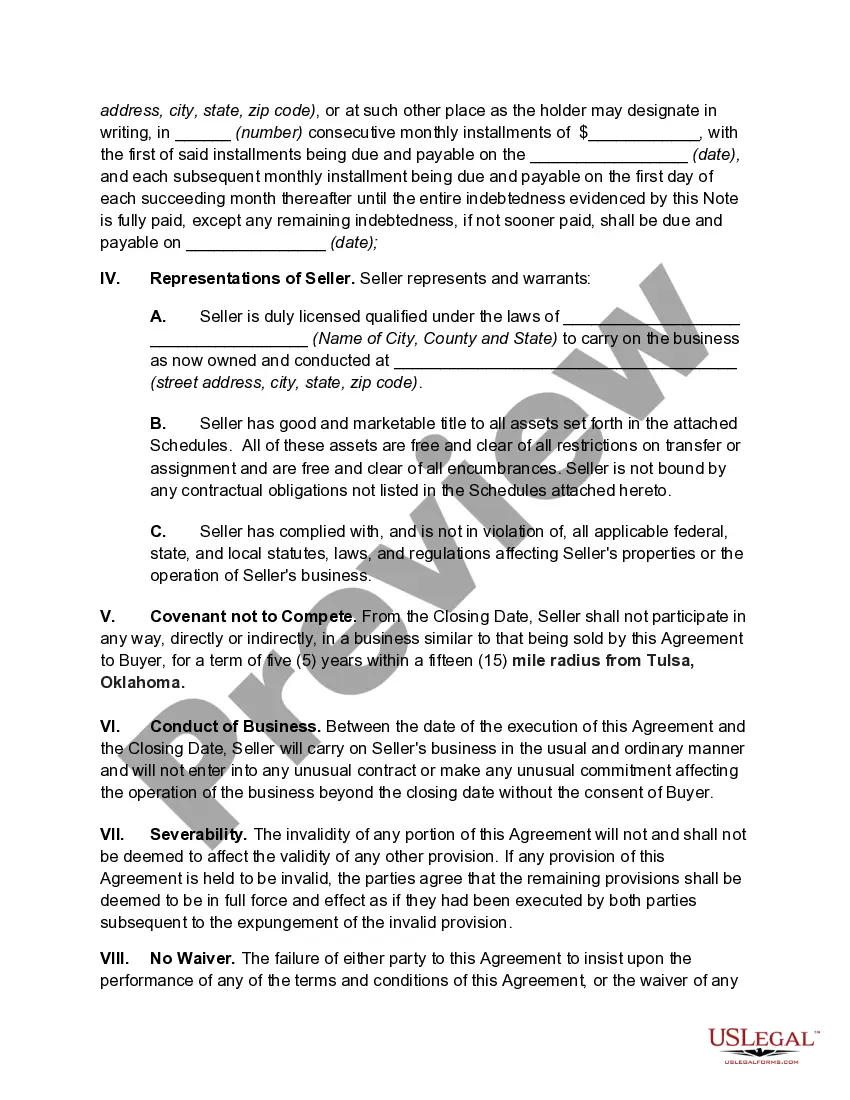

The sale of any ongoing business, even a sole proprietorship, can be a complicated transaction. The buyer and seller (and their attorneys) must consider the law of contracts, taxation, real estate, corporations, securities, and antitrust in many situations. Depending on the nature of the business sold, statutes and regulations concerning the issuance and transfer of permits, licenses, and/or franchises should be consulted. If a license or franchise is important to the business, the buyer generally would want to make the sales agreement contingent on such approval. Sometimes, the buyer will assume certain debts, liabilities, or obligations of the seller. In such a sale, it is vital that the buyer know exactly what debts he/she is assuming.

In any sale of a business, the buyer and the seller should make sure that the sale complies with any Bulk Sales Law of the state whose laws govern the transaction. A bulk sale is a sale of goods by a business which engages in selling items out of inventory (as opposed to manufacturing or service industries). Article 6 of the Uniform Commercial Code, which has been adopted at least in part by all states, governs bulk sales. If the sale involves a business covered by Article 6 and the parties do not follow the statutory requirements, the sale can be void as against the seller's creditors, and the buyer may be personally liable to them. Sometimes, rather than follow all of the requirements of the bulk sales law, a seller will specifically agree to indemnify the buyer for any liabilities that result to the buyer for failure to comply with the bulk sales law.

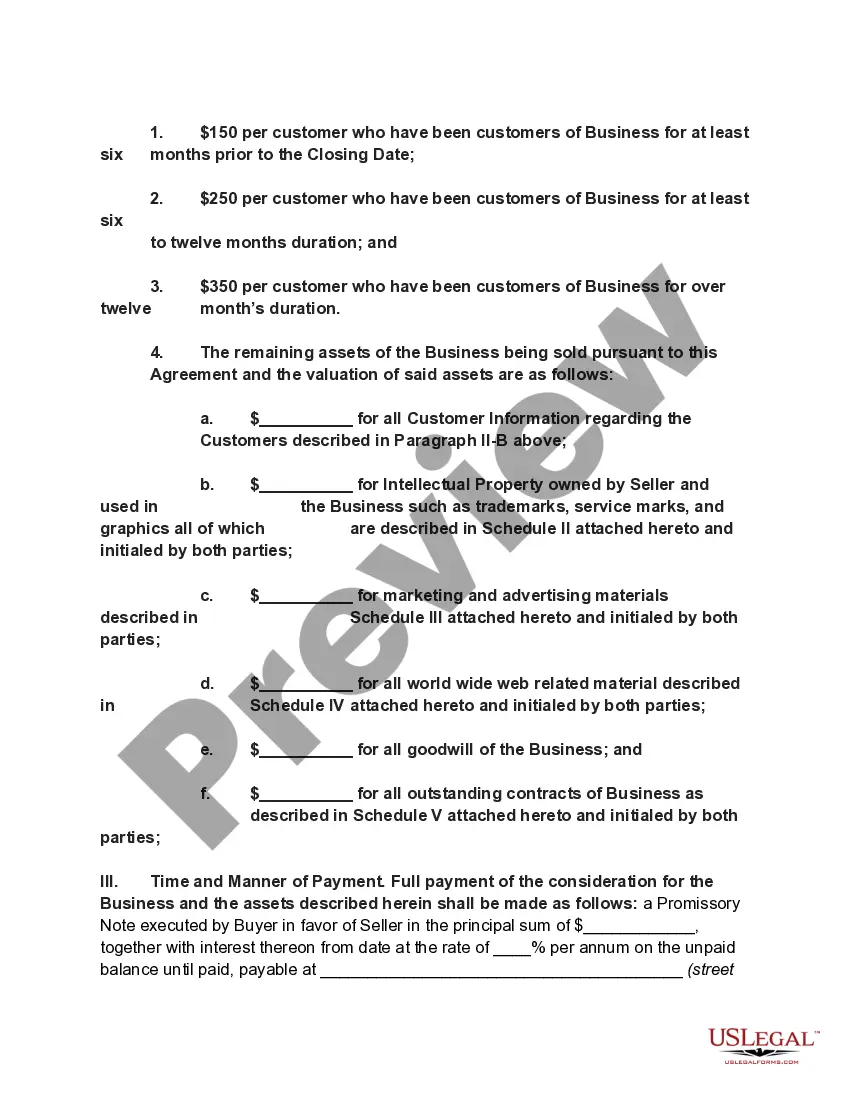

Of course the sellerýs financial statements should be studied by the buyer and/or the buyerýs accountants. The balance sheet and other financial reports reflect the financial condition of the business. The seller should be required to represent that it has no material obligations or liabilities that were not reflected in the balance sheet and that it will not incur any obligations or liabilities in the period from the date of the balance sheet to the date of closing, except those incurred in the regular course of business.

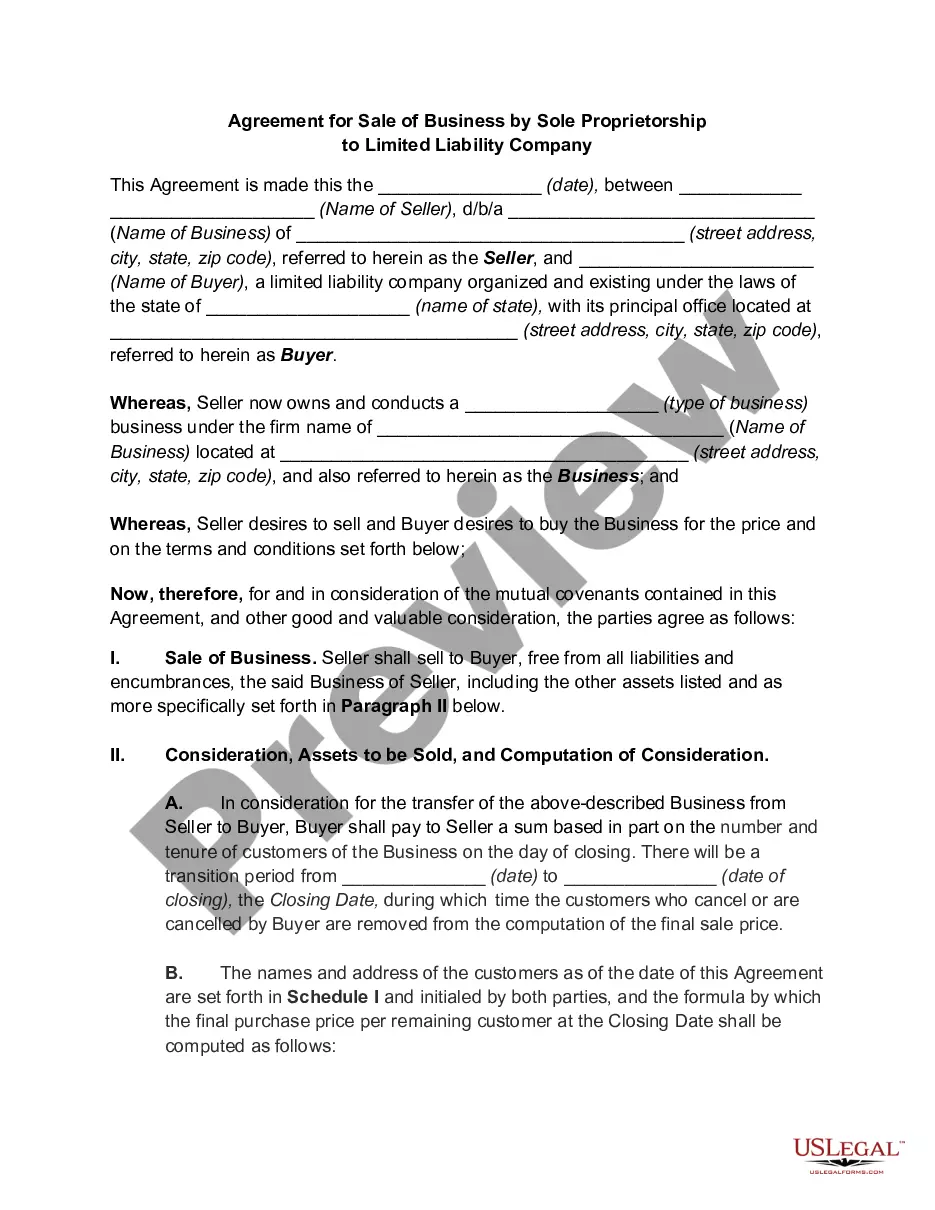

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

The New Jersey Agreement for Sale of Business by Sole Proprietorship to Limited Liability Company is a legal document that outlines the terms and conditions for the transfer of a business from a sole proprietorship to a limited liability company (LLC) in the state of New Jersey. This agreement protects the interests of both the seller (sole proprietorship) and the buyer (LLC) and facilitates a smooth transition of ownership. The agreement typically includes specific details such as the effective date of the sale, the names and addresses of both parties, the assets and liabilities being transferred, the purchase price, payment terms, and any additional conditions agreed upon by both parties. Different types of New Jersey Agreement for Sale of Business by Sole Proprietorship to Limited Liability Company may include variations tailored to specific industries or circumstances. Some examples are: 1. Restaurant Sale Agreement: Specifically designed for the transfer of a restaurant from a sole proprietorship to an LLC. It may include provisions for the transfer of liquor licenses, inventory, and cooking equipment. 2. Retail Store Sale Agreement: This type of agreement is ideal for the sale of a retail business, and it may address the transfer of inventory, fixtures, customer lists, and lease agreements for the retail space. 3. Service-Based Business Sale Agreement: Geared towards service-oriented businesses like consulting firms or IT companies, this agreement may include clauses pertaining to the transfer of client contracts, non-compete agreements, and intellectual property rights. 4. Real Estate Sale Agreement: When a sole proprietorship owns property, this agreement becomes crucial for transferring ownership of the property along with the business. It may cover property details, such as title transfers, leases, and permits. 5. Manufacturing Business Sale Agreement: Designed specifically for manufacturing businesses, this agreement may include provisions for the transfer of equipment, raw materials, patents, and supply contracts. In all cases, it is essential to consult legal professionals and ensure compliance with New Jersey state laws and regulations when drafting and executing the Agreement for Sale of Business by Sole Proprietorship to Limited Liability Company.The New Jersey Agreement for Sale of Business by Sole Proprietorship to Limited Liability Company is a legal document that outlines the terms and conditions for the transfer of a business from a sole proprietorship to a limited liability company (LLC) in the state of New Jersey. This agreement protects the interests of both the seller (sole proprietorship) and the buyer (LLC) and facilitates a smooth transition of ownership. The agreement typically includes specific details such as the effective date of the sale, the names and addresses of both parties, the assets and liabilities being transferred, the purchase price, payment terms, and any additional conditions agreed upon by both parties. Different types of New Jersey Agreement for Sale of Business by Sole Proprietorship to Limited Liability Company may include variations tailored to specific industries or circumstances. Some examples are: 1. Restaurant Sale Agreement: Specifically designed for the transfer of a restaurant from a sole proprietorship to an LLC. It may include provisions for the transfer of liquor licenses, inventory, and cooking equipment. 2. Retail Store Sale Agreement: This type of agreement is ideal for the sale of a retail business, and it may address the transfer of inventory, fixtures, customer lists, and lease agreements for the retail space. 3. Service-Based Business Sale Agreement: Geared towards service-oriented businesses like consulting firms or IT companies, this agreement may include clauses pertaining to the transfer of client contracts, non-compete agreements, and intellectual property rights. 4. Real Estate Sale Agreement: When a sole proprietorship owns property, this agreement becomes crucial for transferring ownership of the property along with the business. It may cover property details, such as title transfers, leases, and permits. 5. Manufacturing Business Sale Agreement: Designed specifically for manufacturing businesses, this agreement may include provisions for the transfer of equipment, raw materials, patents, and supply contracts. In all cases, it is essential to consult legal professionals and ensure compliance with New Jersey state laws and regulations when drafting and executing the Agreement for Sale of Business by Sole Proprietorship to Limited Liability Company.