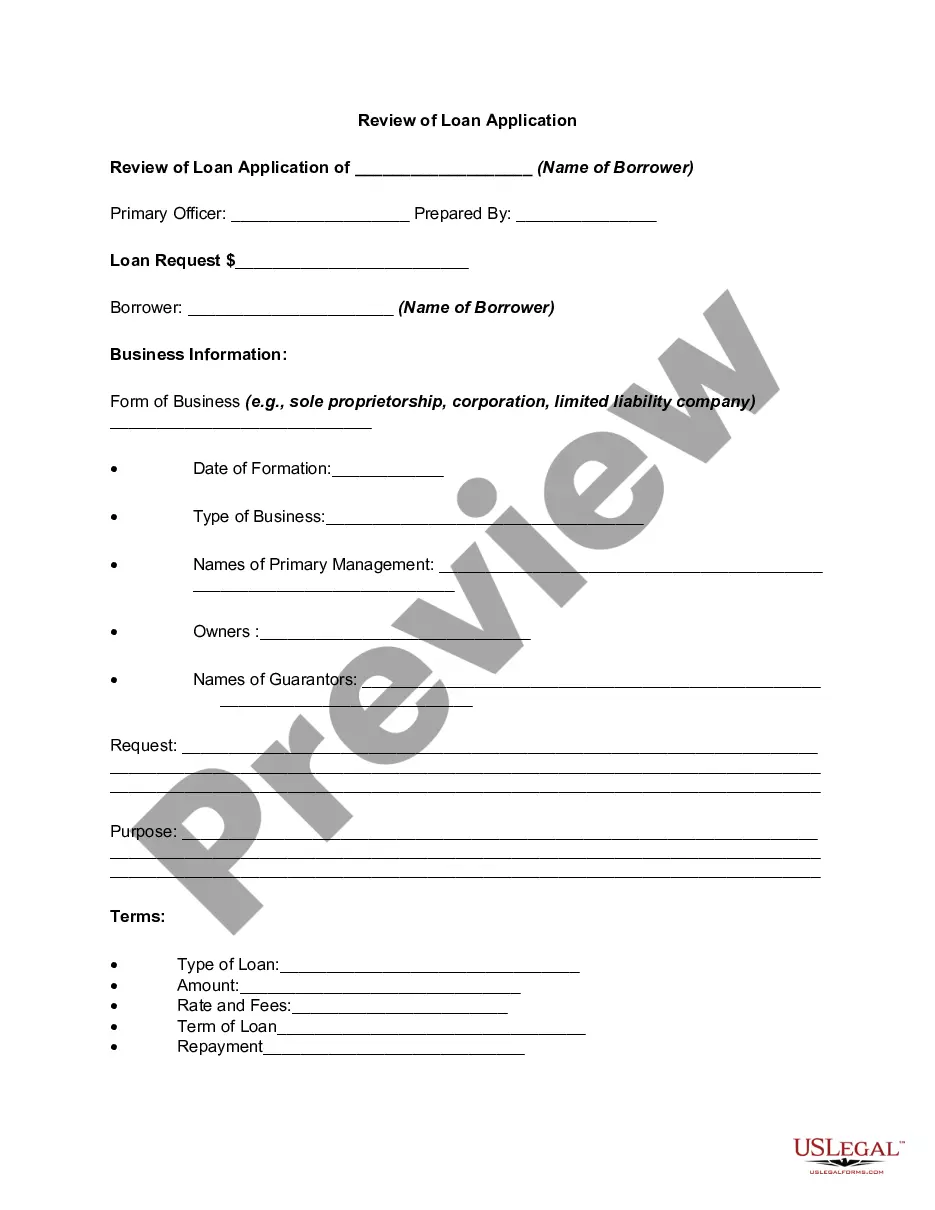

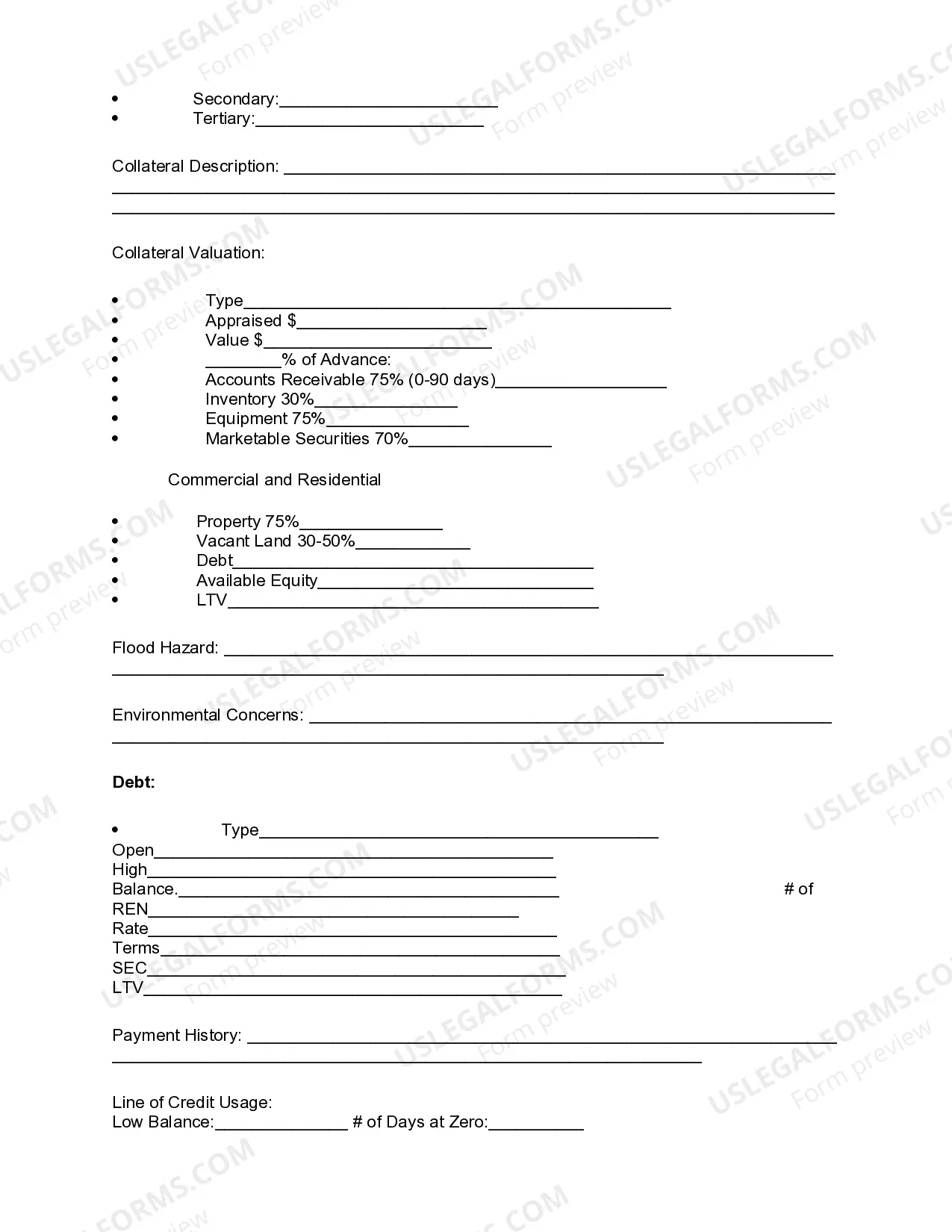

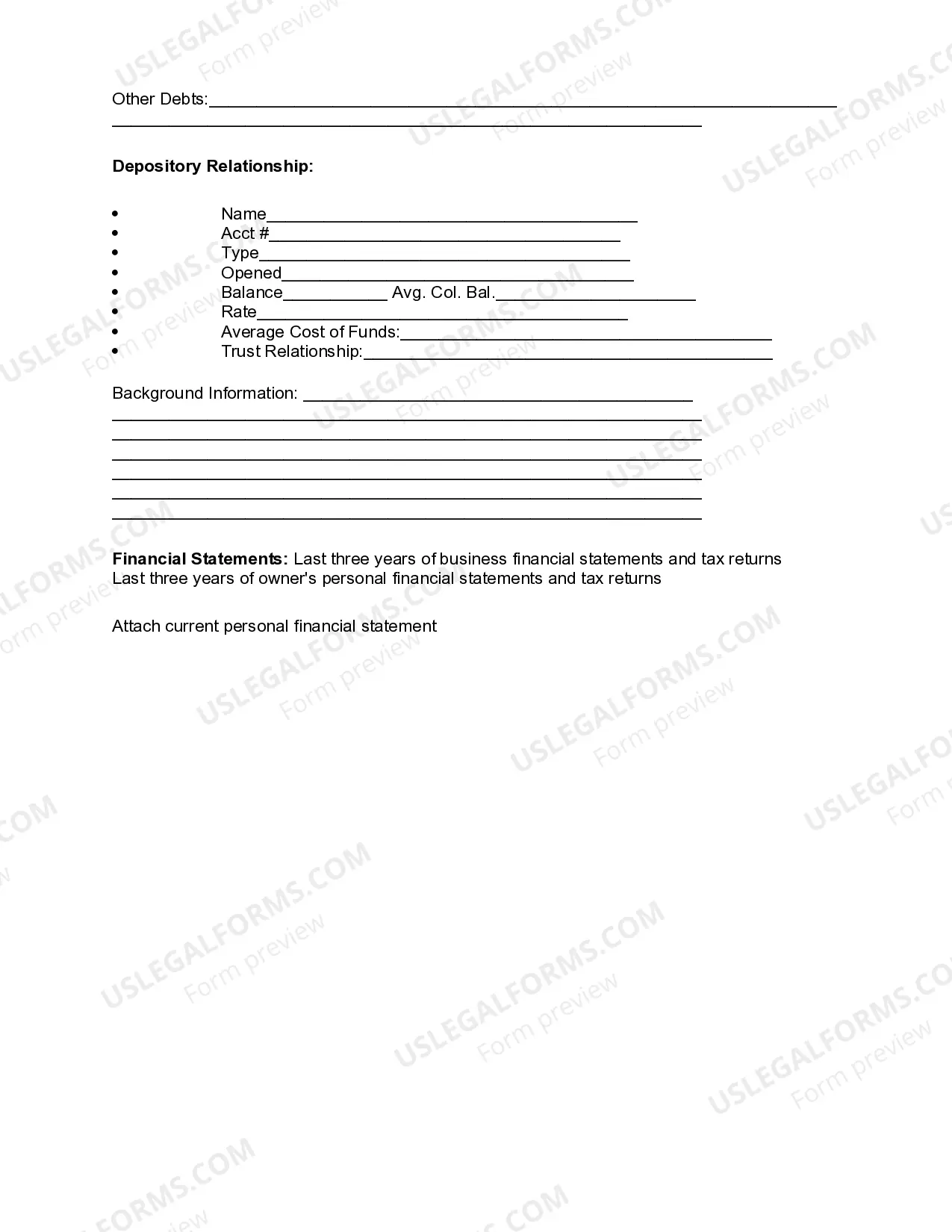

New Jersey Review of Loan Application is an essential step in the loan approval process for individuals and businesses based in the state of New Jersey. This comprehensive and detailed review ensures that borrowers meet the necessary requirements and provide accurate information, ensuring the credibility and legality of the loan application. When applying for a loan in New Jersey, there are various types of review processes that borrowers may encounter. These reviews can differ based on the loan type, including personal loans, mortgage loans, business loans, or student loans. Each loan type has specific criteria and documentation requirements that the borrower must fulfill. A typical New Jersey Review of Loan Application involves a careful examination of several key aspects. Firstly, the lender evaluates the borrower's creditworthiness by reviewing their credit history and credit score. This information provides insight into the borrower's financial responsibility, previous borrowing habits, and repayment patterns. Income verification is another crucial element of the review process. Lenders need to ensure that borrowers have a stable and consistent income source to repay the loan promptly. This verification usually includes reviewing pay stubs, tax returns, bank statements, and employment history. In addition to credit and income verification, lenders also analyze the borrower's debt-to-income ratio (DTI). DTI compares the borrower's monthly debt obligations to their monthly income, ensuring that they have sufficient capacity to handle additional loan payments. A lower DTI ratio signifies a lower risk for the lender. Furthermore, lenders may inquire about the purpose of the loan application. Different loans serve distinct purposes, such as home purchases, debt consolidation, education expenses, or business expansions. Understanding the loan's purpose helps the lender determine the appropriateness and feasibility of the loan application. Collateral may come into play for certain types of loans, such as mortgage loans or secured business loans. Lenders often assess the value and condition of the collateral to secure the loan in case of default. This step provides an added layer of protection for the lender. Lastly, identifying any potential red flags or inconsistencies is an integral part of the New Jersey Review of Loan Application. Lenders meticulously examine the application and supporting documents to ensure accuracy, legitimacy, and compliance with regulatory requirements. Any discrepancies or irregularities may delay or even lead to the rejection of the loan application. In conclusion, the New Jersey Review of Loan Application covers multiple aspects, such as creditworthiness, income verification, debt-to-income ratios, loan purpose, collateral evaluation, and identification of red flags. By conducting a thorough review, lenders minimize risks and make informed decisions when approving or rejecting loan applications.

New Jersey Review of Loan Application

Description

How to fill out New Jersey Review Of Loan Application?

It is possible to commit hrs online searching for the legal papers format that meets the state and federal needs you will need. US Legal Forms gives thousands of legal types which can be analyzed by pros. You can actually download or print out the New Jersey Review of Loan Application from your services.

If you have a US Legal Forms accounts, you may log in and then click the Down load key. After that, you may complete, change, print out, or sign the New Jersey Review of Loan Application. Every legal papers format you purchase is the one you have forever. To get one more duplicate for any acquired type, check out the My Forms tab and then click the corresponding key.

If you use the US Legal Forms site the first time, keep to the easy recommendations under:

- Initially, make certain you have selected the correct papers format for your state/metropolis that you pick. Browse the type information to make sure you have selected the proper type. If accessible, take advantage of the Review key to check throughout the papers format at the same time.

- If you would like get one more model in the type, take advantage of the Lookup field to discover the format that fits your needs and needs.

- Upon having identified the format you need, click on Buy now to proceed.

- Choose the prices prepare you need, key in your accreditations, and register for a merchant account on US Legal Forms.

- Total the financial transaction. You can utilize your charge card or PayPal accounts to pay for the legal type.

- Choose the formatting in the papers and download it to the product.

- Make modifications to the papers if possible. It is possible to complete, change and sign and print out New Jersey Review of Loan Application.

Down load and print out thousands of papers web templates utilizing the US Legal Forms site, that offers the biggest variety of legal types. Use professional and express-particular web templates to take on your organization or individual needs.

Form popularity

FAQ

The loan has been assigned to an underwriter to review and approve the loan. It is a normal process don't be alarmed by the wording. Once the loan is approved, the underwriter will request any additional documents needed for what is called the clear to close.

A credit review?also known as account monitoring or account review inquiry?is a periodic assessment of an individual's or business's credit profile. Creditors?such as banks, financial services institutions, credit bureaus, settlement companies, and credit counselors?may conduct credit reviews.

Getting approved for a personal loan generally takes anywhere from one day to one week. As we mentioned above, how long it takes for a personal loan to go through depends on several factors, like your credit score. However, one of the primary factors that will affect your approval time is where you get your loan from.

Typically, a loan review is conducted on commercial loan files, either internally by bank or credit union staff, or by hired third-party auditors. These investigators check for completeness of loan documentation and/or evaluate loan performance.

Loan review refers to examining outstanding loans to make sure borrowers adhere to their credit agreements and the bank follows its loan policies. While banks today use various loan review procedures, a few general principles are followed by nearly all banks.

Getting approved for a personal loan generally takes anywhere from one day to one week. As we mentioned above, how long it takes for a personal loan to go through depends on several factors, like your credit score. However, one of the primary factors that will affect your approval time is where you get your loan from.

A loan review provides an assessment of the overall quality of a loan portfolio. Specifically, a loan review: ? Assesses individual loans, including repayment risks.

Once you have applied for the loan, you can visit the lender's website to check your loan status. After loan approval, your loan amount will be disbursed within a few hours to your bank account.