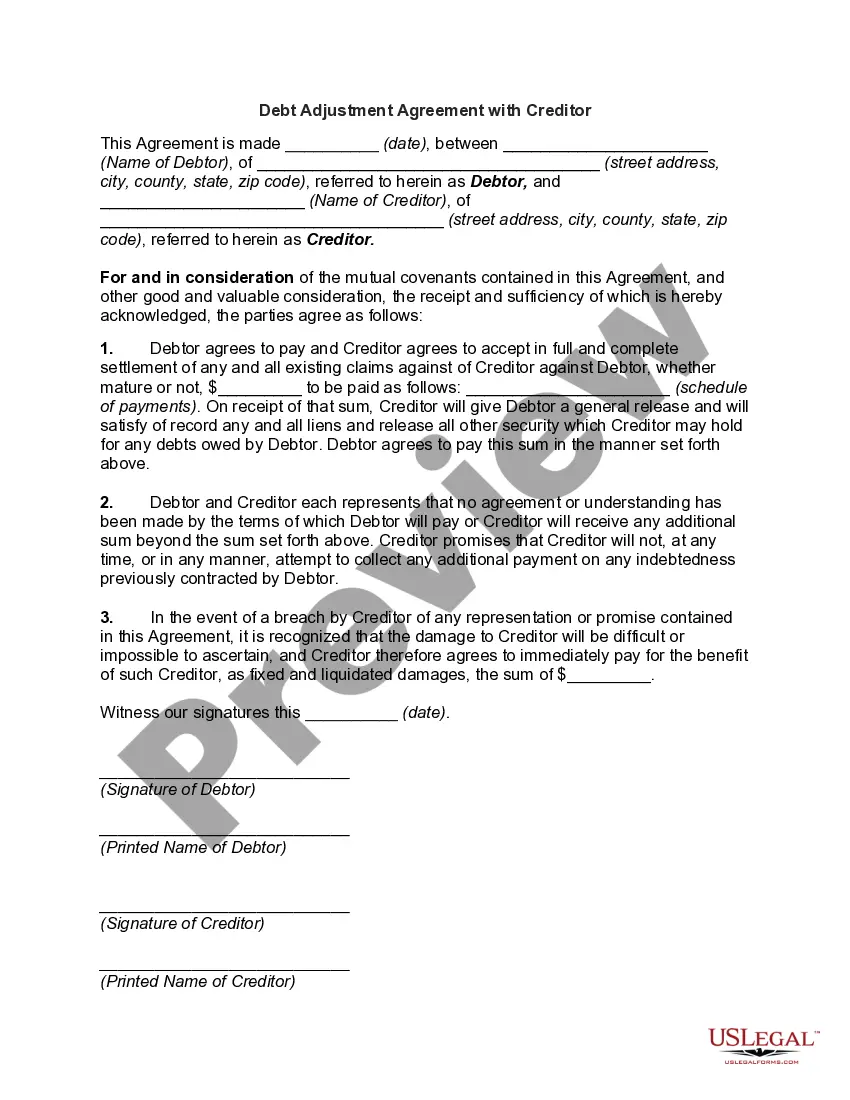

A New Jersey Debt Adjustment Agreement with Creditor is a legally binding contract entered into between a borrower and their creditor to outline a plan for repaying outstanding debts. This agreement is designed to provide relief for individuals or businesses burdened by debt, helping them to manage their financial obligations and avoid bankruptcy. One common type of New Jersey Debt Adjustment Agreement with Creditor is a Debt Management Plan (DMP). In a DMP, the borrower works with a credit counseling agency to negotiate reduced interest rates and monthly payments with their creditors. The agency then distributes the agreed-upon payments to each creditor until the debt is fully repaid. Another type of agreement is a Debt Settlement Agreement (DSA), which involves negotiating with creditors to settle the debt for a reduced amount. Typically, this involves making a lump sum payment or a series of payments to satisfy the outstanding debt. Creditors may be willing to accept a reduced amount to avoid the risk of the borrower filing for bankruptcy. A New Jersey Debt Adjustment Agreement with Creditor typically includes details such as the names and contact information of the parties involved, a description of the debts being addressed, payment terms, interest rates (if applicable), and any other specific terms or conditions agreed upon. It is essential to review and understand all provisions of the agreement before signing to ensure compliance and avoid potential penalties. The purpose of a New Jersey Debt Adjustment Agreement with Creditor is to establish a clear and manageable repayment plan, allowing the borrower to regain control of their finances and work towards becoming debt-free. By entering into such an agreement, both parties can avoid more severe financial consequences and work towards resolving the debt in a more sustainable manner. In summary, a New Jersey Debt Adjustment Agreement with Creditor is a crucial tool for individuals or businesses seeking to address and resolve their outstanding debts. By exploring options such as Debt Management Plans or Debt Settlement Agreements, borrowers can find a customized solution that suits their specific financial situation and goals. It is important to consider seeking professional advice from credit counseling agencies or debt relief services to ensure the agreement is structured properly and results in meaningful debt resolution.

New Jersey Debt Adjustment Agreement with Creditor

Description

How to fill out New Jersey Debt Adjustment Agreement With Creditor?

US Legal Forms - one of the most significant libraries of legitimate kinds in the USA - offers a variety of legitimate record layouts it is possible to acquire or print out. While using internet site, you can find a huge number of kinds for company and individual reasons, sorted by categories, claims, or key phrases.You can get the newest versions of kinds such as the New Jersey Debt Adjustment Agreement with Creditor in seconds.

If you currently have a membership, log in and acquire New Jersey Debt Adjustment Agreement with Creditor from the US Legal Forms collection. The Down load key will appear on each develop you look at. You gain access to all earlier downloaded kinds within the My Forms tab of your own profile.

If you want to use US Legal Forms for the first time, allow me to share easy recommendations to help you get started out:

- Make sure you have picked the correct develop for your area/region. Click the Review key to analyze the form`s content. See the develop outline to actually have chosen the right develop.

- In case the develop doesn`t satisfy your specifications, use the Lookup discipline near the top of the monitor to get the one which does.

- Should you be content with the form, confirm your choice by clicking on the Purchase now key. Then, choose the costs prepare you favor and supply your accreditations to register for the profile.

- Method the transaction. Make use of your credit card or PayPal profile to accomplish the transaction.

- Select the formatting and acquire the form on the system.

- Make adjustments. Fill up, modify and print out and indicator the downloaded New Jersey Debt Adjustment Agreement with Creditor.

Each web template you added to your money lacks an expiry time and is also your own property forever. So, in order to acquire or print out an additional version, just proceed to the My Forms area and click on about the develop you need.

Gain access to the New Jersey Debt Adjustment Agreement with Creditor with US Legal Forms, the most comprehensive collection of legitimate record layouts. Use a huge number of skilled and condition-certain layouts that satisfy your organization or individual requirements and specifications.