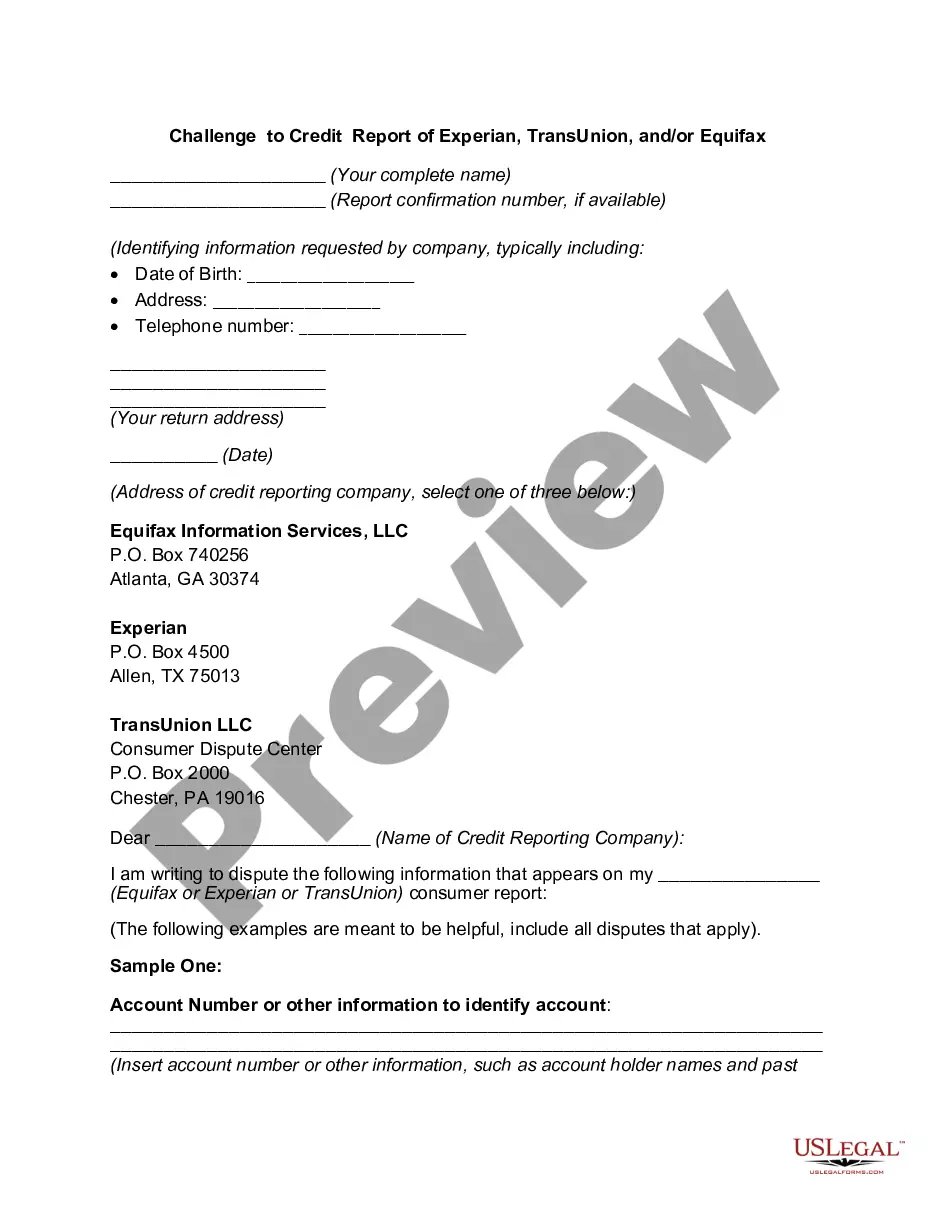

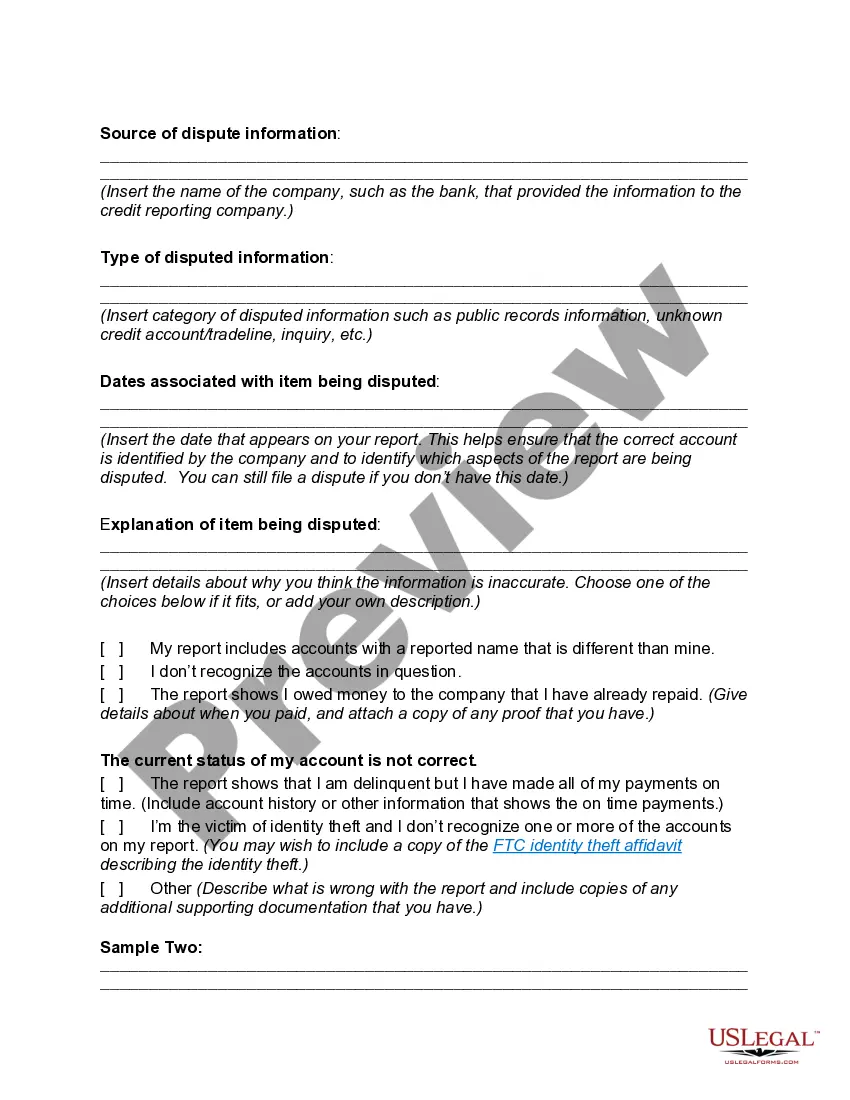

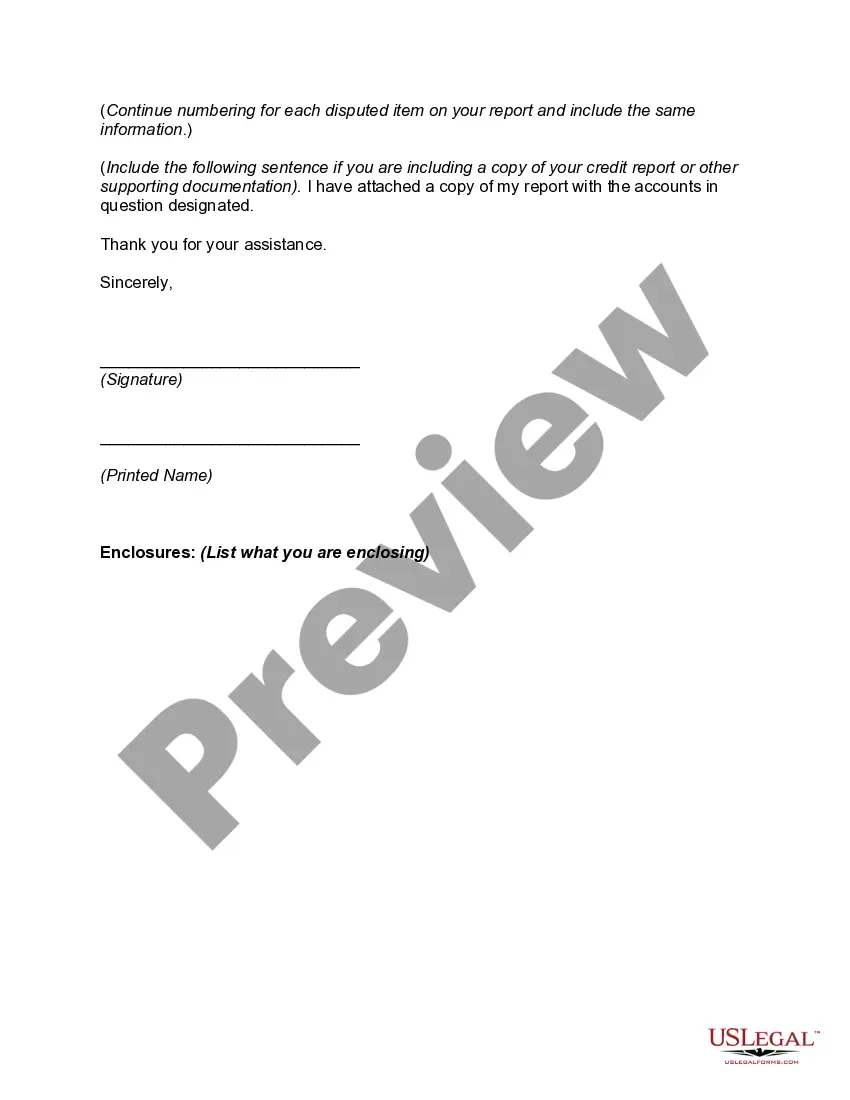

Title: A Comprehensive Guide: Understanding New Jersey's Challenge to Credit Report of Experian, TransUnion, and/or Equifax Introduction: When it comes to improving your financial health, maintaining an accurate credit report is crucial. In New Jersey, individuals have the right to challenge any errors or discrepancies found on their credit reports issued by credit reporting agencies like Experian, TransUnion, and Equifax. This detailed description will explore various types and procedures of challenging credit reports in New Jersey, utilizing relevant keywords throughout. 1. Overview of Challenging Credit Reports in New Jersey: a. Importance of credit reports in financial decision-making processes. b. Statutory rights provided by federal laws like the Fair Credit Reporting Act (FCRA) and New Jersey Fair Credit Reporting Act (NJ FCRA). c. Key players involved: Individuals, credit reporting agencies (Experian, TransUnion, Equifax), and furnishes of information (creditors, lenders, etc.). d. Objective: To ensure the accuracy and fairness of credit reports. 2. Identifying Errors and Discrepancies: a. Different types of errors to look out for: Incorrect personal information, outdated accounts, duplicate accounts, unfamiliar inquiries, mistaken late payments, and more. b. Regular monitoring and obtaining free annual credit reports. c. Establishing a solid foundation for challenging invalid information. 3. Initiating the Challenge Process: a. Reviewing credit reports: Identifying specific errors and gathering supporting documentation. b. Drafting dispute letters: Formal written communication that highlights the error(s) in detail, provides supporting evidence, and requests correction or removal. c. Electronic methods: Utilizing online dispute resolution platforms offered by credit reporting agencies. d. Timelines and deadlines: Adhering to the proper time constraints for effective dispute resolution. 4. Challenging Multiple Credit Reporting Agencies: a. How to challenge Experian, TransUnion, and Equifax simultaneously. b. Highlighting inconsistencies across multiple credit reports. c. Submitting separate dispute letters for each agency. 5. The Role of Credit Reporting Agencies: a. Investigation process: Credit reporting agencies are required to investigate the dispute within a specific timeframe. b. Collaboration with furnishes of information: Communication with creditors to validate the disputed information. c. Corrective action: Amending the credit report or removing erroneous information if deemed inaccurate or unverifiable. 6. Escalating the Dispute: a. If initial challenges are unsuccessful, escalation options are available. b. Filing a complaint with the Consumer Financial Protection Bureau (CFPB). c. Seeking legal assistance: Engaging a credit attorney to navigate complex credit dispute matters. Conclusion: Challenging credit reports is a crucial step towards maintaining an accurate financial profile. In New Jersey, individuals possess the right to challenge any inaccuracies found on their credit reports issued by credit reporting agencies. By closely monitoring credit reports, identifying errors, and following the appropriate procedures, residents of New Jersey can proactively safeguard their financial well-being.

New Jersey Challenge to Credit Report of Experian, TransUnion, and/or Equifax

Description

How to fill out New Jersey Challenge To Credit Report Of Experian, TransUnion, And/or Equifax?

Are you within a place in which you require paperwork for both company or person functions almost every working day? There are a lot of authorized file web templates available online, but finding versions you can depend on isn`t easy. US Legal Forms provides a large number of develop web templates, just like the New Jersey Challenge to Credit Report of Experian, TransUnion, and/or Equifax, which are created to fulfill federal and state specifications.

When you are presently acquainted with US Legal Forms website and also have an account, merely log in. Following that, you can down load the New Jersey Challenge to Credit Report of Experian, TransUnion, and/or Equifax web template.

Unless you offer an account and need to begin to use US Legal Forms, abide by these steps:

- Get the develop you want and ensure it is for your appropriate city/area.

- Use the Review option to review the form.

- Look at the information to ensure that you have chosen the right develop.

- In case the develop isn`t what you are trying to find, make use of the Research discipline to get the develop that meets your requirements and specifications.

- If you get the appropriate develop, click Acquire now.

- Select the pricing prepare you would like, fill in the specified details to create your bank account, and pay money for your order with your PayPal or charge card.

- Pick a hassle-free data file file format and down load your copy.

Find all the file web templates you might have purchased in the My Forms menus. You can aquire a further copy of New Jersey Challenge to Credit Report of Experian, TransUnion, and/or Equifax any time, if necessary. Just click the required develop to down load or produce the file web template.

Use US Legal Forms, the most comprehensive variety of authorized kinds, in order to save time as well as prevent faults. The assistance provides appropriately produced authorized file web templates which you can use for a range of functions. Create an account on US Legal Forms and commence making your daily life easier.