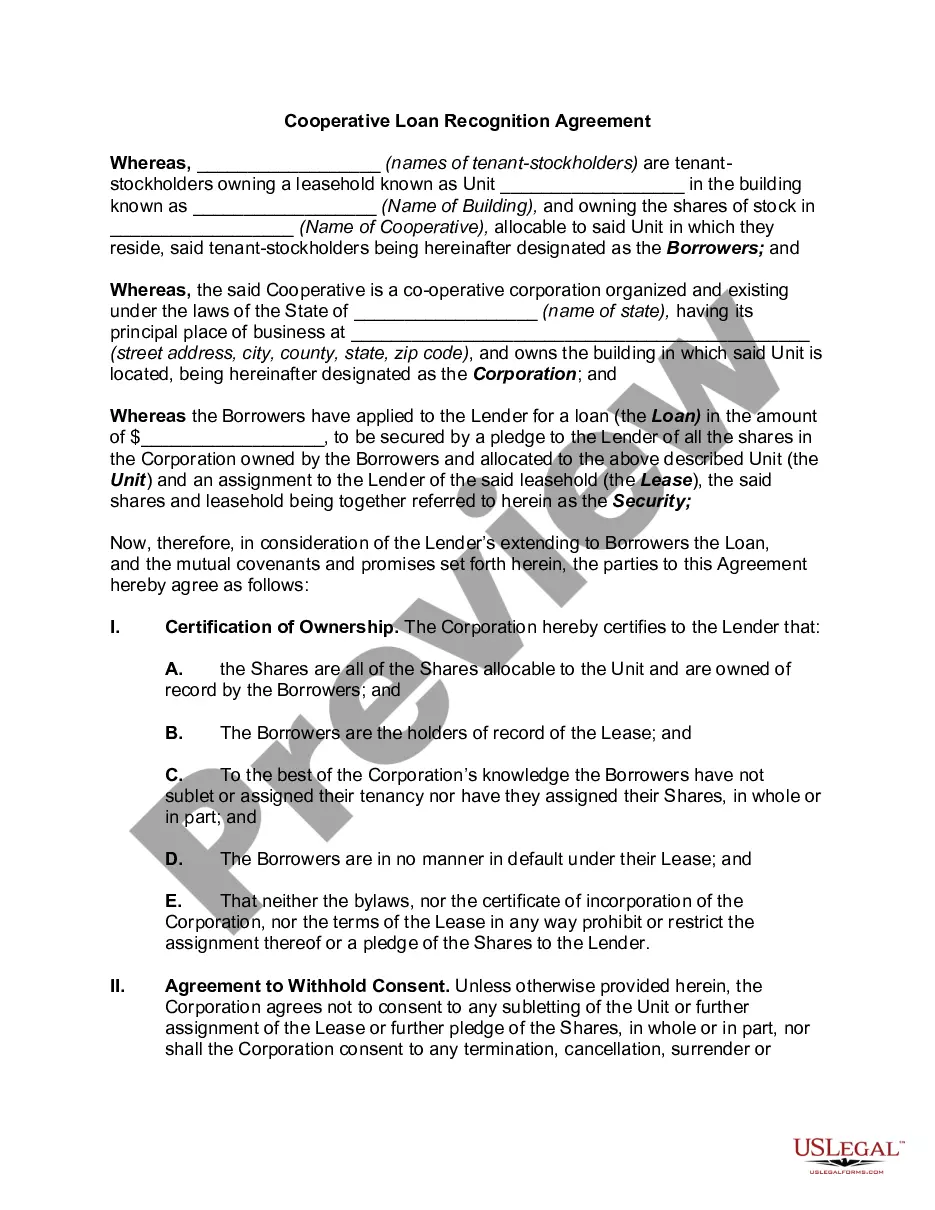

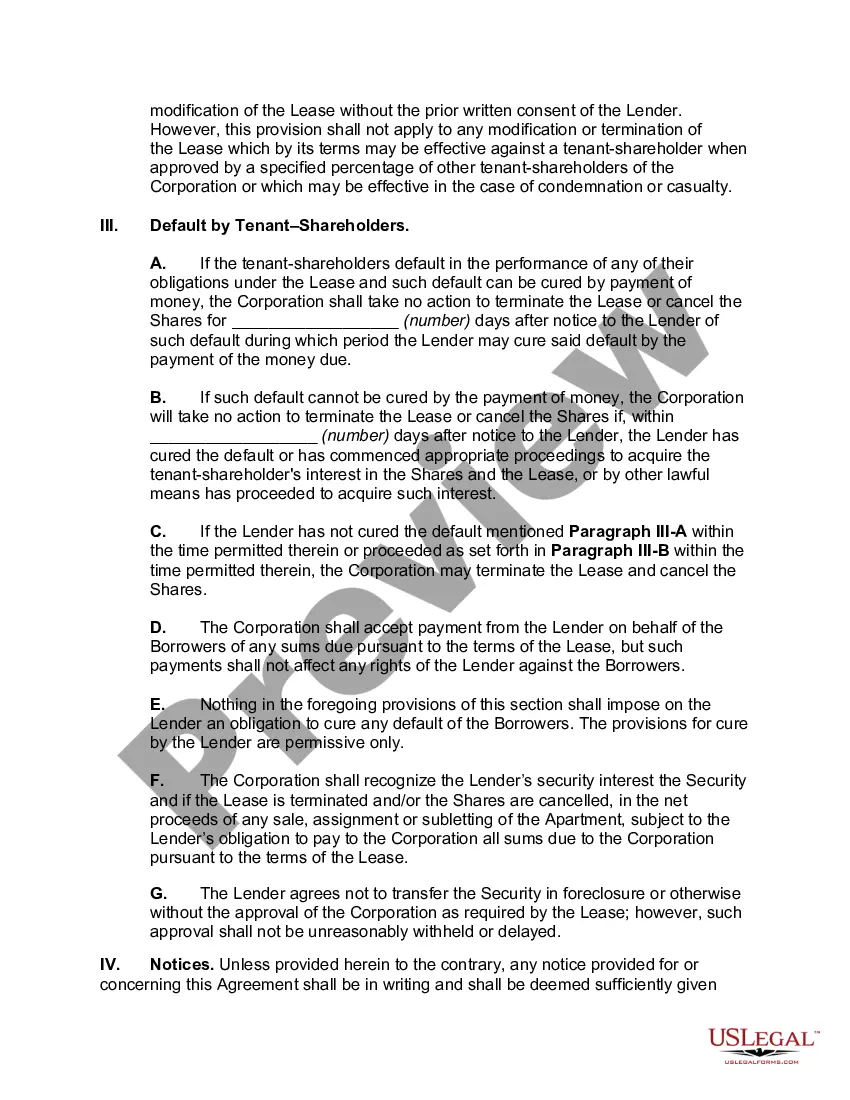

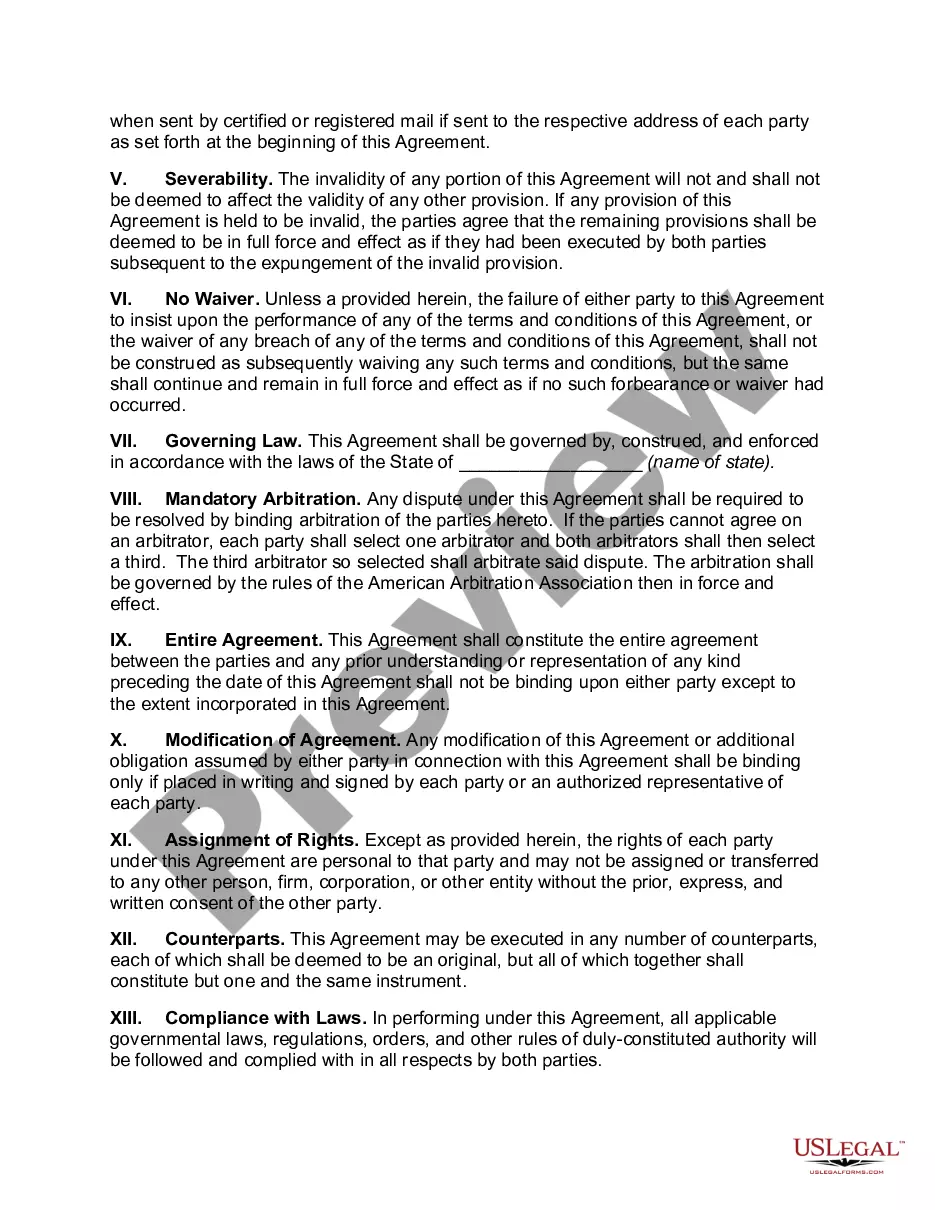

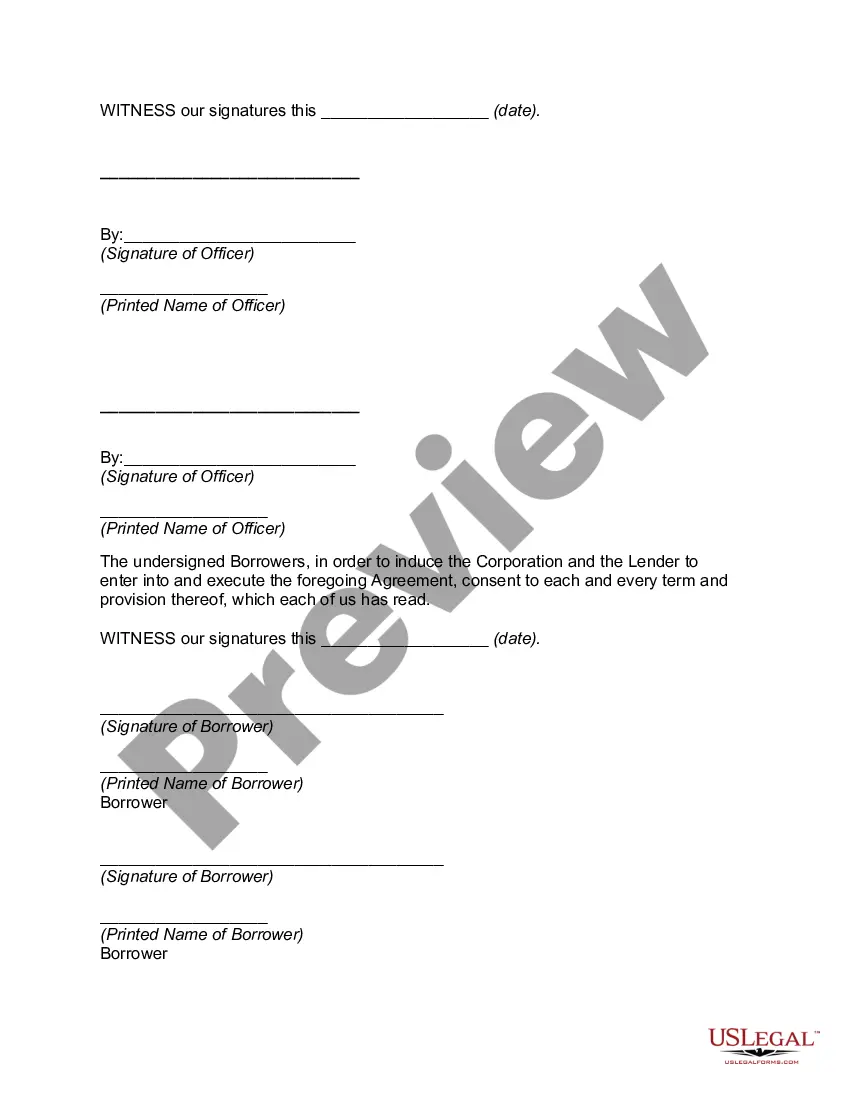

A New Jersey Cooperative Loan Recognition Agreement refers to a legal document that outlines the terms and conditions of a loan provided to a cooperative in New Jersey. Co-ops, also known as housing cooperatives, are community-owned residential properties where residents collectively own and manage the building or complex. The Cooperative Loan Recognition Agreement ensures that the loan provided to the cooperative is recognized and secured properly. It typically includes details such as the loan amount, interest rate, repayment schedule, and any collateral or guarantees involved. This agreement is meant to protect the lender's rights and ensure the repayment of the loan. Different types of New Jersey Cooperative Loan Recognition Agreements can exist based on various factors such as the purpose of the loan or the specific terms agreed upon by the cooperative and the lender. Some common types of Cooperative Loan Recognition Agreements in New Jersey include: 1. Construction Loan Recognition Agreement: This type of agreement is used when a cooperative is undergoing construction or renovation. The loan is provided to cover the expenses associated with building or improving the cooperative property. 2. Refinancing Loan Recognition Agreement: When a cooperative decides to refinance its existing loan, a refinancing loan recognition agreement is put in place. This agreement outlines the terms of the new loan that will be used to pay off the existing loan, typically to secure better interest rates or repayment terms. 3. Acquisition Loan Recognition Agreement: In instances where a cooperative is purchasing a new property or expanding its existing property, an acquisition loan recognition agreement is signed. This agreement defines the terms of the loan used for the acquisition or expansion. 4. Working Capital Loan Recognition Agreement: Sometimes, a cooperative may require additional funds for its day-to-day operations or to cover unexpected expenses. In such cases, a working capital loan recognition agreement is entered into, outlining the terms and conditions of the loan used to meet the cooperative's short-term financial needs. Regardless of the specific type, a New Jersey Cooperative Loan Recognition Agreement plays a vital role in establishing a legally binding agreement between the cooperative and the lender. It ensures transparency, protects the rights of both parties involved, and provides a framework for loan repayment.

New Jersey Cooperative Loan Recognition Agreement

Description

How to fill out New Jersey Cooperative Loan Recognition Agreement?

You can commit time on the web trying to find the lawful papers format which fits the state and federal demands you need. US Legal Forms offers 1000s of lawful types which are examined by specialists. You can actually acquire or print out the New Jersey Cooperative Loan Recognition Agreement from my support.

If you have a US Legal Forms accounts, you are able to log in and then click the Download switch. Afterward, you are able to comprehensive, modify, print out, or sign the New Jersey Cooperative Loan Recognition Agreement. Each and every lawful papers format you acquire is the one you have for a long time. To obtain one more copy associated with a obtained develop, visit the My Forms tab and then click the related switch.

If you work with the US Legal Forms internet site for the first time, adhere to the simple recommendations beneath:

- Initially, make sure that you have chosen the proper papers format for the state/city of your choice. Look at the develop information to make sure you have picked out the appropriate develop. If available, make use of the Preview switch to look throughout the papers format at the same time.

- If you would like locate one more version of the develop, make use of the Search industry to get the format that suits you and demands.

- After you have found the format you need, click Acquire now to continue.

- Pick the pricing plan you need, type your accreditations, and register for an account on US Legal Forms.

- Comprehensive the purchase. You may use your charge card or PayPal accounts to fund the lawful develop.

- Pick the formatting of the papers and acquire it to your device.

- Make adjustments to your papers if possible. You can comprehensive, modify and sign and print out New Jersey Cooperative Loan Recognition Agreement.

Download and print out 1000s of papers layouts making use of the US Legal Forms web site, that provides the most important collection of lawful types. Use professional and express-certain layouts to tackle your small business or individual requirements.

Form popularity

FAQ

The stock, shares, membership certificates, or other contractual agreement evidencing ownership. The original Recognition Agreement, and, if applicable, the original assignment of the Recognition Agreement to the lender.

A recognition agreement is a legal document that allows parties to recognize each other's interests in an agreement.

Mutual recognition agreements lay down the conditions under which one Party (non-member country) will accept conformity assessment results (e.g. testing or certification) performed by the other's Party (the EU) designated conformity assessment bodies (CABs) to show compliance with the first Party's (non-member country) ...

Recognition Agreement means, with respect to a Cooperative Mortgage Loan, an agreement executed by a Cooperative Corporation which, among other things, acknowledges the lien of the Mortgage on the Mortgaged Property in question.

A recognition agreement names the union or unions who have rights to represent and negotiate on behalf of employees in that workplace. It will make clear whether a particular union has sole negotiating rights for a bargaining group, or whether the employer recognises two or more unions jointly.

A recognition agreement names the union or unions who have rights to represent and negotiate on behalf of employees in that workplace.

More specifically, a recognition agreement is a contract between a subtenant and a prime landlord under which the prime landlord agrees to recognize the subtenant and the sublease if the tenant/sublandlord defaults under the prime lease and the prime landlord terminates the prime lease.

Assignment of Recognition Agreement . With respect to a Cooperative Loan, an assignment of the Recognition Agreement sufficient under the laws of the jurisdiction wherein the related Cooperative Unit is located to reflect the assignment of such Recognition Agreement.