The New Jersey Waiver of Qualified Joint and Survivor Annuity (JSA) is a legal provision that allows individuals to waive their right to a joint and survivor annuity in retirement plans. Keywords: New Jersey, waiver, qualified joint and survivor annuity, JSA. JSA: The first type of New Jersey Waiver of Qualified Joint and Survivor Annuity is known as JSA. This waiver enables individuals to opt-out of the qualified joint and survivor annuity provision, which typically provides a continued income stream to the surviving spouse in the event of the retiree's death. By choosing JSA, the retiree can receive a higher monthly payment during their lifetime but eliminates the guarantee of income for their spouse after their passing. BSA: The second type is BSA, which is similar to JSA but provides a smaller monthly payment to the retiree during their lifetime in exchange for a reduced survivor benefit for their spouse. This option offers a more balanced approach, allowing a certain level of income security for both the retiree and their surviving spouse. Mandatory JSA: In contrast to the above waivers, the state of New Jersey also has a mandatory Qualified Joint and Survivor Annuity provision. This means that unless a retiree chooses one of the available waiver options, their retirement plan will automatically include a joint and survivor annuity, providing a reduced monthly payment to the retiree but ensuring continued income for the surviving spouse. Considerations: When deciding between the various types of New Jersey Waiver of Qualified Joint and Survivor Annuity, individuals should carefully assess their financial situation, anticipated retirement needs, and the financial well-being of their spouse. Consulting with a financial advisor or retirement specialist can help determine the most suitable option. Overall, the New Jersey Waiver of Qualified Joint and Survivor Annuity (JSA) offers retirees the flexibility to choose between different annuity options based on their unique circumstances, ensuring financial security during retirement while considering the support for their spouse after their passing.

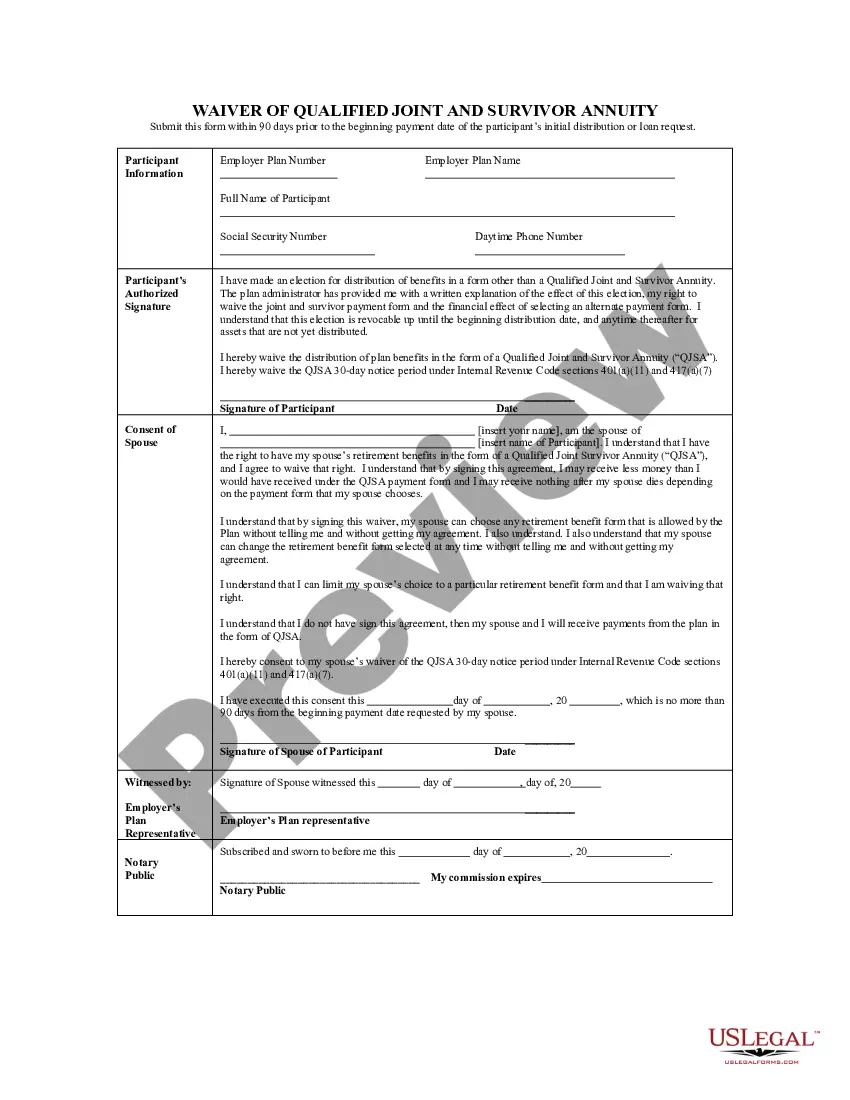

New Jersey Waiver of Qualified Joint and Survivor Annuity - QJSA

Description

How to fill out New Jersey Waiver Of Qualified Joint And Survivor Annuity - QJSA?

Have you been inside a situation that you require paperwork for both company or personal uses virtually every time? There are a variety of legal record templates available online, but discovering kinds you can rely is not simple. US Legal Forms provides a large number of kind templates, such as the New Jersey Waiver of Qualified Joint and Survivor Annuity - QJSA, that happen to be composed to satisfy state and federal demands.

When you are currently informed about US Legal Forms site and possess a merchant account, just log in. Afterward, you can down load the New Jersey Waiver of Qualified Joint and Survivor Annuity - QJSA template.

If you do not provide an accounts and want to begin using US Legal Forms, follow these steps:

- Discover the kind you will need and ensure it is for your right area/state.

- Make use of the Review button to analyze the shape.

- Read the outline to actually have selected the appropriate kind.

- In case the kind is not what you are seeking, take advantage of the Look for area to discover the kind that meets your needs and demands.

- When you get the right kind, simply click Purchase now.

- Choose the rates strategy you want, submit the necessary information and facts to generate your account, and pay for the transaction using your PayPal or credit card.

- Decide on a practical data file structure and down load your duplicate.

Locate all of the record templates you possess purchased in the My Forms menus. You can get a further duplicate of New Jersey Waiver of Qualified Joint and Survivor Annuity - QJSA any time, if needed. Just select the essential kind to down load or produce the record template.

Use US Legal Forms, probably the most comprehensive variety of legal forms, to conserve time and prevent blunders. The support provides expertly produced legal record templates which you can use for a selection of uses. Generate a merchant account on US Legal Forms and commence producing your lifestyle a little easier.

Form popularity

FAQ

When the participant dies, the spouse will receive lifetime payments in the same or reduced amount. The participant may waive the Qualified Joint and Survivor Annuity with spousal consent and elect to receive another form of payment.

Qualified Joint and Survivor AnnuityIf your spouse consents to change the way the Plan's retirement benefits are paid, your spouse gives up his or her right to the QJSA payments. This is referred to as a waiver of the QJSA payment form.

It makes sense to waive a joint pension if: (1) the spouse has a good pension of his or her own; (2) the spouse is ill unto death and not likely to outlive the worker; (3) the couple has so much money that the spouse doesn't need the pension to live on.

This special payment form is often called a qualified joint and survivor annuity or QJSA payment form. This benefit is paid to the participant each year and, on the participant's death, a survivor annuity is paid to the surviving spouse.

A joint and survivor annuity is an insurance product designed for couples that continues to make regular payments as long as one spouse lives. A joint and survivor annuity has the advantage of providing income if one or both people live longer than expected. This is not a good choice for a younger couple.

Qualified Joint and Survivor Annuity (QJSA) includes a level monthly payment for your lifetime and a survivor benefit for your spouse after your death equal to the percentage designated of that monthly payment.

This benefit provides payments to the participant's spouse for his or her lifetime equal to a percentage (as specified in the Pension Plan) not less than one-half of the annuity that would have been payable during their joint lives. The participant may waive the Qualified Preretirement Survivor Annuity.

life annuity provides the largest monthly payment but pays only during your lifetime. It's a poor choice if your spouse will need income from your pension to pay routine expenses. A jointandsurvivor annuity pays you during your lifetime and then continues to pay your spouse or other named beneficiary.

A QJSA is when retirement benefits are paid as a life annuity (a series of payments, usually monthly, for life) to the participant and a survivor annuity over the life of the participant's surviving spouse (or a former spouse, child or dependent who must be treated as a surviving spouse under a QDRO) following the

QJSA rules apply to money-purchase pension plans, defined benefit plans, and target benefits. They can also apply to profit-sharing and 401(k) and 403(b) plans, but only if so elected under the plan.