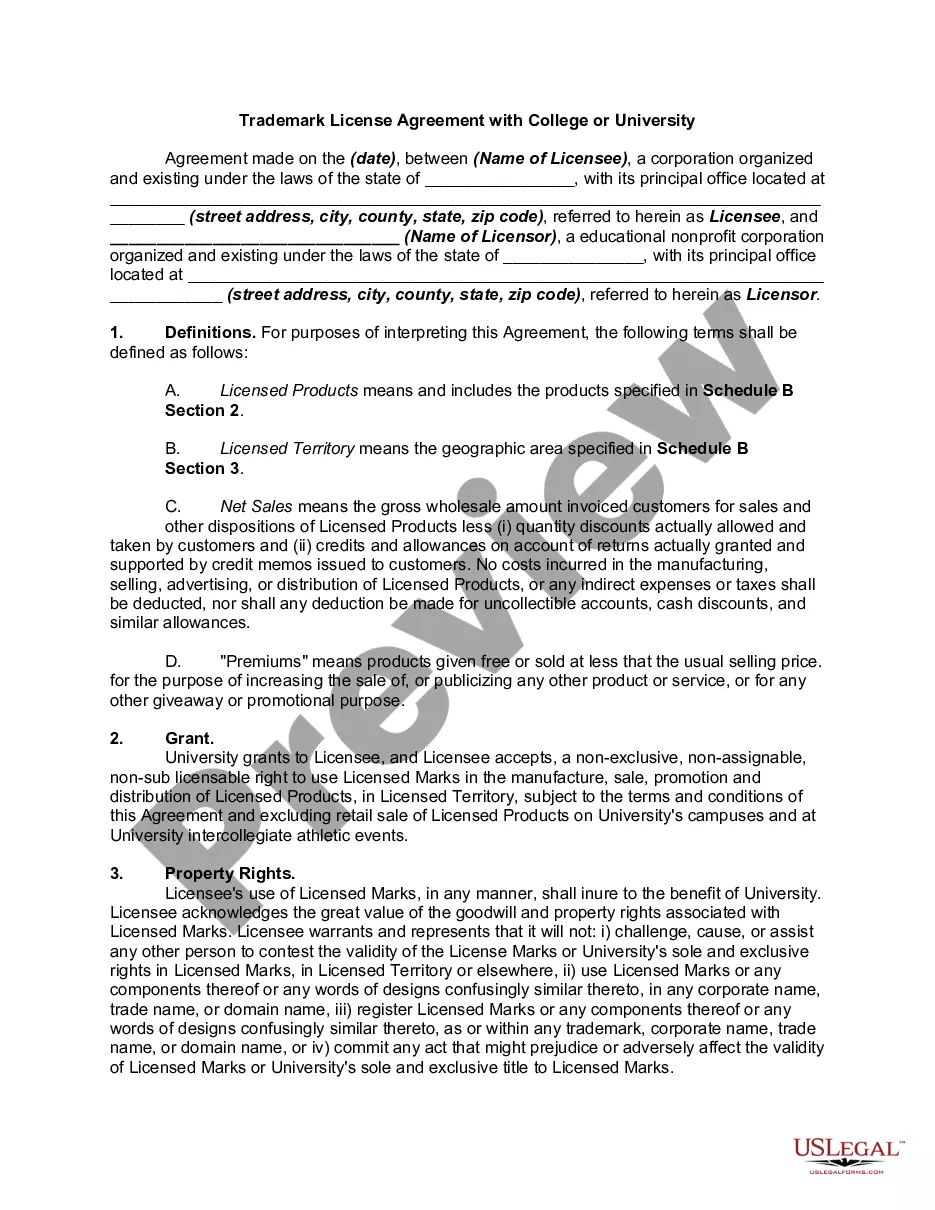

New Jersey Line of Credit or Loan Agreement Between Corporate or Business Borrower and Bank: A Line of Credit or Loan Agreement between Corporate or Business Borrower and a Bank is a legally binding document that outlines the terms and conditions of a borrowing arrangement in the state of New Jersey. This agreement provides a framework for businesses to access funds from a lender to meet their financial needs. The New Jersey Line of Credit or Loan Agreement may come in various types, each with its own specific purpose and features. Here are some common types: 1. Revolving Line of Credit Agreement: This type of agreement provides a predetermined credit limit that the borrower can draw upon over a specific period. Funds can be borrowed, repaid, and borrowed again repeatedly, making it a flexible financing option for businesses with fluctuating cash flow needs. 2. Term Loan Agreement: Unlike a line of credit, a term loan agreement offers a lump sum amount that the borrower must repay within a specified timeframe. It is typically used for more substantial investments or when a business requires a one-time infusion of capital. 3. Secured Loan Agreement: In this type of agreement, the borrower pledges collateral to secure the loan. The collateral, such as real estate or valuable assets, provides assurance to the lender and may enable the borrower to receive a lower interest rate or higher credit limit. 4. Unsecured Loan Agreement: Unlike a secured loan, an unsecured loan agreement does not require collateral. Instead, the lender evaluates the borrower's creditworthiness, financial statements, and other factors to determine the loan's terms and interest rate. This type of loan carries a higher risk for the lender, resulting in a potentially higher interest rate for the borrower. 5. Working Capital Line of Credit Agreement: Designed to meet the short-term financing needs of a business, this agreement provides funds to cover operational expenses, inventory purchases, or accounts receivable management. It helps businesses manage their cash flow gaps and maintain liquidity. The New Jersey Line of Credit or Loan Agreement typically includes details such as the amount of credit available, interest rates, repayment terms, fees, late payment penalties, and any applicable grace periods. The agreement also outlines the rights and responsibilities of both the borrower and the lender, ensuring transparency and clarity in the borrowing relationship. It's worth noting that legal advice is essential when drafting or reviewing this agreement, as compliance with New Jersey state laws and regulations is crucial to protect the interests of all parties involved. In conclusion, a New Jersey Line of Credit or Loan Agreement is a crucial tool for businesses seeking financial support from a bank. Whether it's a revolving line of credit or a term loan, this agreement establishes the terms and conditions for accessing funds, helping businesses meet their financial objectives and ensure a mutually beneficial relationship between the borrower and the lender.

New Jersey Line of Credit or Loan Agreement Between Corporate or Business Borrower and Bank

Description

How to fill out New Jersey Line Of Credit Or Loan Agreement Between Corporate Or Business Borrower And Bank?

US Legal Forms - one of many largest libraries of legal varieties in America - offers a wide array of legal file templates you may obtain or printing. Utilizing the web site, you can get thousands of varieties for company and personal uses, sorted by classes, says, or keywords.You can find the latest versions of varieties like the New Jersey Line of Credit or Loan Agreement Between Corporate or Business Borrower and Bank in seconds.

If you already have a subscription, log in and obtain New Jersey Line of Credit or Loan Agreement Between Corporate or Business Borrower and Bank from your US Legal Forms collection. The Down load option will appear on each kind you look at. You get access to all earlier downloaded varieties from the My Forms tab of your own account.

If you want to use US Legal Forms initially, listed here are straightforward instructions to obtain started out:

- Be sure you have picked out the right kind for your metropolis/region. Click on the Review option to examine the form`s content material. Read the kind explanation to actually have selected the proper kind.

- When the kind does not satisfy your demands, use the Search field at the top of the screen to discover the one which does.

- In case you are happy with the shape, confirm your choice by simply clicking the Acquire now option. Then, select the costs prepare you like and supply your qualifications to register to have an account.

- Approach the purchase. Make use of your bank card or PayPal account to accomplish the purchase.

- Choose the format and obtain the shape on the product.

- Make modifications. Complete, revise and printing and indication the downloaded New Jersey Line of Credit or Loan Agreement Between Corporate or Business Borrower and Bank.

Each and every web template you included with your money does not have an expiration date and is your own property eternally. So, if you would like obtain or printing another duplicate, just visit the My Forms segment and click on in the kind you require.

Get access to the New Jersey Line of Credit or Loan Agreement Between Corporate or Business Borrower and Bank with US Legal Forms, the most extensive collection of legal file templates. Use thousands of expert and state-distinct templates that satisfy your small business or personal needs and demands.