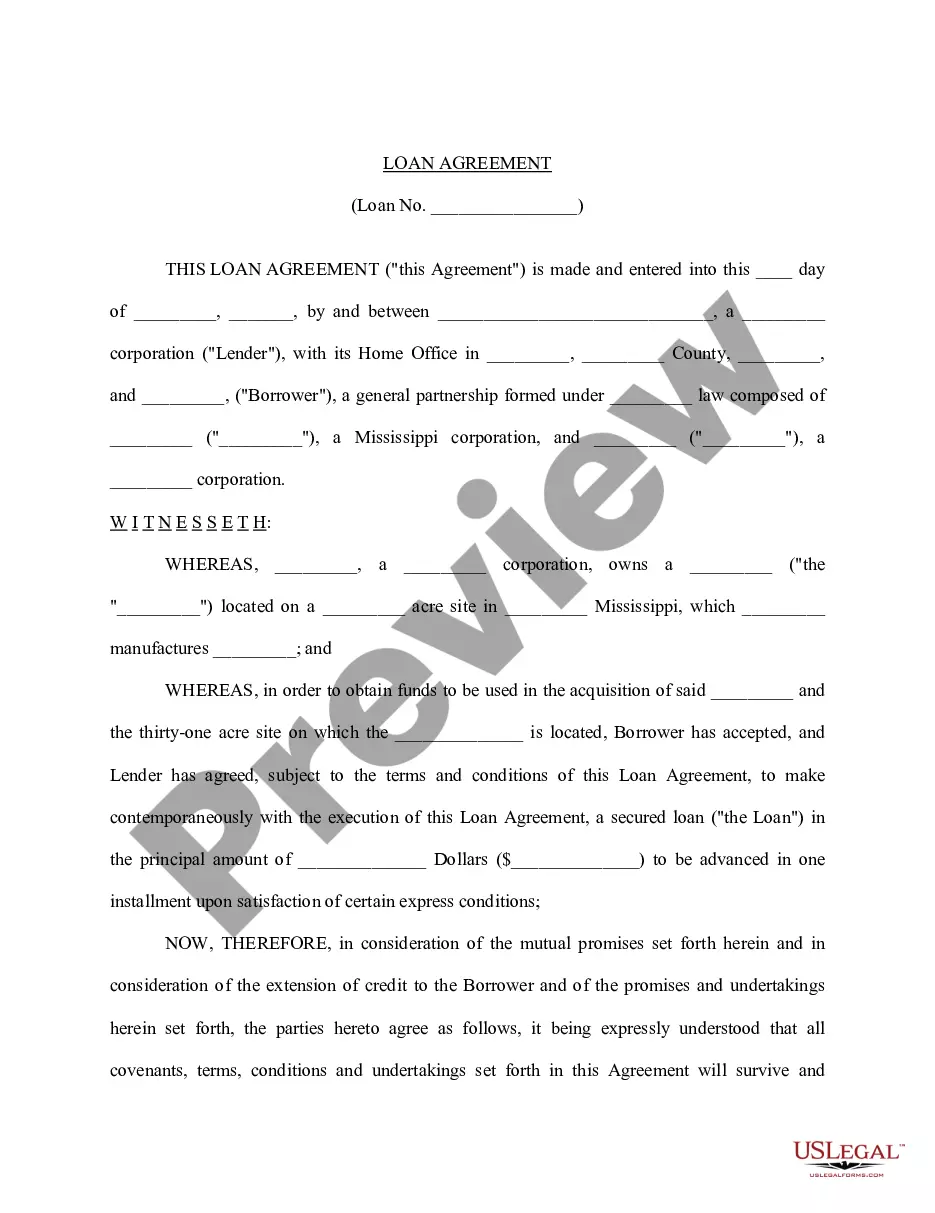

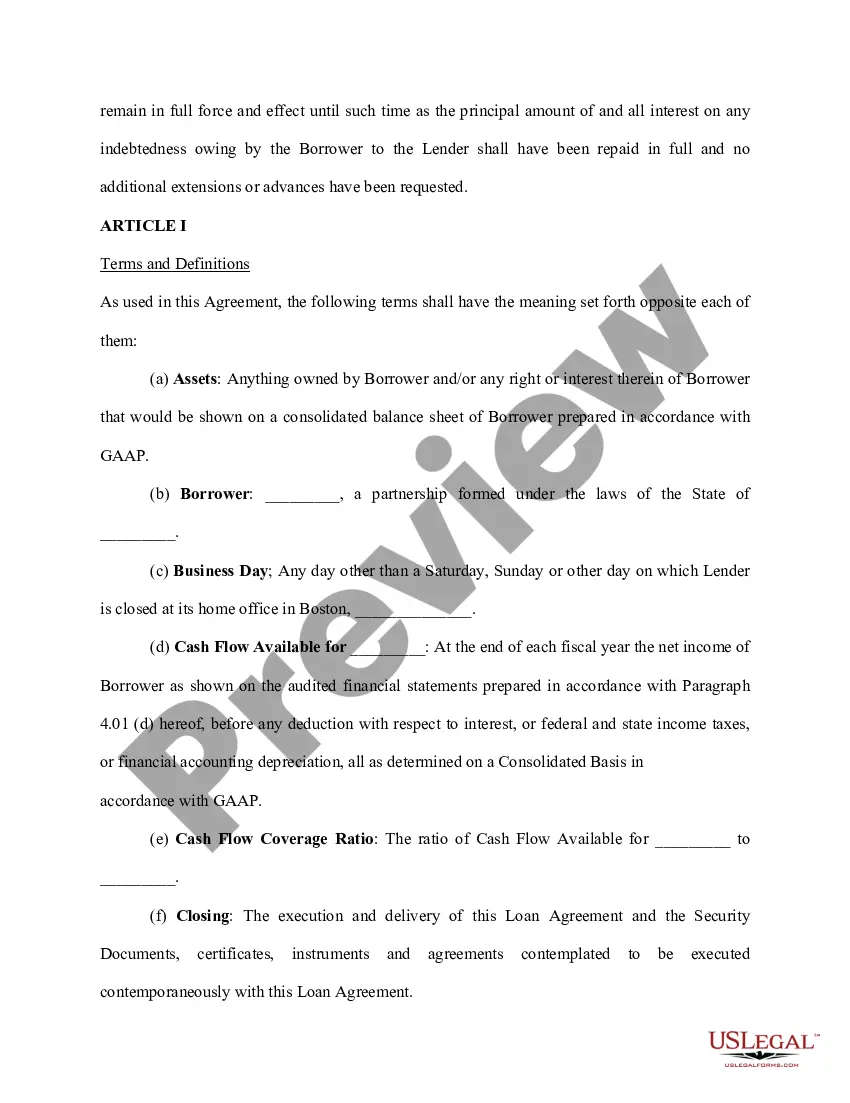

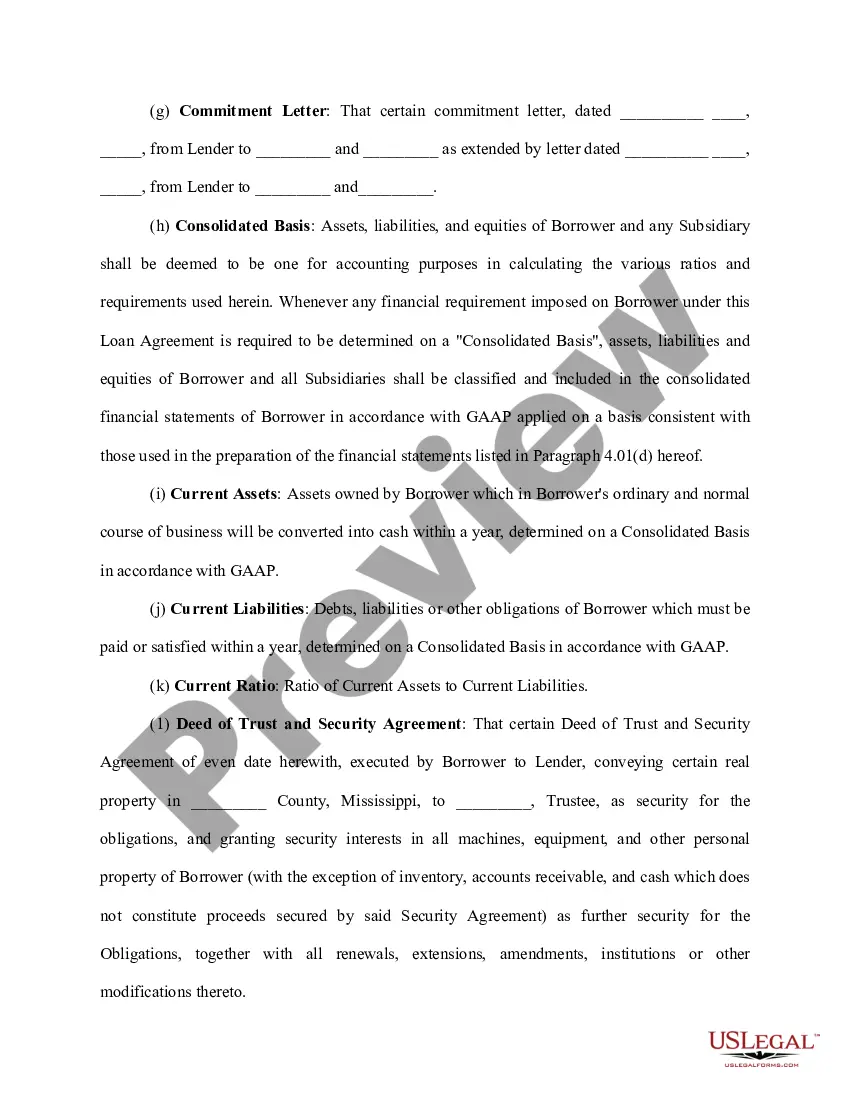

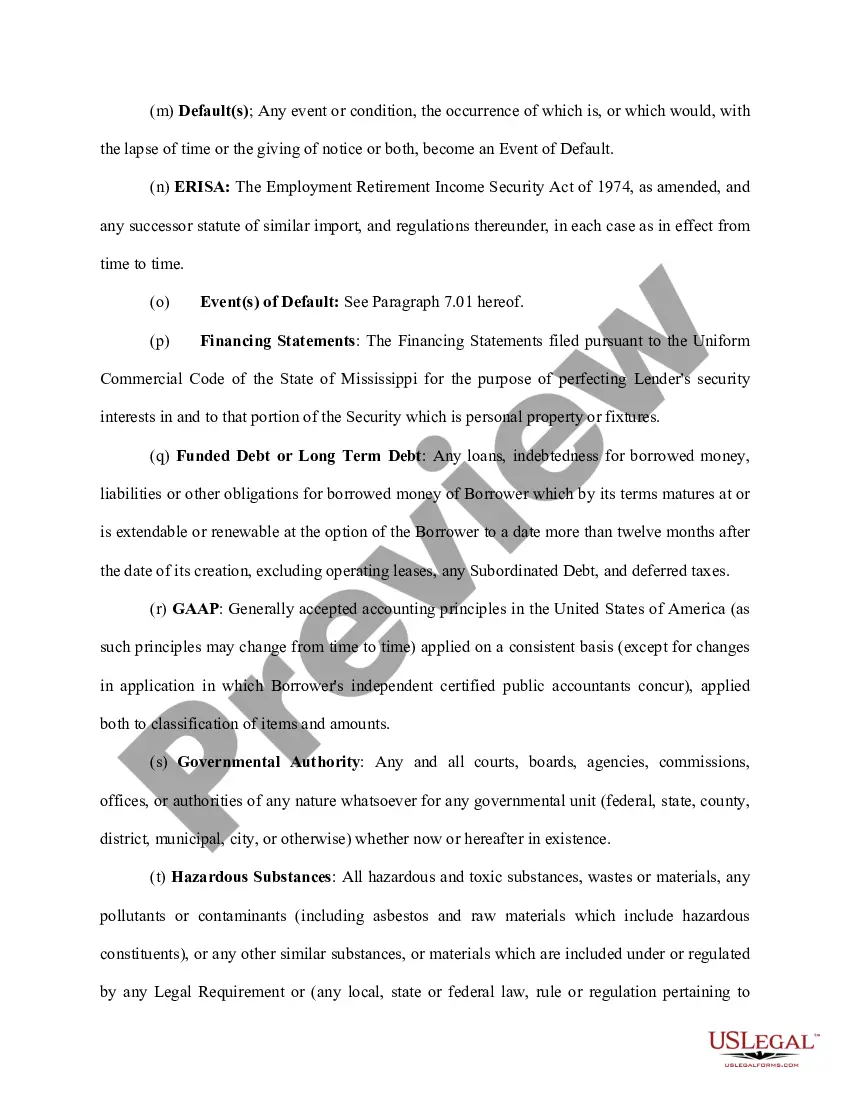

A New Jersey Loan Agreement for Family Member is a legally binding document that outlines the terms and conditions of a loan between family members residing in the state of New Jersey. This agreement ensures that both the borrower and the lender are protected and sets clear expectations for repayment. In New Jersey, there are various types of Loan Agreements for Family Members that can be customized based on the specific needs of the parties involved. 1. Promissory Note: This type of loan agreement is the most common and straightforward option. It includes essential details such as the loan amount, interest rate (if applicable), repayment schedule, and any collateral provided as security for the loan. The promissory note creates a legal obligation for the borrower to repay the loan according to the agreed terms. 2. Forgivable Loan Agreement: This type of loan agreement is often used when a family member intends to forgive a portion or the entire loan amount over time. It outlines the conditions under which the loan can be forgiven, such as meeting specific milestones or fulfilling certain obligations. This agreement ensures that both parties have a shared understanding of the forgiveness conditions. 3. Interfamily Mortgage Loan: In certain instances, a family member may loan money to another family member for the purpose of purchasing or refinancing a property. In such cases, an interfamily mortgage loan agreement is required. This agreement functions similarly to a traditional mortgage, with specific terms related to interest rates, repayment schedules, and potential foreclosure procedures. 4. Revolving Loan Agreement: A revolving loan agreement allows a family member to borrow from a predetermined credit limit multiple times within a specified period. This type of loan agreement is often useful when the borrower expects to require funds periodically. The agreement outlines the terms for borrowing and repaying funds, and the available credit limit is replenished as the borrower repays the loan. Regardless of the type of New Jersey Loan Agreement for Family Member, it is crucial to include important elements such as the identities of both parties, the loan amount, the repayment schedule, interest rates (if applicable), any collateral provided, and any additional terms and conditions mutually agreed upon. Creating a comprehensive Loan Agreement for Family Members ensures a clear understanding between parties involved, minimizes potential conflicts, and provides legal protection in case of disputes. It is advisable to consult with a legal professional to ensure that the agreement complies with all applicable laws and adequately protects the interests of both parties.

New Jersey Loan Agreement for Family Member

Description

How to fill out New Jersey Loan Agreement For Family Member?

Finding the right legal file format might be a battle. Of course, there are a variety of web templates available on the Internet, but how would you obtain the legal kind you need? Make use of the US Legal Forms web site. The services gives a huge number of web templates, like the New Jersey Loan Agreement for Family Member, that you can use for enterprise and private demands. Every one of the types are inspected by experts and meet federal and state needs.

In case you are presently signed up, log in in your accounts and click the Down load button to obtain the New Jersey Loan Agreement for Family Member. Use your accounts to search through the legal types you may have purchased in the past. Proceed to the My Forms tab of your respective accounts and acquire one more duplicate of the file you need.

In case you are a fresh customer of US Legal Forms, here are easy guidelines so that you can adhere to:

- First, ensure you have selected the right kind for your personal area/state. You are able to examine the shape utilizing the Review button and read the shape outline to guarantee this is the best for you.

- In the event the kind will not meet your expectations, utilize the Seach industry to get the appropriate kind.

- When you are positive that the shape is suitable, click the Purchase now button to obtain the kind.

- Select the pricing prepare you desire and enter in the required info. Make your accounts and pay for your order using your PayPal accounts or credit card.

- Opt for the data file format and acquire the legal file format in your device.

- Comprehensive, edit and print out and indication the received New Jersey Loan Agreement for Family Member.

US Legal Forms may be the biggest library of legal types in which you can discover various file web templates. Make use of the company to acquire expertly-created documents that adhere to condition needs.