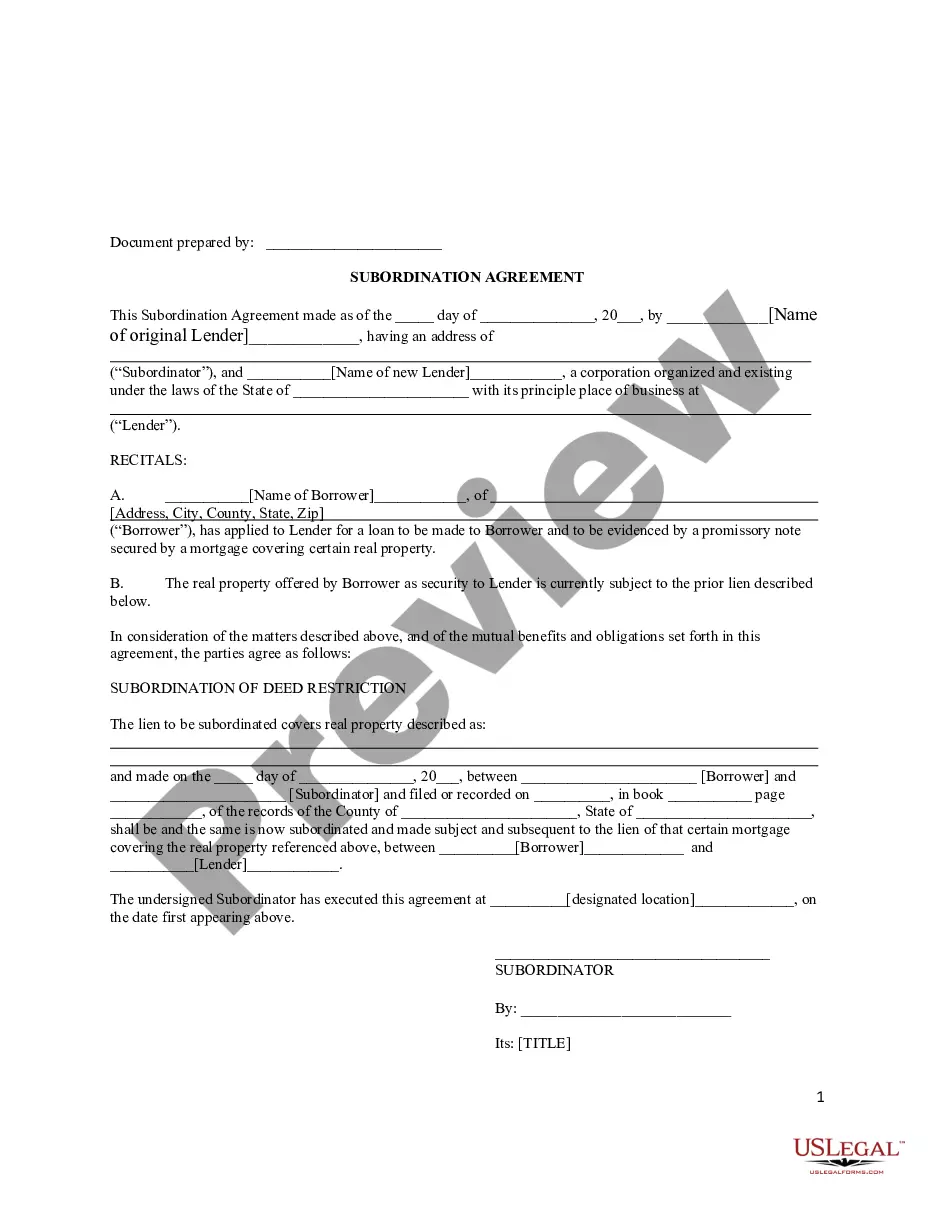

New Jersey Subordination Agreement Subordinating Existing Mortgage to New Mortgage

Description

How to fill out Subordination Agreement Subordinating Existing Mortgage To New Mortgage?

You can spend hrs on the web trying to find the authorized papers web template which fits the federal and state needs you require. US Legal Forms supplies a large number of authorized types which can be examined by professionals. It is simple to acquire or produce the New Jersey Subordination Agreement Subordinating Existing Mortgage to New Mortgage from your assistance.

If you currently have a US Legal Forms account, you are able to log in and click the Download switch. After that, you are able to full, modify, produce, or signal the New Jersey Subordination Agreement Subordinating Existing Mortgage to New Mortgage. Each authorized papers web template you acquire is the one you have permanently. To get another duplicate associated with a obtained kind, proceed to the My Forms tab and click the related switch.

Should you use the US Legal Forms site initially, keep to the basic directions beneath:

- Initial, make sure that you have chosen the right papers web template for your region/town of your choosing. Browse the kind information to make sure you have selected the proper kind. If accessible, make use of the Preview switch to appear throughout the papers web template as well.

- In order to locate another variation in the kind, make use of the Lookup discipline to get the web template that fits your needs and needs.

- Once you have found the web template you need, click on Get now to continue.

- Select the pricing plan you need, type in your credentials, and sign up for an account on US Legal Forms.

- Total the transaction. You can utilize your bank card or PayPal account to pay for the authorized kind.

- Select the file format in the papers and acquire it in your gadget.

- Make modifications in your papers if needed. You can full, modify and signal and produce New Jersey Subordination Agreement Subordinating Existing Mortgage to New Mortgage.

Download and produce a large number of papers layouts making use of the US Legal Forms web site, that offers the biggest collection of authorized types. Use expert and state-specific layouts to take on your company or person requires.

Form popularity

FAQ

8) Keep the original signed subordination agreement in your file to be given to your title agent to record AT THE SAME TIME they record the RIM easement. Do not record the mortgage subordination agreement ahead of easement recording.

Again, if you're refinancing your first mortgage and the property also has a subordinate mortgage, the refinancing lender will usually handle the process of getting the necessary subordination agreement. But you need to ensure that the required subordination agreement is completed before the new loan's closing date.

Getting A Second Mortgage A second mortgage will become a subordinate loan. If you repay the primary loan within the term of the second mortgage, the second mortgage can take its place as the primary loan.

A subordinated loan agreement (SLA) must be filed with NFA at least ten days prior to the proposed effective date of the agreement.

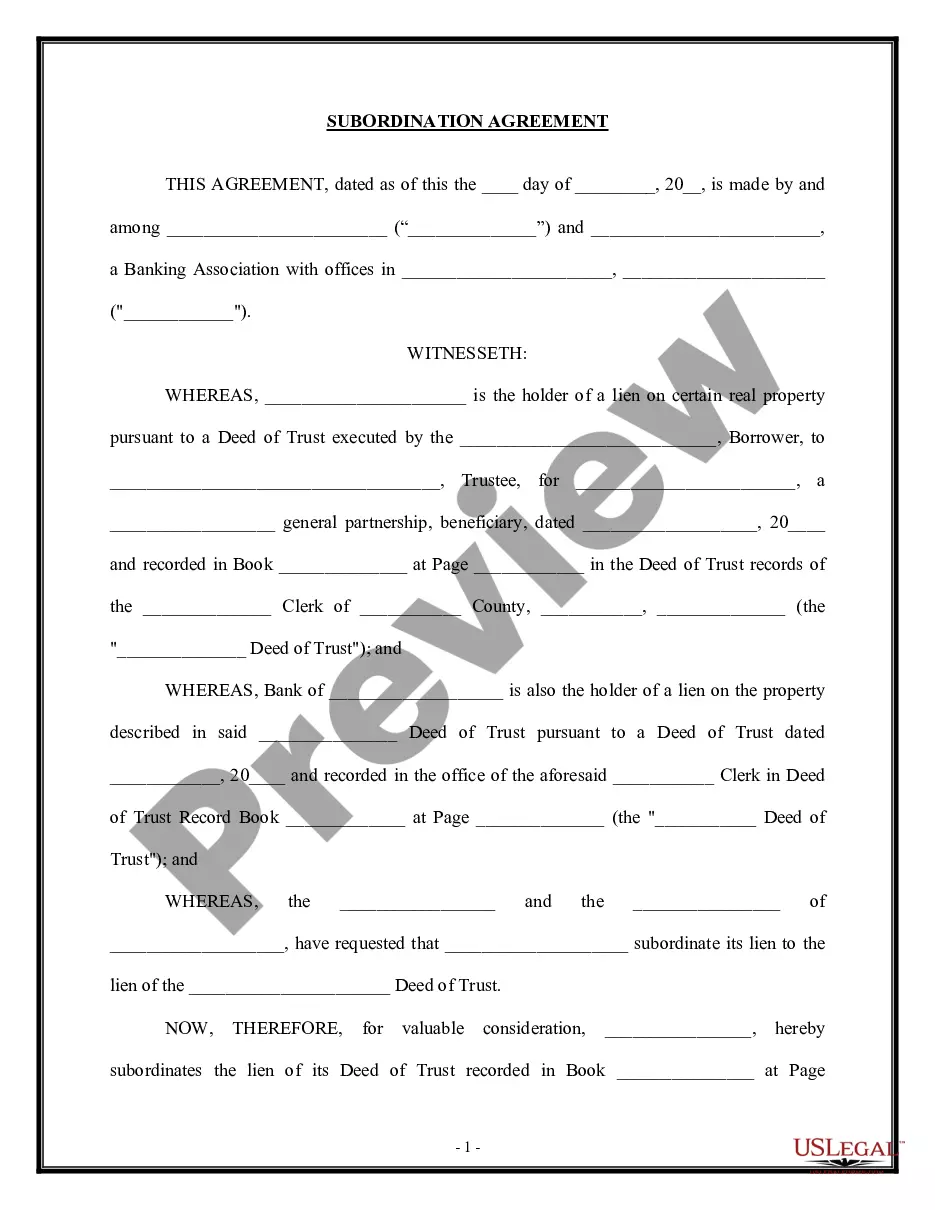

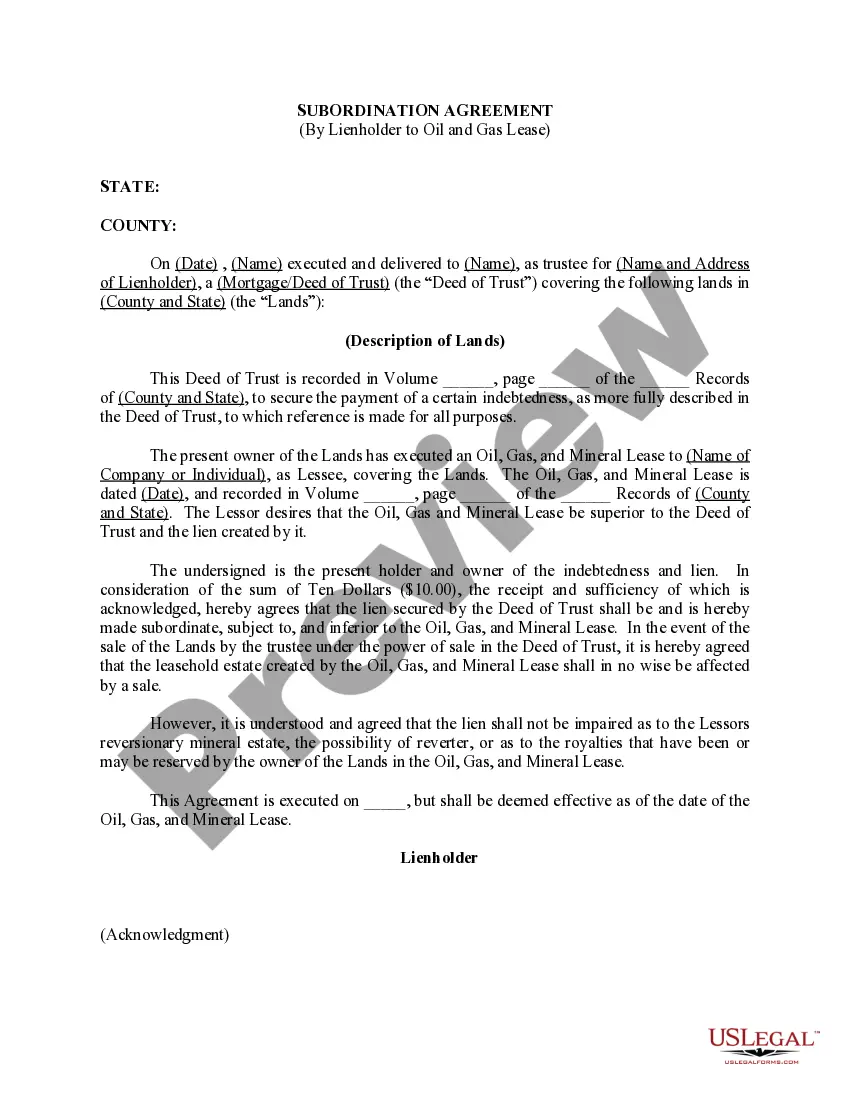

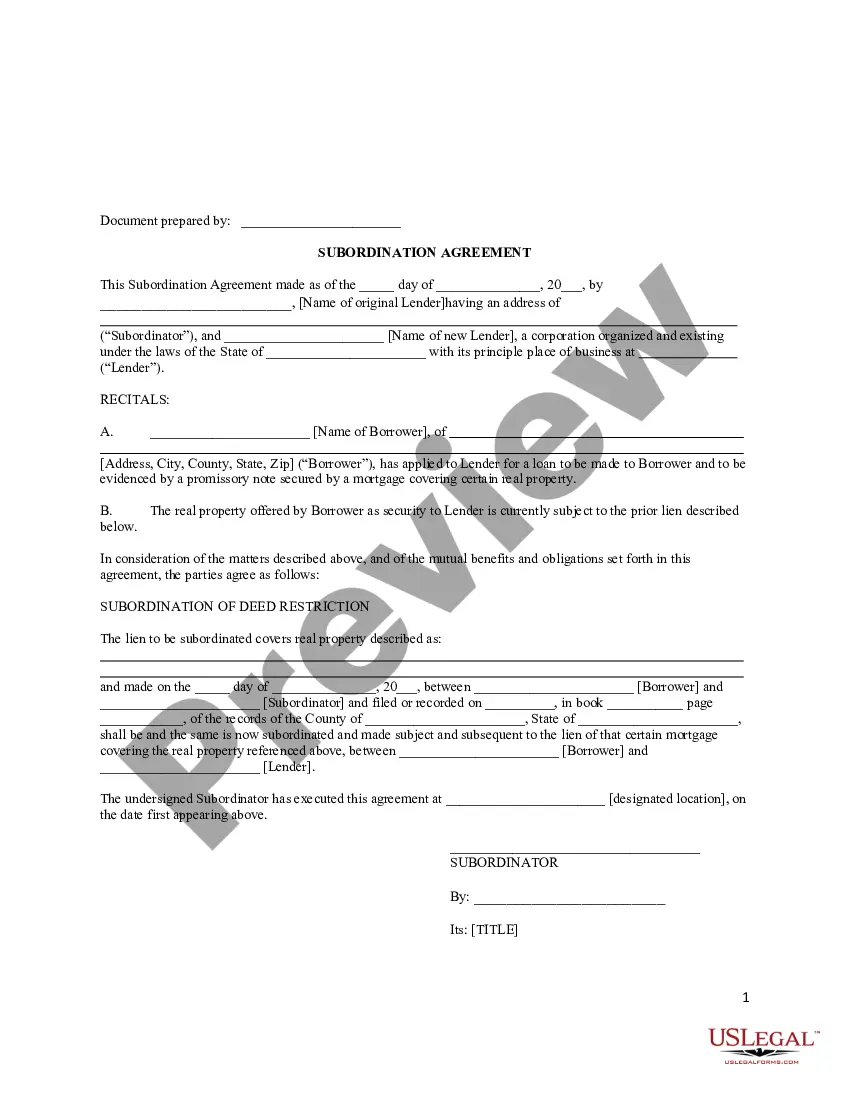

Subordination agreements are used to legally establish the order in which debts are to be repaid in the event of a foreclosure or bankruptcy. In return for the agreement, the lender with the subordinated debt will be compensated in some manner for the additional risk.

The order of subordination is determined based on the type of loan against your property. If you only have one home mortgage and no other liens, you'll find that mortgage subordination won't come into play until you have more than one lien on your home.

A subordination agreement prioritizes debts, ranking one behind another for purposes of collecting repayment from a debtor in the event of foreclosure or bankruptcy. A second-in-line creditor collects only when and if the priority creditor has been fully paid.

Many people have a subordinate mortgage in the form of a home equity line of credit or home equity loan. A subordinate mortgage is secured by your property but sits in second position, if you have a primary mortgage, for getting paid in the event you default.