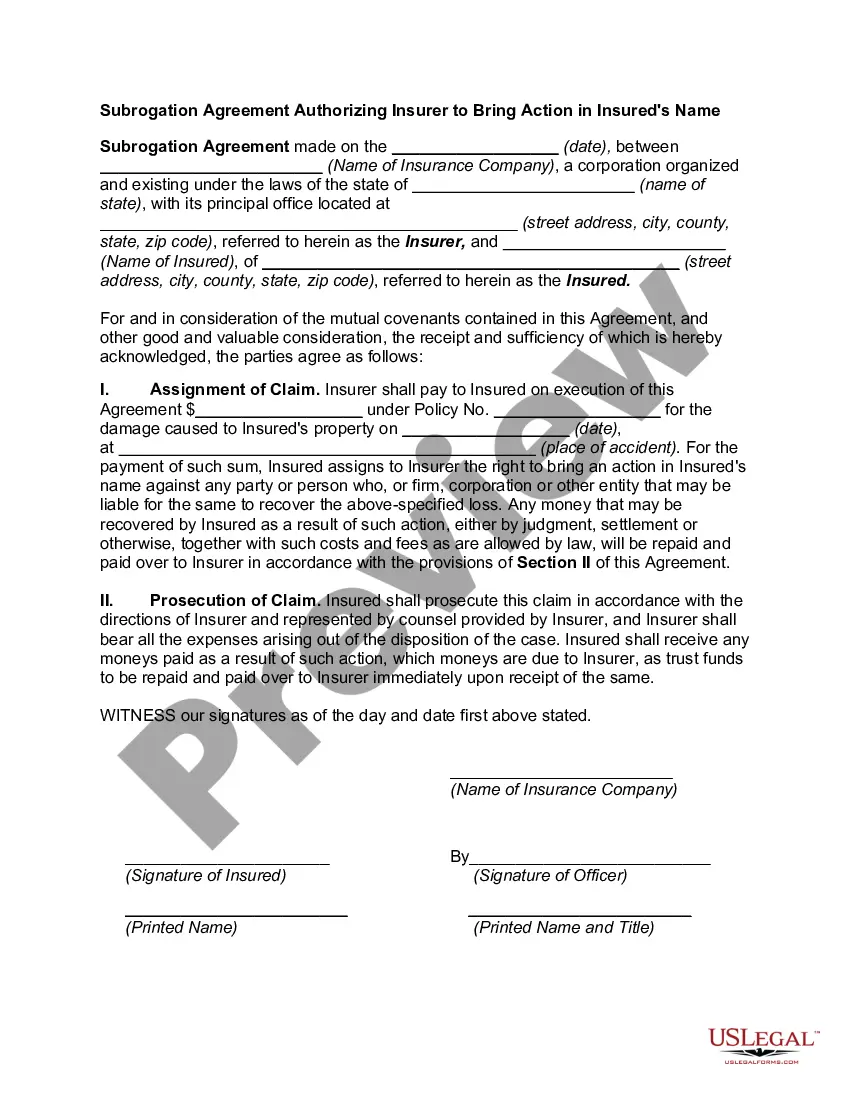

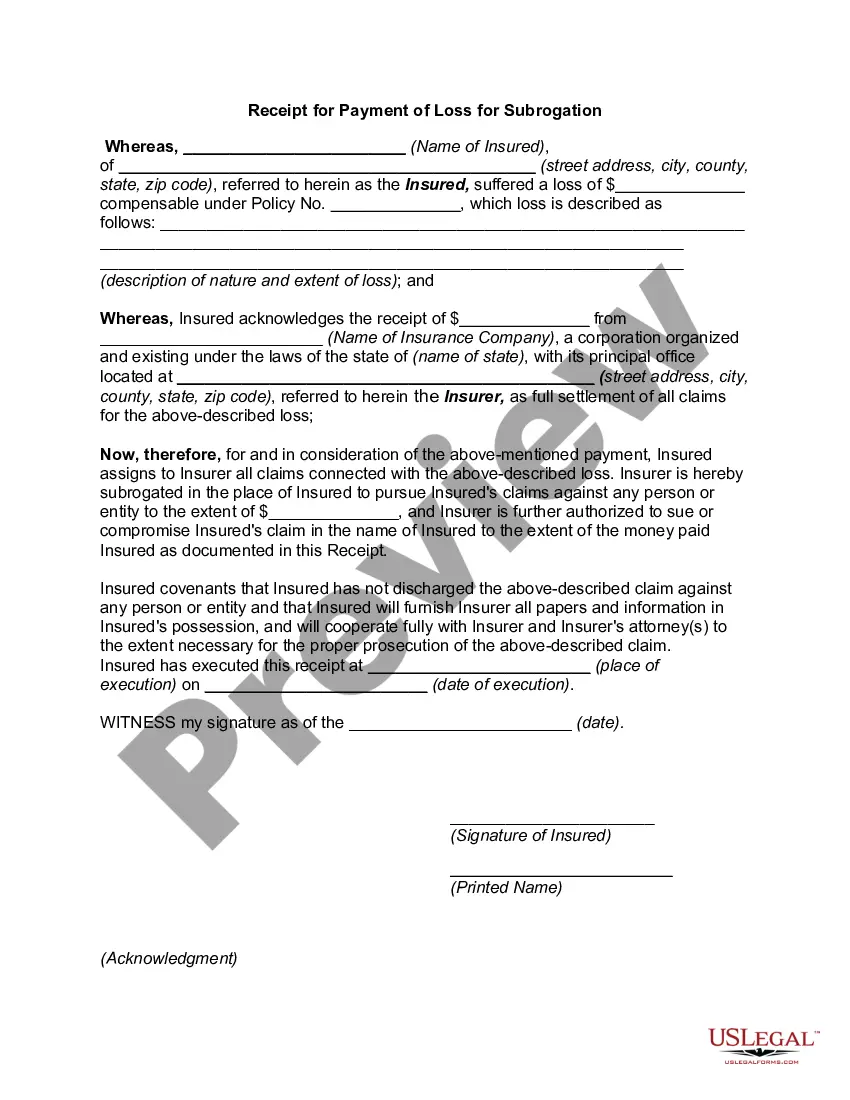

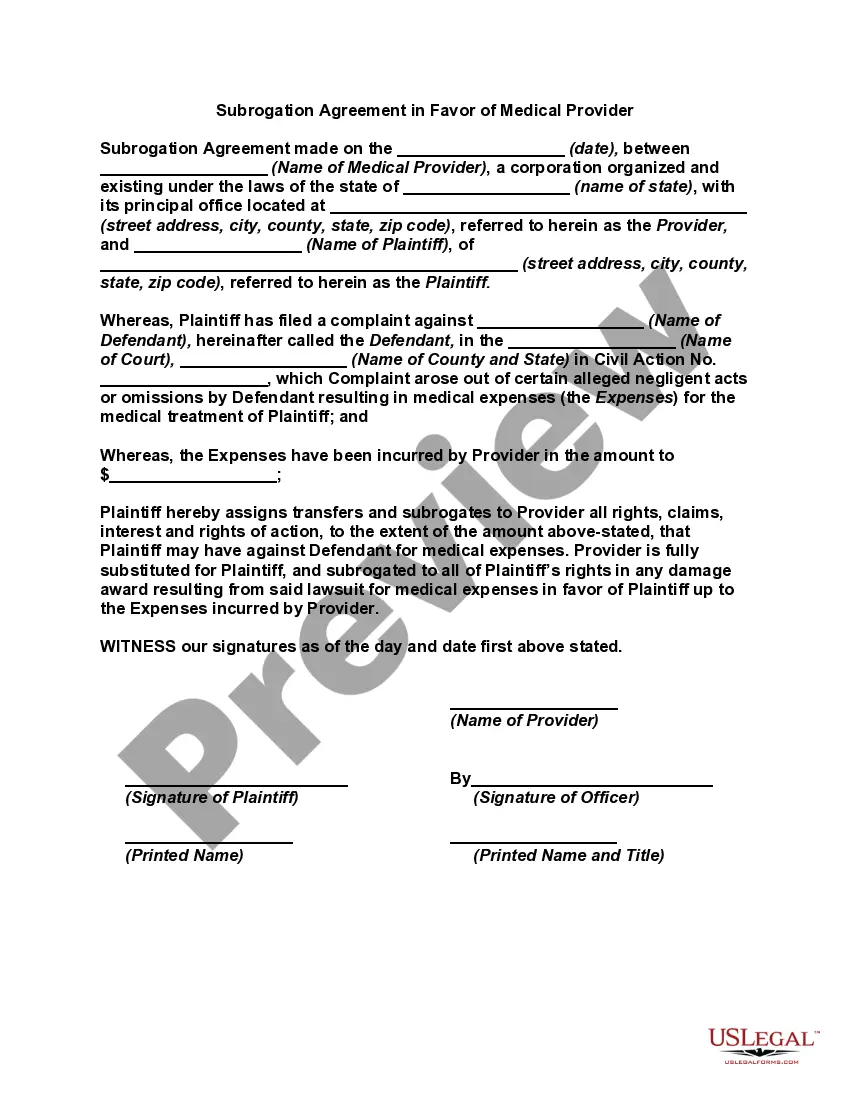

New Jersey Subrogation Agreement between Insurer and Insured

Description

How to fill out Subrogation Agreement Between Insurer And Insured?

US Legal Forms - among the largest libraries of lawful varieties in the States - offers a wide array of lawful file templates you can download or produce. Utilizing the site, you can find thousands of varieties for organization and specific uses, sorted by classes, suggests, or keywords.You can find the newest versions of varieties much like the New Jersey Subrogation Agreement between Insurer and Insured in seconds.

If you currently have a membership, log in and download New Jersey Subrogation Agreement between Insurer and Insured from the US Legal Forms catalogue. The Download switch can look on each develop you perspective. You get access to all formerly saved varieties within the My Forms tab of your accounts.

If you wish to use US Legal Forms initially, here are straightforward instructions to obtain began:

- Be sure to have picked out the proper develop for the area/region. Go through the Review switch to review the form`s content. See the develop explanation to ensure that you have selected the proper develop.

- In case the develop does not satisfy your needs, use the Lookup discipline near the top of the display to obtain the one who does.

- When you are pleased with the form, validate your decision by simply clicking the Buy now switch. Then, pick the rates prepare you want and offer your accreditations to register on an accounts.

- Approach the deal. Use your bank card or PayPal accounts to accomplish the deal.

- Select the structure and download the form in your system.

- Make adjustments. Load, edit and produce and sign the saved New Jersey Subrogation Agreement between Insurer and Insured.

Each and every template you included with your money lacks an expiry particular date and it is the one you have for a long time. So, in order to download or produce another copy, just visit the My Forms portion and click on around the develop you want.

Obtain access to the New Jersey Subrogation Agreement between Insurer and Insured with US Legal Forms, by far the most comprehensive catalogue of lawful file templates. Use thousands of specialist and status-certain templates that meet your small business or specific needs and needs.

Form popularity

FAQ

"Subrogation," or "subro" for short, refers to the right your insurance company holds under your policy ? after they've paid a covered claim ? to request reimbursement from the at-fault party. This reimbursement often comes from the at-fault party's insurance company.

January 23, 2020. Recently, Judge Sheridan of the District of New Jersey rejected a waiver of subrogation in a residential solar contract, finding that the contract was one of adhesion and that the waiver was against public interest. New Jersey Manufacturers Insurance Group v.

January 23, 2020. Recently, Judge Sheridan of the District of New Jersey rejected a waiver of subrogation in a residential solar contract, finding that the contract was one of adhesion and that the waiver was against public interest. New Jersey Manufacturers Insurance Group v.

Not all states agree with this interpretation, and the actual effect of a valid waiver of subrogation varies from state to state, with most states still undecided one way or the other.

An insurance company may not subrogate against its own insured or a co-insured. However, when a party claiming to be a co-insured is merely a loss payee to which no liability coverage is afforded, subrogation is permissible.

A waiver of subrogation means that an insurance company has a higher chance of paying out losses that it cannot recover itself. Therefore, an insurance company must charge more if the insured plans on agreeing to this clause. A waiver of subrogation is common in the construction and real estate industries.

The anti-subrogation rule (ASR) is a common law defense, which provides that a subrogated insurer standing in the shoes of an insured cannot bring a recovery action against or sue its own insured. See Davis v. Heinz, 254 A.D.2d 830 (4th Dep't 1998).