Partnership agreements are written documents that explicitly detail the relationship between the business partners and their individual obligations and contributions to the partnership. Since partnership agreements should cover all possible business situations that could arise during the partnership's life, the documents are often complex; legal counsel in drafting and reviewing the finished contract is generally recommended. If a partnership does not have a partnership agreement in place when it dissolves, the guidelines of the Uniform Partnership Act and various state laws will determine how the assets and debts of the partnership are distributed.

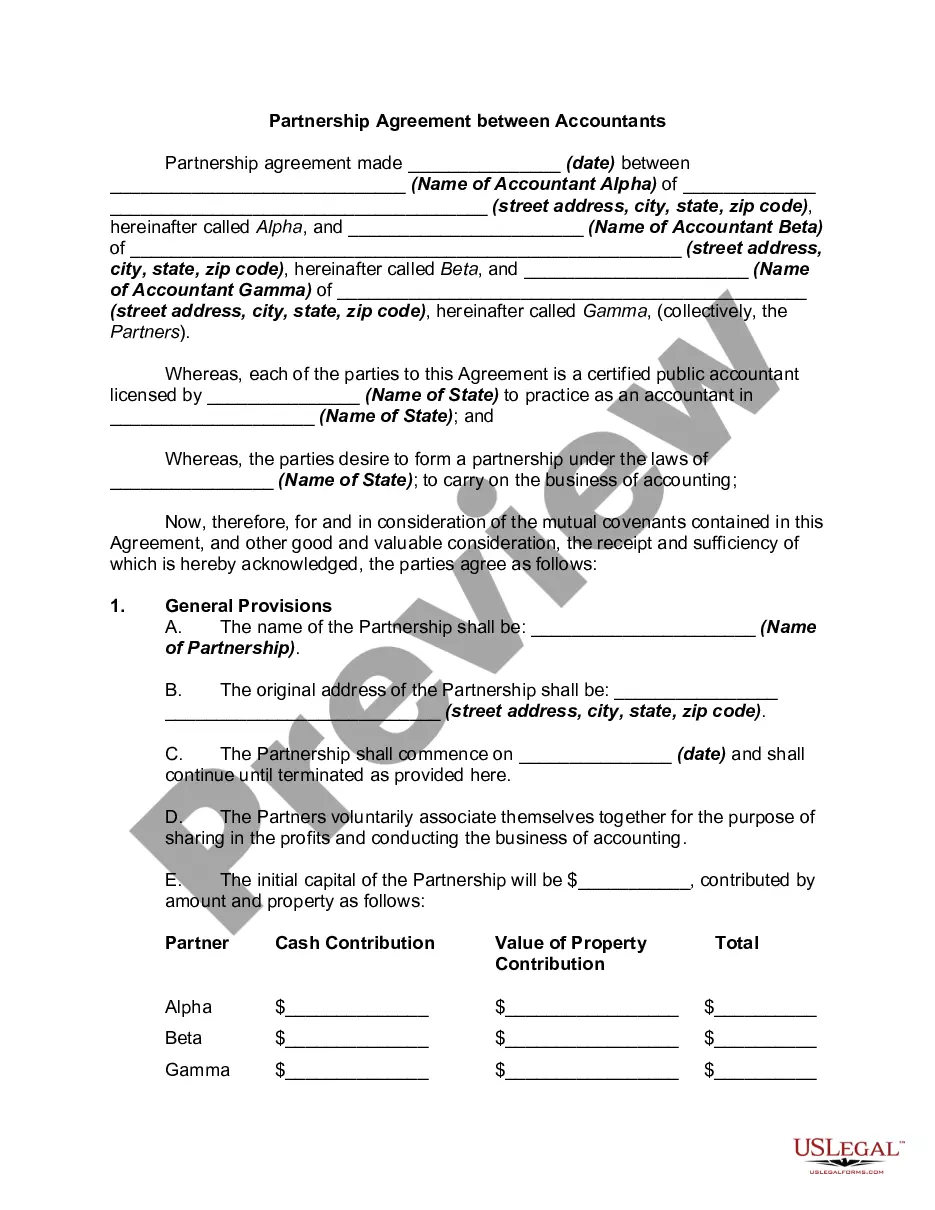

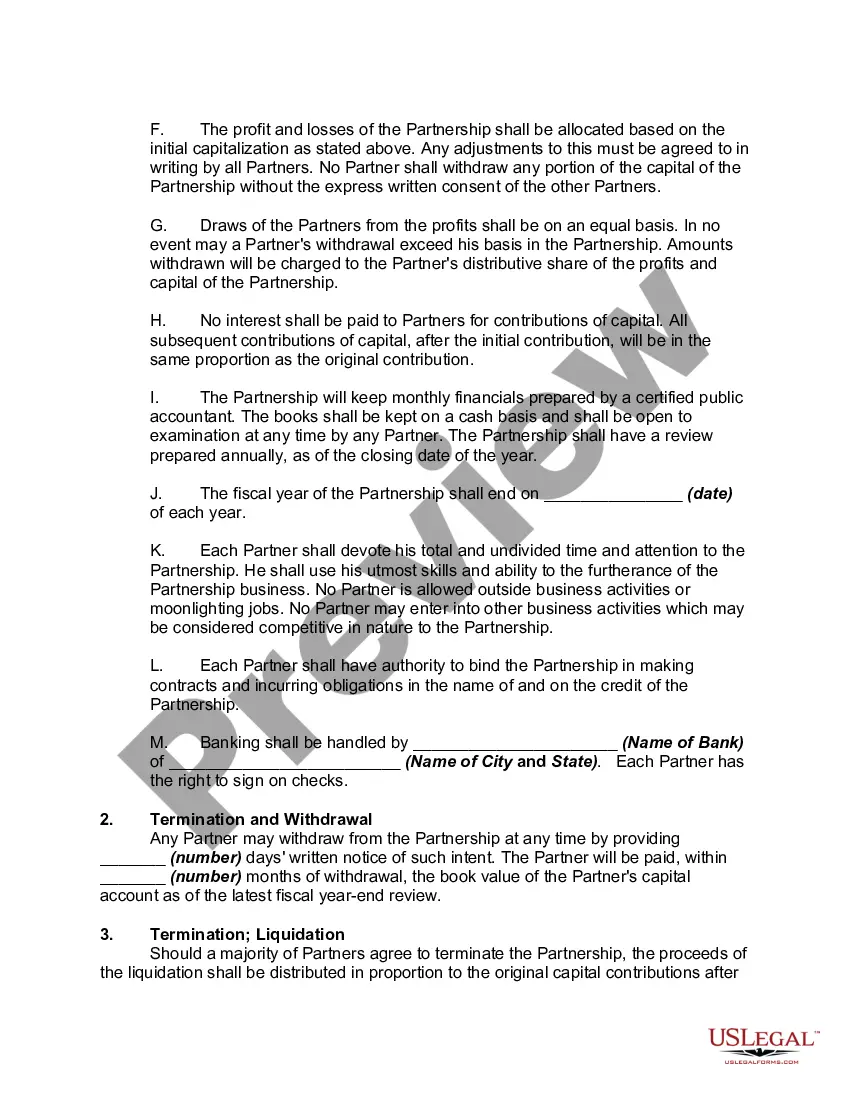

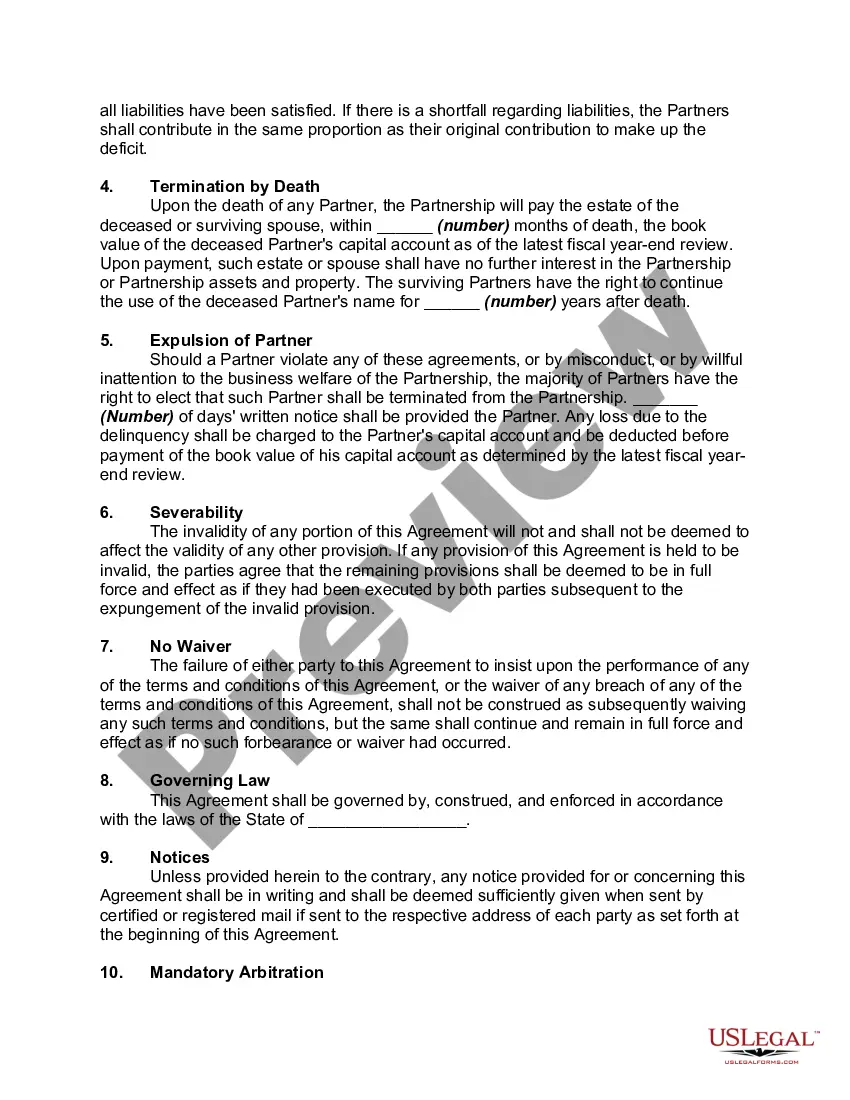

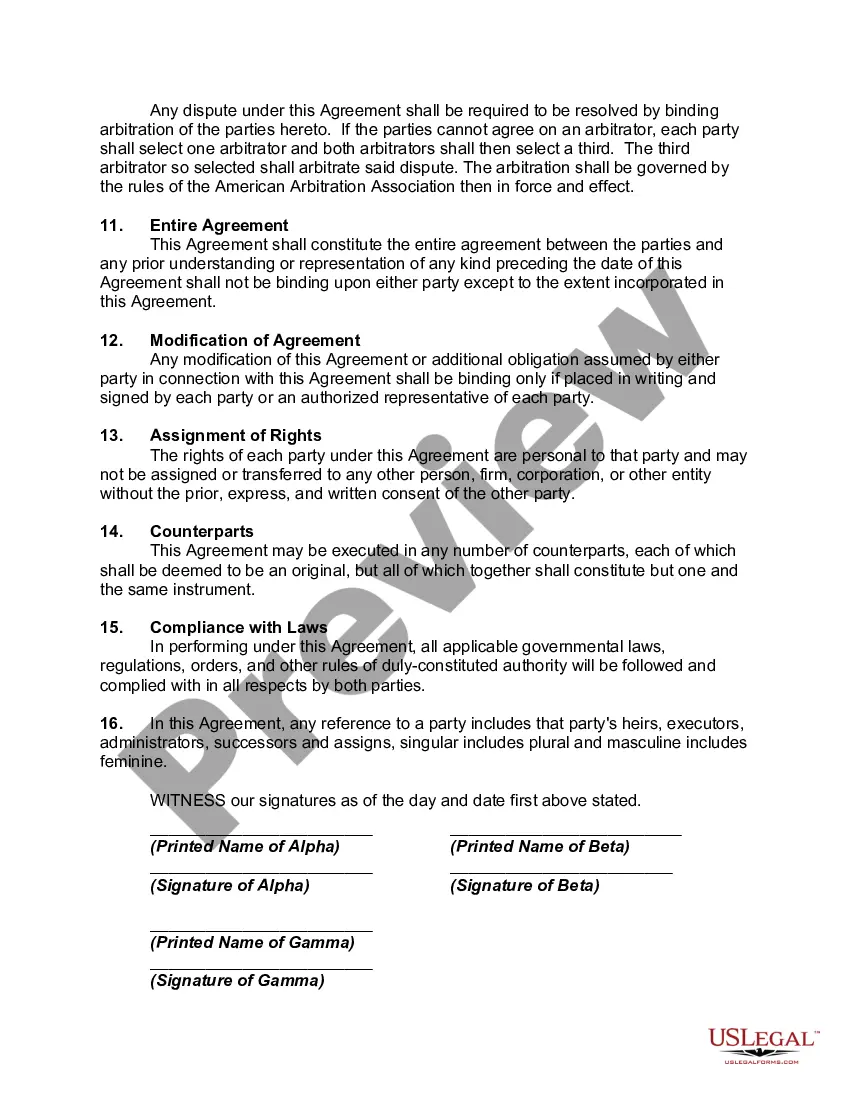

A New Jersey Partnership Agreement between Accountants is a legally binding contract that outlines the terms and conditions of a partnership formed among accountants in the state of New Jersey. This agreement establishes the relationship between the partners and governs the operation, management, and financial aspects of the partnership. The agreement typically contains several key provisions, including but not limited to: 1. Partnership Formation: This section outlines the process of forming the partnership, including the names and contact information of the partners, the effective date of the agreement, and the purpose or objectives of the partnership. 2. Capital Contribution: This provision specifies each partner's initial contribution to the partnership's capital, whether in cash, assets, or services. It also details any additional contributions required from partners in the future and the consequences of failing to make such contributions. 3. Profit and Loss Sharing: The partnership agreement defines the distribution of profits and losses among partners, usually in proportion to their capital contributions or through a predetermined formula. It may also include special provisions for allocating profits or losses in certain circumstances. 4. Decision-Making Authority: This section outlines the decision-making process within the partnership, including the voting rights of each partner and the procedures for making important business decisions. It may also include provisions for resolving disputes or deadlocks among partners. 5. Duties and Responsibilities: The agreement defines the roles, responsibilities, and obligations of each partner in the partnership. It outlines the scope of services to be provided, expectations regarding work hours, client management, and any restrictions on pursuing other business interests. 6. Withdrawal and Termination: This provision outlines the process for partners to withdraw from the partnership and the consequences of such withdrawal. It may also specify the circumstances under which the partnership can be terminated, such as retirement, death, or bankruptcy of a partner. 7. Non-Compete and Confidentiality: The partnership agreement may include clauses prohibiting partners from engaging in competing businesses or disclosing sensitive information to third parties. These provisions protect the partnership's intellectual property, client relationships, and trade secrets. Types of New Jersey Partnership Agreement Between Accountants: 1. General Partnership Agreement: This is the most common type of partnership agreement, where all partners equally share profits, losses, decision-making authority, and responsibilities. Each partner is personally liable for the partnership's debts. 2. Limited Partnership Agreement: In this type of agreement, there are general partners who manage the business and have unlimited liability, and limited partners who only contribute capital and have limited liability. Limited partners are not actively involved in the partnership's day-to-day operations. 3. Limited Liability Partnership Agreement (LLP): This agreement provides partners with limited liability protection, shielding their personal assets from the partnership's debts and obligations. Laps are commonly chosen by professional service firms, including accountants, to limit their personal exposure. In conclusion, a New Jersey Partnership Agreement between Accountants is a crucial document that establishes the framework for a collaborative business venture. It addresses important aspects of the partnership, protects the interests of all partners, and ensures the smooth functioning of the accounting practice in compliance with New Jersey state regulations.A New Jersey Partnership Agreement between Accountants is a legally binding contract that outlines the terms and conditions of a partnership formed among accountants in the state of New Jersey. This agreement establishes the relationship between the partners and governs the operation, management, and financial aspects of the partnership. The agreement typically contains several key provisions, including but not limited to: 1. Partnership Formation: This section outlines the process of forming the partnership, including the names and contact information of the partners, the effective date of the agreement, and the purpose or objectives of the partnership. 2. Capital Contribution: This provision specifies each partner's initial contribution to the partnership's capital, whether in cash, assets, or services. It also details any additional contributions required from partners in the future and the consequences of failing to make such contributions. 3. Profit and Loss Sharing: The partnership agreement defines the distribution of profits and losses among partners, usually in proportion to their capital contributions or through a predetermined formula. It may also include special provisions for allocating profits or losses in certain circumstances. 4. Decision-Making Authority: This section outlines the decision-making process within the partnership, including the voting rights of each partner and the procedures for making important business decisions. It may also include provisions for resolving disputes or deadlocks among partners. 5. Duties and Responsibilities: The agreement defines the roles, responsibilities, and obligations of each partner in the partnership. It outlines the scope of services to be provided, expectations regarding work hours, client management, and any restrictions on pursuing other business interests. 6. Withdrawal and Termination: This provision outlines the process for partners to withdraw from the partnership and the consequences of such withdrawal. It may also specify the circumstances under which the partnership can be terminated, such as retirement, death, or bankruptcy of a partner. 7. Non-Compete and Confidentiality: The partnership agreement may include clauses prohibiting partners from engaging in competing businesses or disclosing sensitive information to third parties. These provisions protect the partnership's intellectual property, client relationships, and trade secrets. Types of New Jersey Partnership Agreement Between Accountants: 1. General Partnership Agreement: This is the most common type of partnership agreement, where all partners equally share profits, losses, decision-making authority, and responsibilities. Each partner is personally liable for the partnership's debts. 2. Limited Partnership Agreement: In this type of agreement, there are general partners who manage the business and have unlimited liability, and limited partners who only contribute capital and have limited liability. Limited partners are not actively involved in the partnership's day-to-day operations. 3. Limited Liability Partnership Agreement (LLP): This agreement provides partners with limited liability protection, shielding their personal assets from the partnership's debts and obligations. Laps are commonly chosen by professional service firms, including accountants, to limit their personal exposure. In conclusion, a New Jersey Partnership Agreement between Accountants is a crucial document that establishes the framework for a collaborative business venture. It addresses important aspects of the partnership, protects the interests of all partners, and ensures the smooth functioning of the accounting practice in compliance with New Jersey state regulations.