New Jersey Sample Letter for Insufficient Amount to Reinstate Loan

Description

How to fill out Sample Letter For Insufficient Amount To Reinstate Loan?

Selecting the optimal legal document template can be challenging. Clearly, there are numerous templates accessible online, but how do you find the legal form you need? Utilize the US Legal Forms website.

The service offers a wide array of templates, including the New Jersey Sample Letter for Insufficient Amount to Reinstate Loan, which can serve both business and personal purposes. All forms are reviewed by experts and comply with federal and state regulations.

If you are already registered, Log In to your account and click on the Download button to obtain the New Jersey Sample Letter for Insufficient Amount to Reinstate Loan. Use your account to check the legal forms you have acquired previously. Go to the My documents section of your account to retrieve another copy of the document you need.

Complete, modify, print, and sign the obtained New Jersey Sample Letter for Insufficient Amount to Reinstate Loan. US Legal Forms is the largest repository of legal forms where you can find a variety of document templates. Utilize this service to acquire professionally crafted documents that adhere to state requirements.

- If you are a new customer of US Legal Forms, here are simple steps to follow.

- First, ensure you have selected the correct form for your area/county. You can browse the form using the Preview button and read the form description to confirm it’s appropriate for you.

- If the form doesn’t meet your needs, use the Search field to find the correct form.

- Once you are certain that the form is suitable, click the Get now button to obtain the form.

- Choose the pricing plan you prefer and enter the required information. Create your account and pay for the order using your PayPal account or Visa or Mastercard.

- Select the document format and download the legal document template to your device.

Form popularity

FAQ

To write a professional letter of request, be clear and concise in your communication. Start with a formal greeting, state your request early, and provide justifications as needed. If your request relates to loans, consider utilizing a 'New Jersey Sample Letter for Insufficient Amount to Reinstate Loan' to ensure that your letter adheres to expectations and conveys your intent effectively.

A convincing letter for rehire should express genuine interest in returning to the company. Highlight your previous contributions, any new skills acquired, and the value you can bring back. Integrating references to a 'New Jersey Sample Letter for Insufficient Amount to Reinstate Loan' might help in crafting a structured letter that conveys your commitment and professionalism.

When writing a letter to reinstate an employee, clearly state the reasons for their reinstatement. Include any relevant dates, obligations, and conditions associated with their return. For those managing financial reinstatement processes, seeking a 'New Jersey Sample Letter for Insufficient Amount to Reinstate Loan' could be useful, as it shares the format and language for formal reinstatement communication.

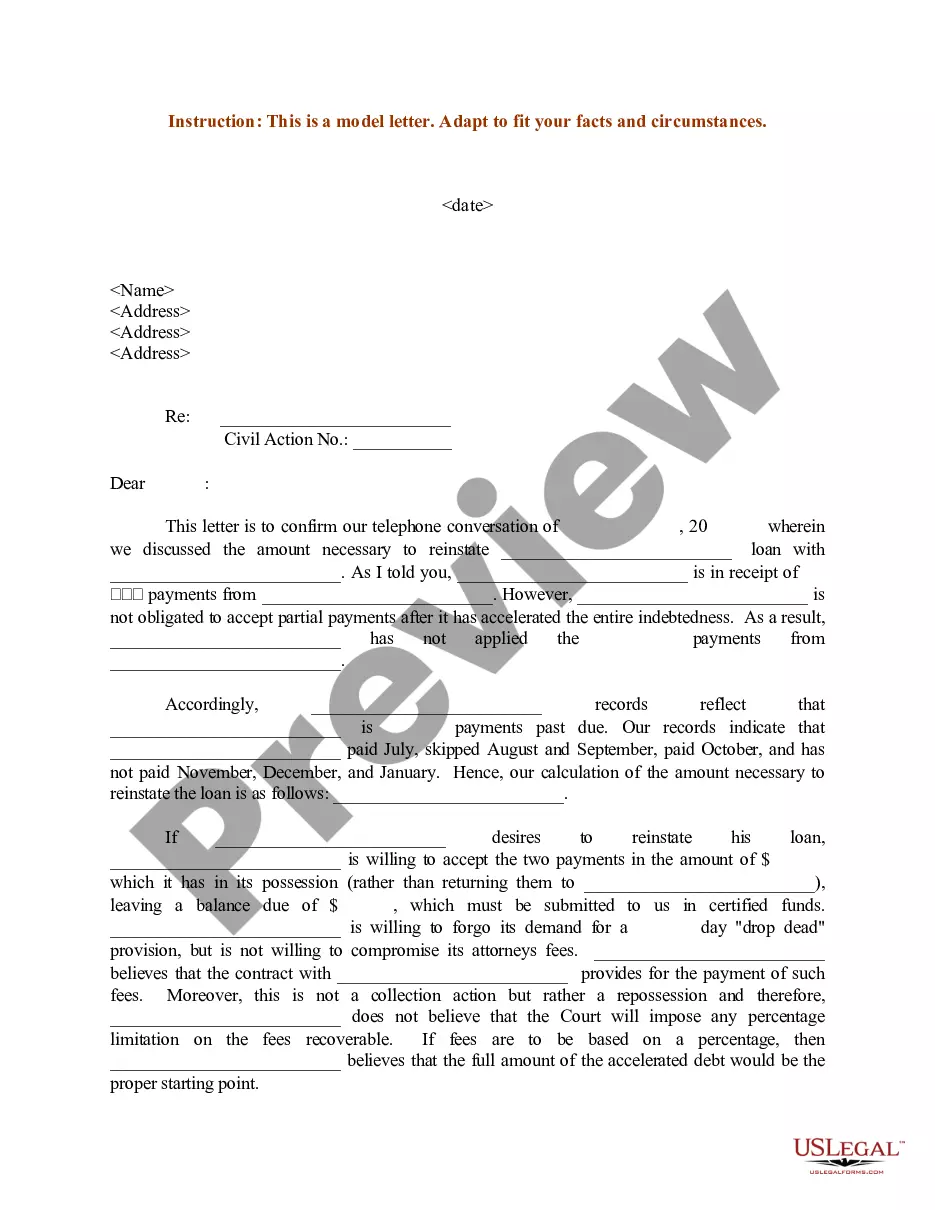

Writing a personal statement for reinstatement involves explaining your situation transparently. Discuss your financial circumstances that led to your loan being in default, and outline your current position and willingness to correct the issue. Referring to a 'New Jersey Sample Letter for Insufficient Amount to Reinstate Loan' can provide a template that highlights essential components of your statement.

To write a letter of request for reinstatement, start by clearly stating your intention to reinstate your loan. Include specific details such as your loan number, the amount owed, and the reason for your request. It's beneficial to refer to a 'New Jersey Sample Letter for Insufficient Amount to Reinstate Loan' to ensure you cover all necessary points and maintain professionalism.

Reinstating your business in New Jersey involves several key steps, including paying any past due taxes and fees. You may also need to draft and submit a New Jersey Sample Letter for Insufficient Amount to Reinstate Loan, detailing your circumstances and intentions. It’s important to gather all necessary documentation to ensure a smooth process. USLegalForms can assist by providing you with the proper forms and guidance to make the reinstatement easier.

To find out if a business is active in New Jersey, you can search the New Jersey Division of Revenue and Enterprise Services online database. Simply enter the business name or identification number to retrieve its status. If you discover that a business is inactive or suspended, utilizing a New Jersey Sample Letter for Insufficient Amount to Reinstate Loan can be the next step toward resolving its status. USLegalForms provides templates and support for these situations.

To reinstate a suspended license in New Jersey, first, determine the reason for the suspension and fulfill any required obligations, such as paying fines or completing educational programs. You may need to submit a New Jersey Sample Letter for Insufficient Amount to Reinstate Loan if your financial circumstances are tied to the suspension. Always check your status through the New Jersey Motor Vehicle Commission's website for guidance, and consider USLegalForms to simplify paperwork.

Reactivating a business often involves addressing any reasons that led to its suspension or inactivity. Typically, you may need to file specific forms with the state and possibly submit a New Jersey Sample Letter for Insufficient Amount to Reinstate Loan. It’s essential to check your business's status online and ensure all financial obligations are met before taking further steps. Utilizing tools from USLegalForms can support you in compiling the right documents.

To reinstate a business in New Jersey, you must first ensure that you have resolved any outstanding issues, such as overdue taxes or penalties. Then, you need to submit a New Jersey Sample Letter for Insufficient Amount to Reinstate Loan to the appropriate state department. This letter will help outline your intentions and provide any necessary documentation for your business's reinstatement. Consider using resources from USLegalForms to streamline this process.