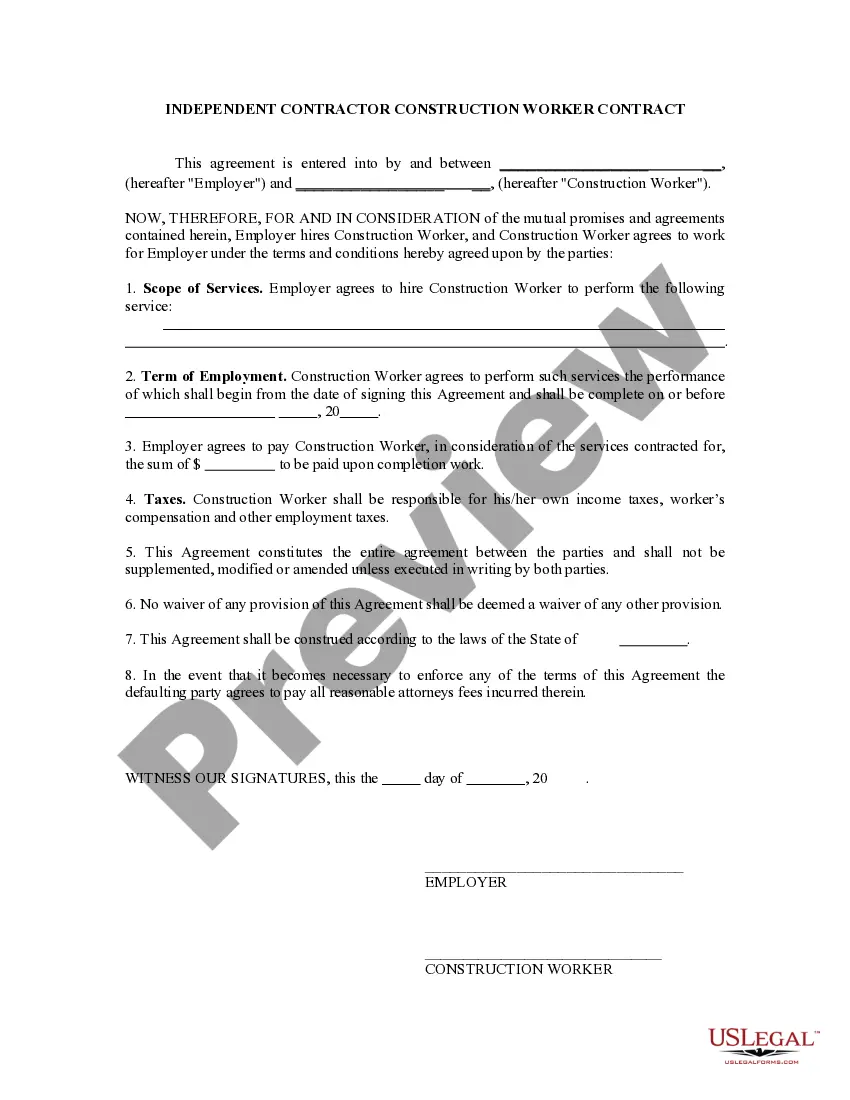

New Jersey Determining Self-Employed Contractor Status

Description

How to fill out Determining Self-Employed Contractor Status?

You might spend hours online looking for the legal document template that complies with the state and federal requirements necessary for you. US Legal Forms provides thousands of legal forms that have been reviewed by professionals.

You can conveniently download or print the New Jersey Determining Self-Employed Contractor Status from my services.

If you possess a US Legal Forms account, you can Log In and then click the Download button. After that, you can complete, modify, print, or sign the New Jersey Determining Self-Employed Contractor Status. Each legal document template you acquire is yours for a long duration.

Complete the transaction. You may use your Visa, Mastercard, or PayPal account to pay for the legal form. Choose the format of the document and download it to your device. Make changes to your document if needed. You may complete, modify, sign, and print the New Jersey Determining Self-Employed Contractor Status. Download and print thousands of document templates using the US Legal Forms website, which offers the largest collection of legal forms. Utilize professional and state-specific templates to meet your business or personal needs.

- To obtain another copy of the purchased form, go to the My documents tab and click the corresponding button.

- If you are visiting the US Legal Forms site for the first time, follow the simple instructions below.

- First, ensure that you have selected the correct document template for the county/city of your choice. Review the form details to confirm you have chosen the right form.

- If available, use the Review button to browse through the document template as well.

- If you wish to get another version of the form, utilize the Search section to find the template that fits your needs and specifications.

- Once you have found the template you require, click on Purchase now to proceed.

- Select the pricing plan you want, enter your credentials, and register for an account on US Legal Forms.

Form popularity

FAQ

Becoming an independent contractor is one of the many ways to be classified as self-employed. By definition, an independent contractor provides work or services on a contractual basis, whereas, self-employment is simply the act of earning money without operating within an employee-employer relationship.

The individual is customarily engaged in an independently established trade, occupation, profession or business.

Self contracting means you are the one overseeing the project. You are in charge of everything including budgeting, getting permits, hiring the workers, getting inspections, and keeping everything organized and clean.

The IRS says that someone is self-employed if they meet one of these conditions: Someone who carries on a trade or business as a sole proprietor or independent contractor, A member of a partnership that carries on a trade or business, or. Someone who is otherwise in business for themselves, including part-time business

Simply put, being an independent contractor is one way to be self-employed. Being self-employed means that you earn money but don't work as an employee for someone else.

How to demonstrate that you are an independent worker on your resumeMention that time when you had to work on a project on your own.Talk about projects that required extra accountability.Describe times when you had to manage several projects all at once.More items...

The basic test for determining whether a worker is an independent contractor or an employee is whether the principal has the right to control the manner and means by which the work is performed.

Four ways to verify your income as an independent contractorIncome-verification letter. The most reliable method for proving earnings for independent contractors is a letter from a current or former employer describing your working arrangement.Contracts and agreements.Invoices.Bank statements and Pay stubs.

The general rule is that an individual is an independent contractor if the payer has the right to control or direct only the result of the work and not what will be done and how it will be done. If you are an independent contractor, then you are self-employed.

The general rule is that an individual is an independent contractor if the payer has the right to control or direct only the result of the work and not what will be done and how it will be done. If you are an independent contractor, then you are self-employed.