New Jersey Aging of Accounts Receivable

Description

How to fill out Aging Of Accounts Receivable?

Are you presently in a role where you require documentation for potential organizational or personal purposes nearly every workday.

There are numerous legal document templates available online, but finding forms you can trust is challenging.

US Legal Forms offers thousands of form templates, including the New Jersey Aging of Accounts Receivable, designed to comply with state and federal requirements.

Once you have the right form, click Purchase now.

Choose a suitable pricing plan, provide the necessary information to set up your account, and complete the purchase using your PayPal or Visa or Mastercard.

- If you are already accustomed to the US Legal Forms website and possess an account, simply Log In.

- Then, you can download the New Jersey Aging of Accounts Receivable template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Locate the form you need and ensure it is for the appropriate city/county.

- Use the Review button to check the form.

- Read the description to confirm that you have selected the correct form.

- If the form does not match what you’re looking for, utilize the Search area to find the form that fits your requirements.

Form popularity

FAQ

Yes, filing an annual report for your LLC in New Jersey is mandatory for all businesses. This report helps you maintain active status with the state, which is beneficial for managing essential aspects like the New Jersey Aging of Accounts Receivable. You can simplify the filing process by leveraging services provided by USLegalForms, ensuring your compliance and peace of mind.

In New Jersey, you must renew your LLC every year by filing the annual report. This renewal is essential to protect your business's status and avoid penalties. By keeping your annual reports up to date, you also gain clearer insights into your business performance, including the management of your New Jersey Aging of Accounts Receivable. Staying proactive can save you potential setbacks.

Yes, as an LLC owner in New Jersey, you must file an annual report. This requirement helps maintain your business's good standing and can also help you better track your financial metrics, including the New Jersey Aging of Accounts Receivable. To navigate this process smoothly, consider utilizing services like USLegalForms to ensure compliance and stay organized.

Yes, you can file your NJ 1040HW online, which simplifies the process significantly. An online filing allows you to access tools and resources that can aid in managing your New Jersey Aging of Accounts Receivable. Using reputable platforms can streamline your filing process and reduce errors, ensuring you stay on top of your finances.

Schedule NJ COJ is a form used to report the details of contributions and adjustments for certain credits available to taxpayers in New Jersey. This schedule helps you accurately calculate your tax situation, which can be beneficial when evaluating your New Jersey Aging of Accounts Receivable. Therefore, you should ensure you complete it correctly to avoid surprises during tax time.

Line 29 on the New Jersey 1040 form relates to your adjusted gross income, which is a key figure that affects your tax liability. Understanding this line is important, as it can influence your financial strategies, including how you manage the New Jersey Aging of Accounts Receivable. For clarity, it's best to consult a tax professional or use comprehensive resources that explain tax forms in detail.

If you fail to file an annual report for your LLC, you may face penalties and potentially lose your business status in New Jersey. This is crucial because non-compliance can lead to complications in managing your New Jersey Aging of Accounts Receivable. Additionally, you might miss opportunities for growth. Consider using USLegalForms to stay compliant and manage your obligations efficiently.

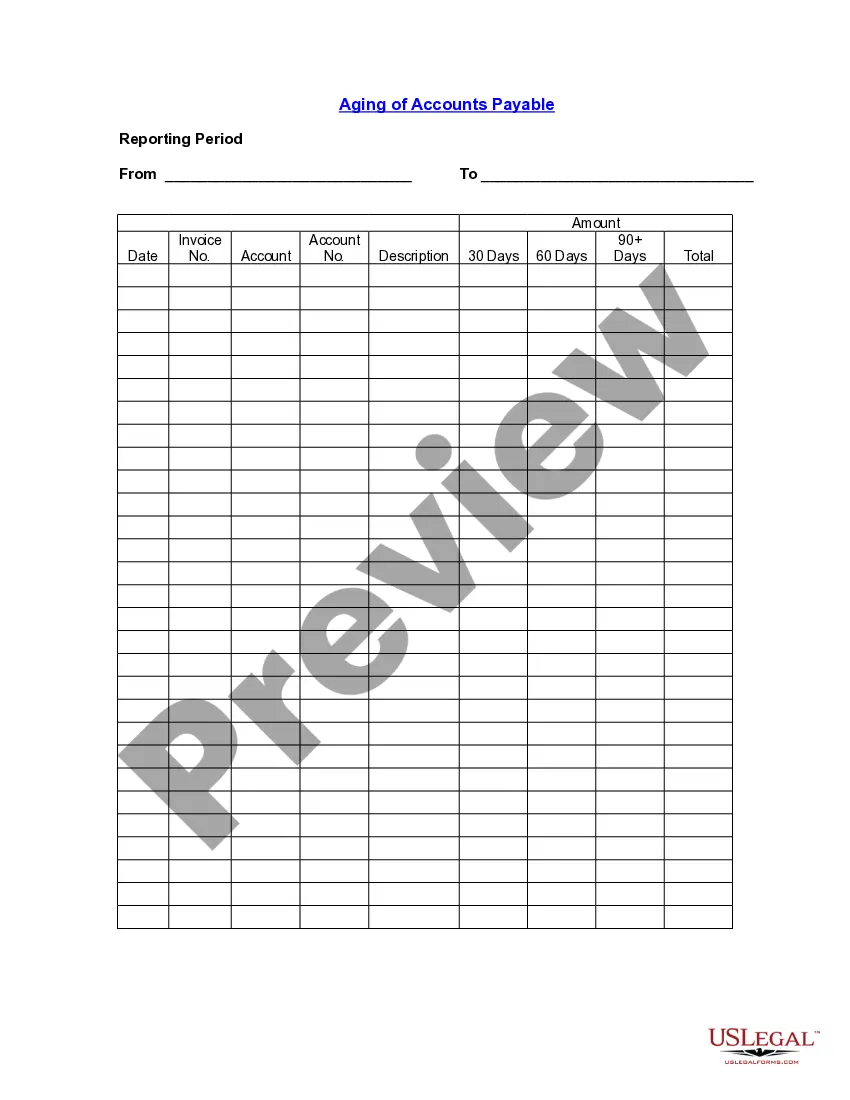

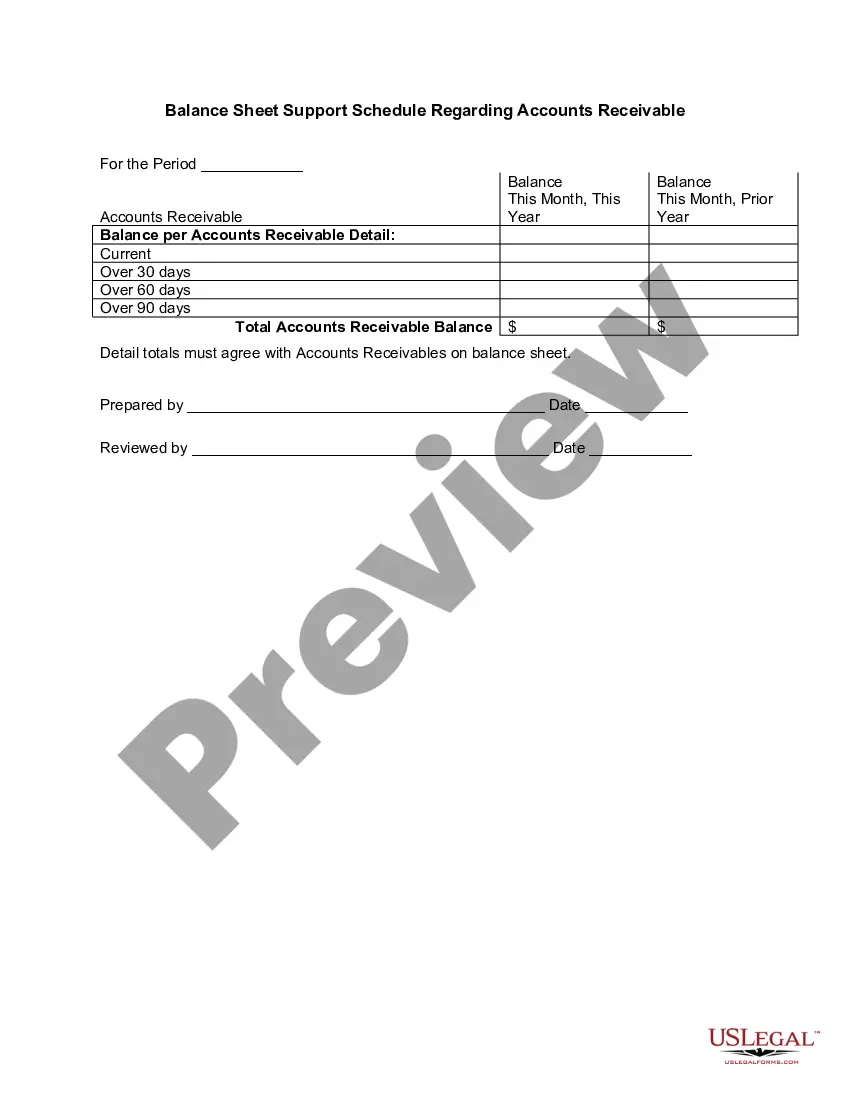

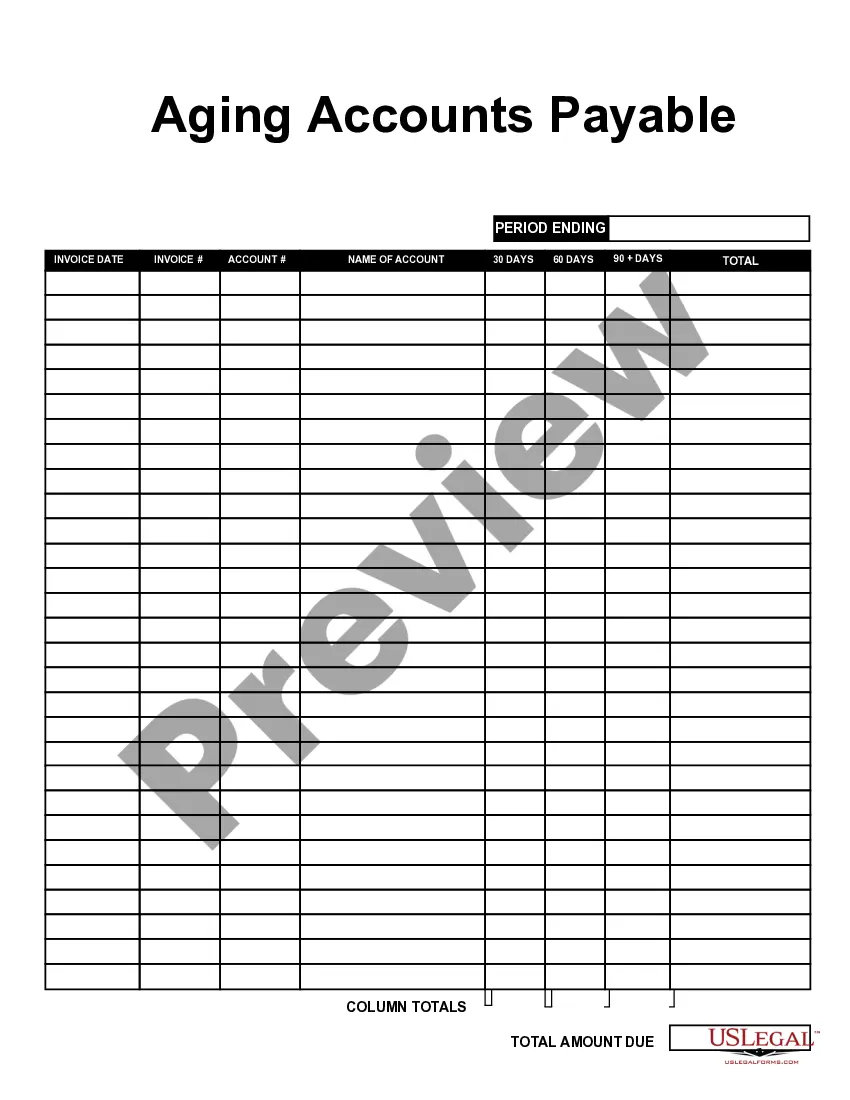

The aging table is a tool that summarizes the outstanding invoices and their respective aging categories. It visually represents the periods when payments are due and overdue. By utilizing an aging table, businesses can efficiently track their New Jersey Aging of Accounts Receivable and focus their collection efforts on the most critical accounts.

An aging schedule categorizes accounts receivable based on how long they have been outstanding. It typically includes categories such as current, 1-30 days, 31-60 days, and beyond. Utilizing this aging schedule can enhance your approach to New Jersey Aging of Accounts Receivable, making it easier to manage collections and revenue.

To calculate accounts receivable aging days, start by determining the invoice date for each account. Then, subtract the invoice date from the current date to find the number of days outstanding. This method provides a clear overview of your New Jersey Aging of Accounts Receivable and helps prioritize collection efforts.