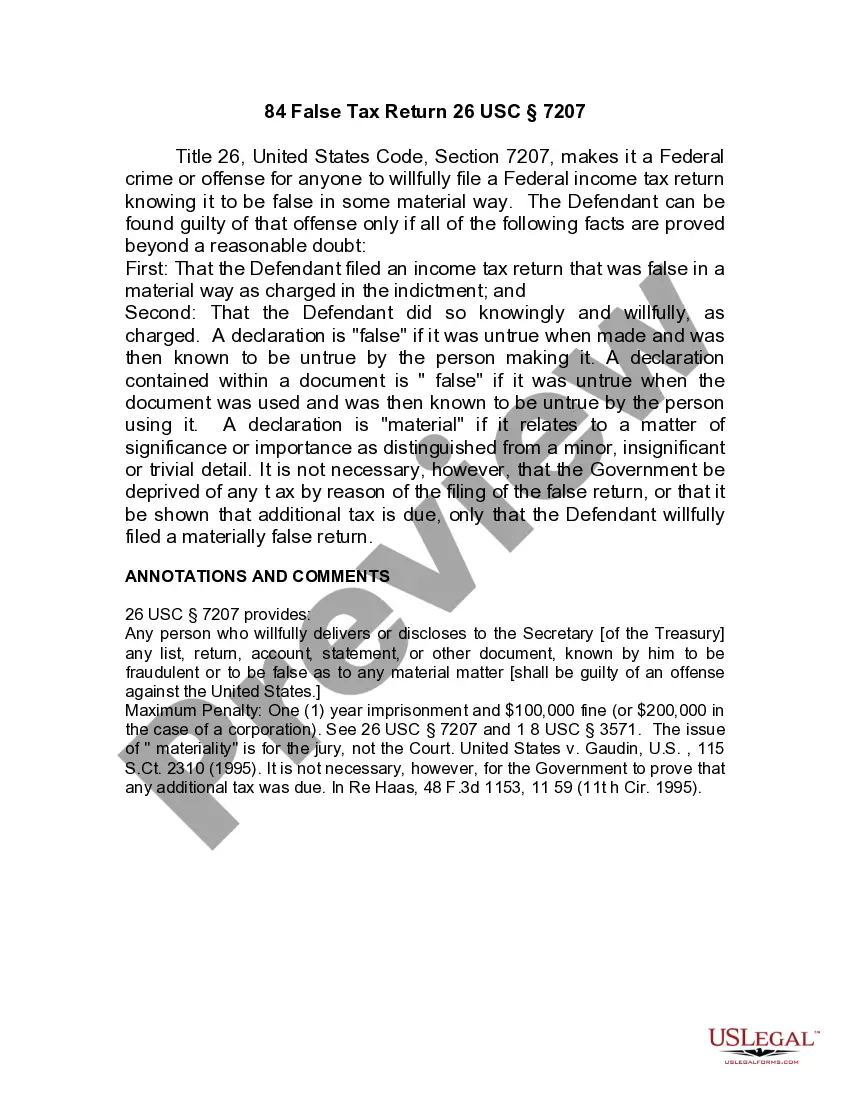

New Jersey Jury Instruction - 10.10.6 Section 6672 Penalty

Description

How to fill out Jury Instruction - 10.10.6 Section 6672 Penalty?

You can devote time on the Internet attempting to find the legitimate record design that fits the state and federal specifications you want. US Legal Forms provides a huge number of legitimate forms which can be examined by specialists. You can actually download or print out the New Jersey Jury Instruction - 10.10.6 Section 6672 Penalty from our assistance.

If you already have a US Legal Forms profile, it is possible to log in and click the Obtain button. Next, it is possible to full, change, print out, or sign the New Jersey Jury Instruction - 10.10.6 Section 6672 Penalty. Each and every legitimate record design you get is your own property eternally. To obtain yet another duplicate for any bought develop, go to the My Forms tab and click the corresponding button.

If you use the US Legal Forms web site initially, adhere to the straightforward directions under:

- First, make sure that you have selected the best record design for your state/area of your choosing. Read the develop description to ensure you have selected the proper develop. If accessible, utilize the Review button to check throughout the record design as well.

- In order to find yet another variation in the develop, utilize the Search area to get the design that fits your needs and specifications.

- After you have discovered the design you want, click on Buy now to proceed.

- Choose the pricing prepare you want, type your credentials, and register for a free account on US Legal Forms.

- Comprehensive the transaction. You can utilize your charge card or PayPal profile to cover the legitimate develop.

- Choose the file format in the record and download it in your product.

- Make adjustments in your record if required. You can full, change and sign and print out New Jersey Jury Instruction - 10.10.6 Section 6672 Penalty.

Obtain and print out a huge number of record templates utilizing the US Legal Forms Internet site, which offers the largest assortment of legitimate forms. Use specialist and express-distinct templates to deal with your small business or person needs.