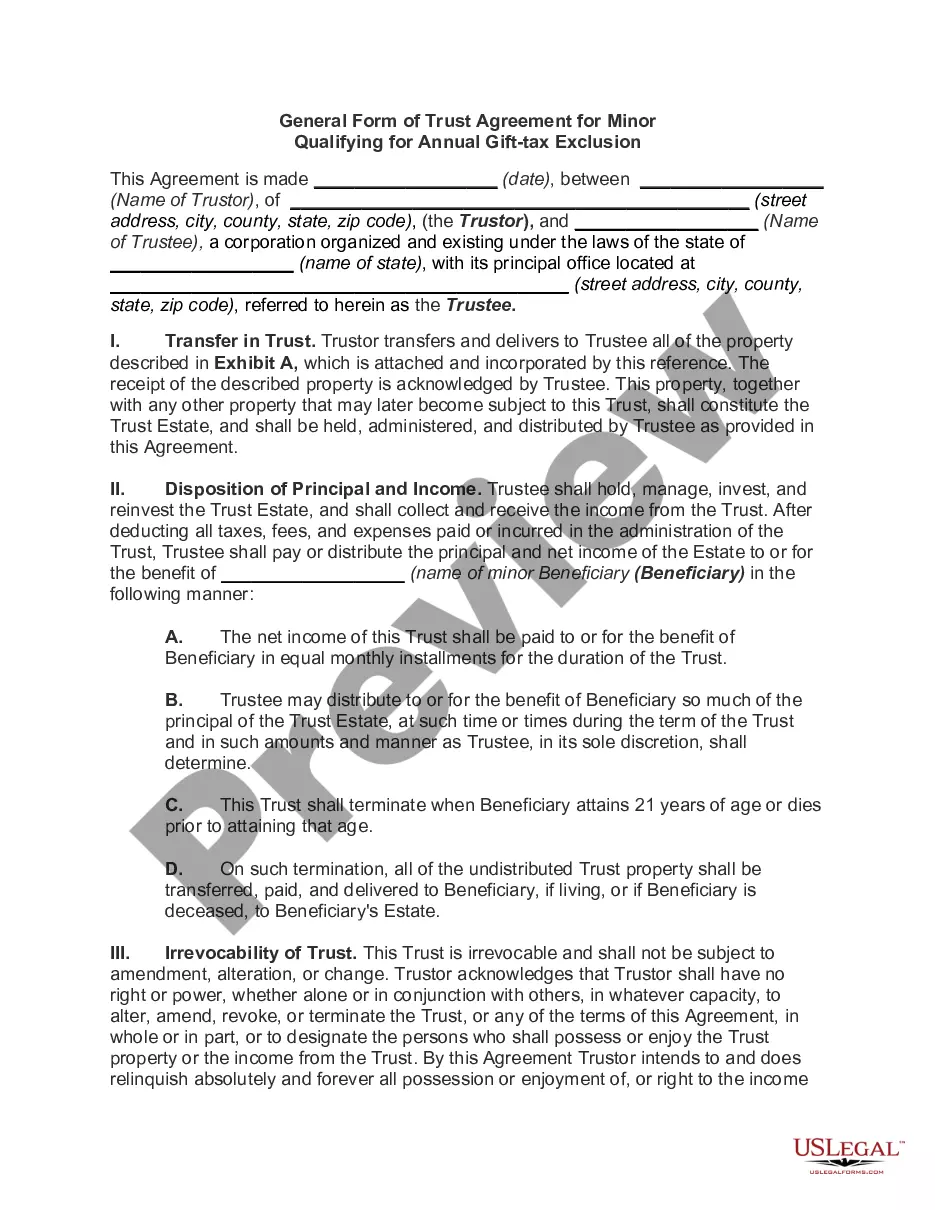

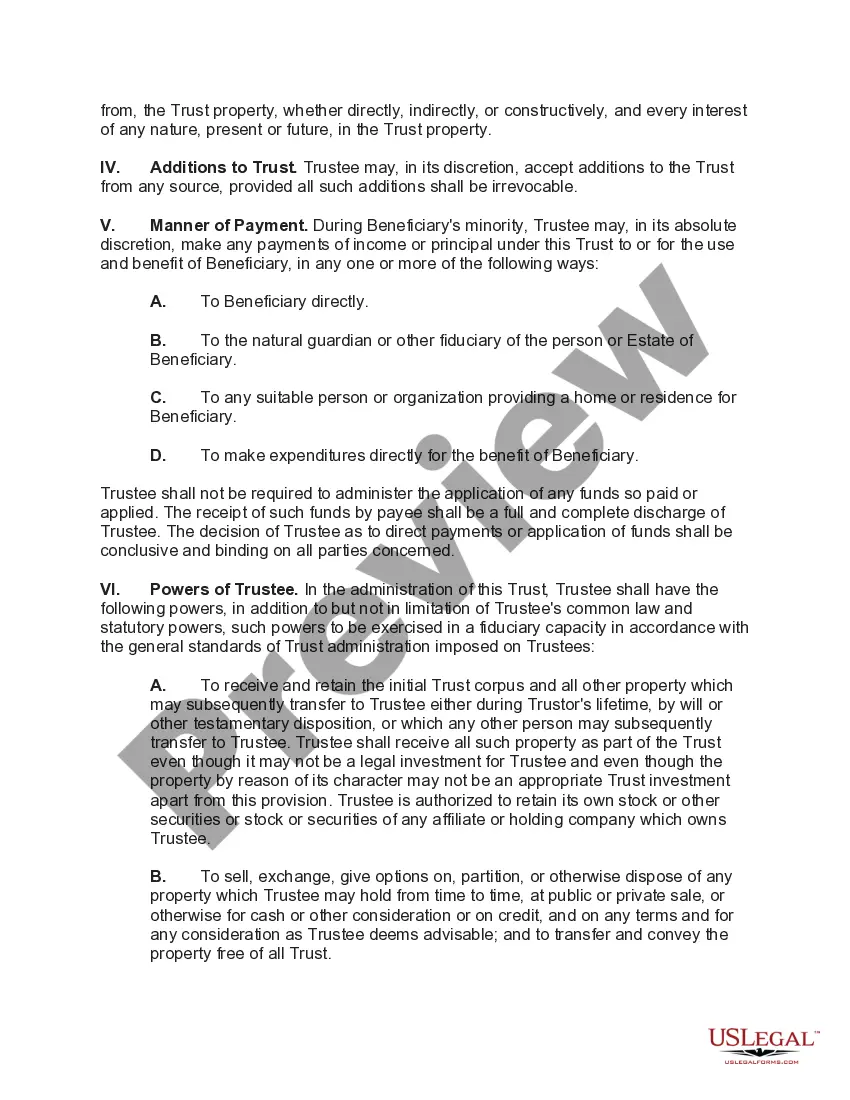

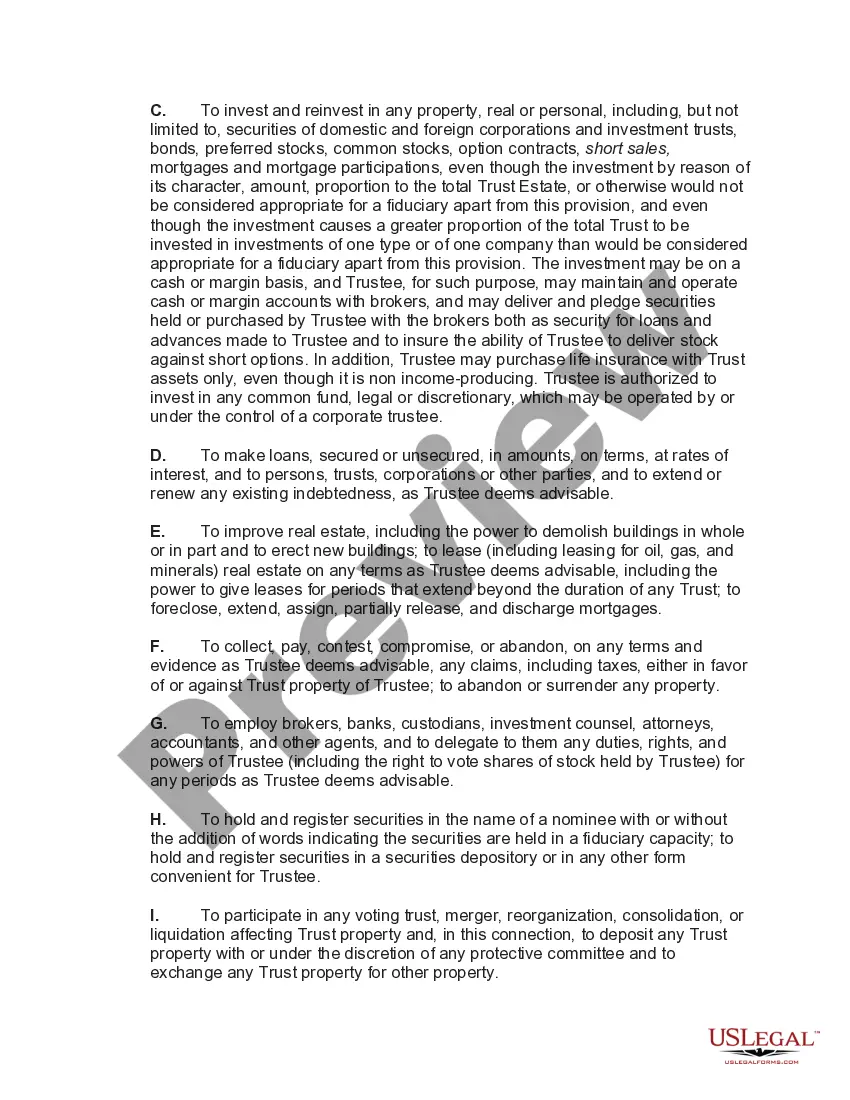

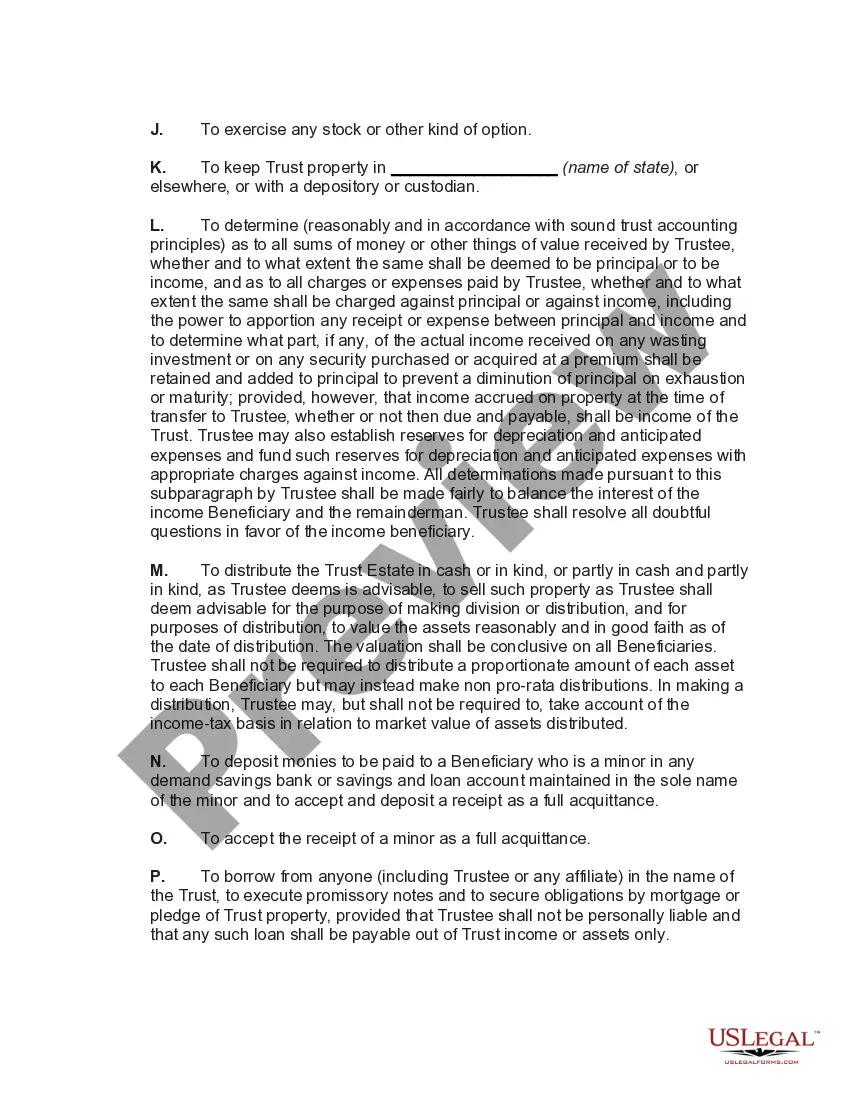

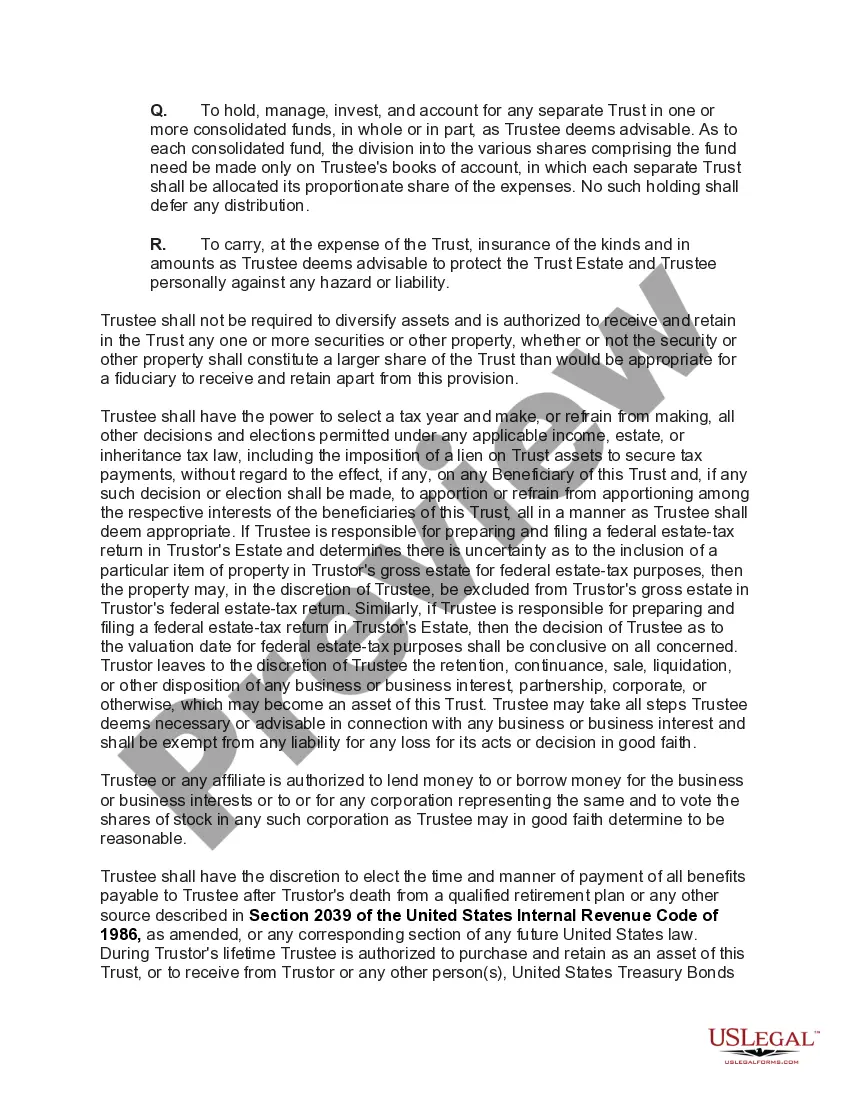

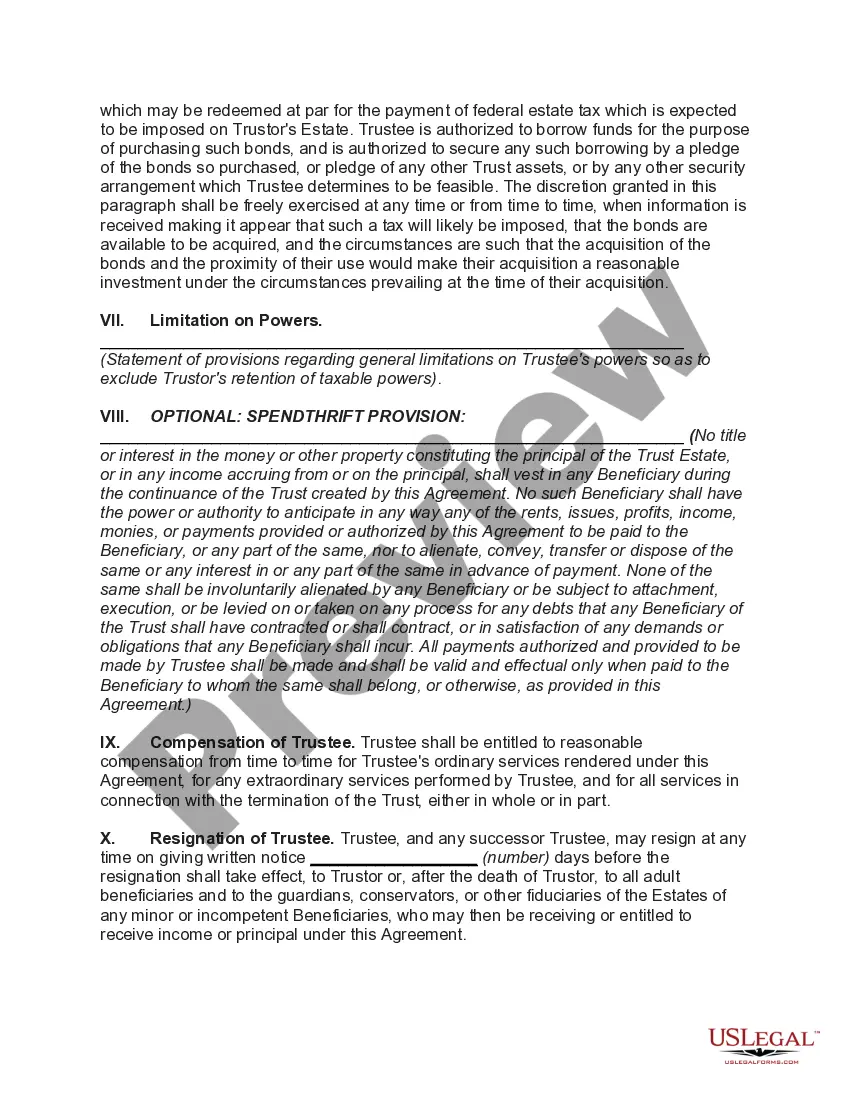

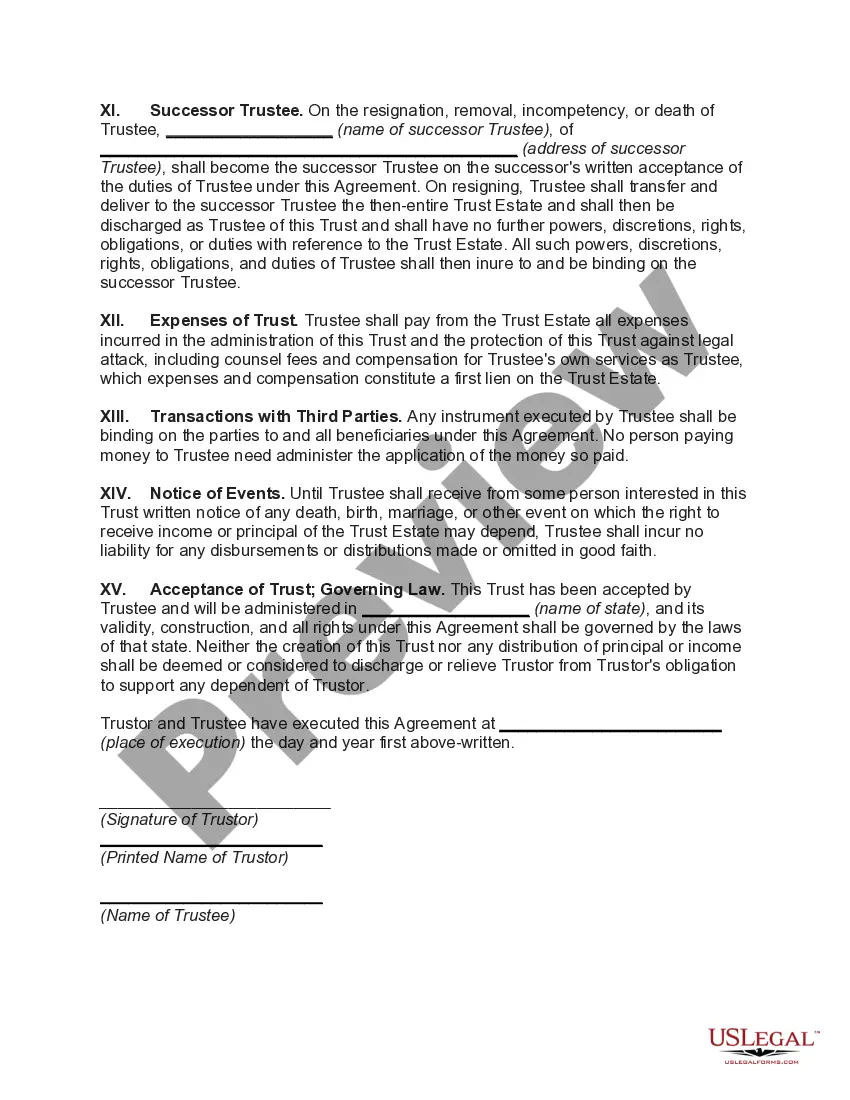

The New Jersey General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion is a legal document that enables individuals to establish a trust for a minor child, while also taking advantage of the annual gift tax exclusion. This type of trust allows individuals to pass on assets to minors without incurring gift tax consequences, up to a certain annual limit. One type of New Jersey General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion is the Crummy Trust. Named after the landmark case Crummy v. Commissioner, this trust incorporates a provision that allows the beneficiary (minor child) to withdraw the gifted assets within a specified time frame, typically 30 days. This "Crummy power of withdrawal" ensures that the gifted assets meet the requirements for qualifying for the annual gift tax exclusion. Another type of New Jersey General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion is the 2503© Trust. This trust is based on Section 2503(c) of the Internal Revenue Code and is specifically designed to qualify for the annual gift tax exclusion. It provides the trustee with discretion to distribute income and/or principal for the minor child's benefit, but generally restricts distributions until the child reaches a certain age, such as 21 or 25. The New Jersey General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion ensures that individuals can transfer assets to a trust for the benefit of a minor child and avoid immediate gift tax consequences. This type of trust offers flexibility in terms of the trustee's discretionary powers and the timing of distributions. By utilizing this trust agreement, individuals can create a valuable estate planning tool to provide financial support and security for their minor children while minimizing potential gift tax liabilities.

New Jersey General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion

Description

How to fill out New Jersey General Form Of Trust Agreement For Minor Qualifying For Annual Gift Tax Exclusion?

If you want to complete, down load, or print legal papers layouts, use US Legal Forms, the most important selection of legal varieties, that can be found on-line. Make use of the site`s easy and hassle-free search to get the papers you will need. A variety of layouts for organization and individual reasons are sorted by groups and says, or keywords. Use US Legal Forms to get the New Jersey General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion within a number of mouse clicks.

When you are already a US Legal Forms customer, log in for your accounts and click the Acquire button to obtain the New Jersey General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion. You can also accessibility varieties you previously acquired from the My Forms tab of your respective accounts.

Should you use US Legal Forms the very first time, follow the instructions under:

- Step 1. Be sure you have selected the shape for the appropriate area/land.

- Step 2. Use the Preview option to check out the form`s articles. Never forget to learn the description.

- Step 3. When you are unsatisfied with all the kind, utilize the Search area near the top of the screen to discover other versions from the legal kind format.

- Step 4. Once you have discovered the shape you will need, select the Purchase now button. Pick the costs program you choose and put your qualifications to sign up on an accounts.

- Step 5. Process the deal. You can use your bank card or PayPal accounts to perform the deal.

- Step 6. Select the format from the legal kind and down load it on the gadget.

- Step 7. Complete, edit and print or indicator the New Jersey General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion.

Every single legal papers format you buy is the one you have permanently. You have acces to every single kind you acquired within your acccount. Click the My Forms segment and choose a kind to print or down load once more.

Be competitive and down load, and print the New Jersey General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion with US Legal Forms. There are many professional and state-specific varieties you may use for the organization or individual needs.