through the outline.

- Step 3. In case you are not satisfied using the develop, utilize the Research industry towards the top of the display screen to get other variations of your authorized develop design.

- Step 4. When you have discovered the form you need, select the Buy now option. Opt for the pricing strategy you prefer and put your references to sign up for an accounts.

- Step 5. Procedure the transaction. You should use your Мisa or Ьastercard or PayPal accounts to accomplish the transaction.

- Step 6. Find the format of your authorized develop and download it in your gadget.

- Step 7. Full, modify and printing or sign the New Jersey Assignment of Accounts Receivable.

Every single authorized file design you get is the one you have eternally. You may have acces to each and every develop you delivered electronically within your acccount. Select the My Forms section and select a develop to printing or download again.

Be competitive and download, and printing the New Jersey Assignment of Accounts Receivable with US Legal Forms. There are thousands of professional and express-specific types you can utilize to your business or specific needs.