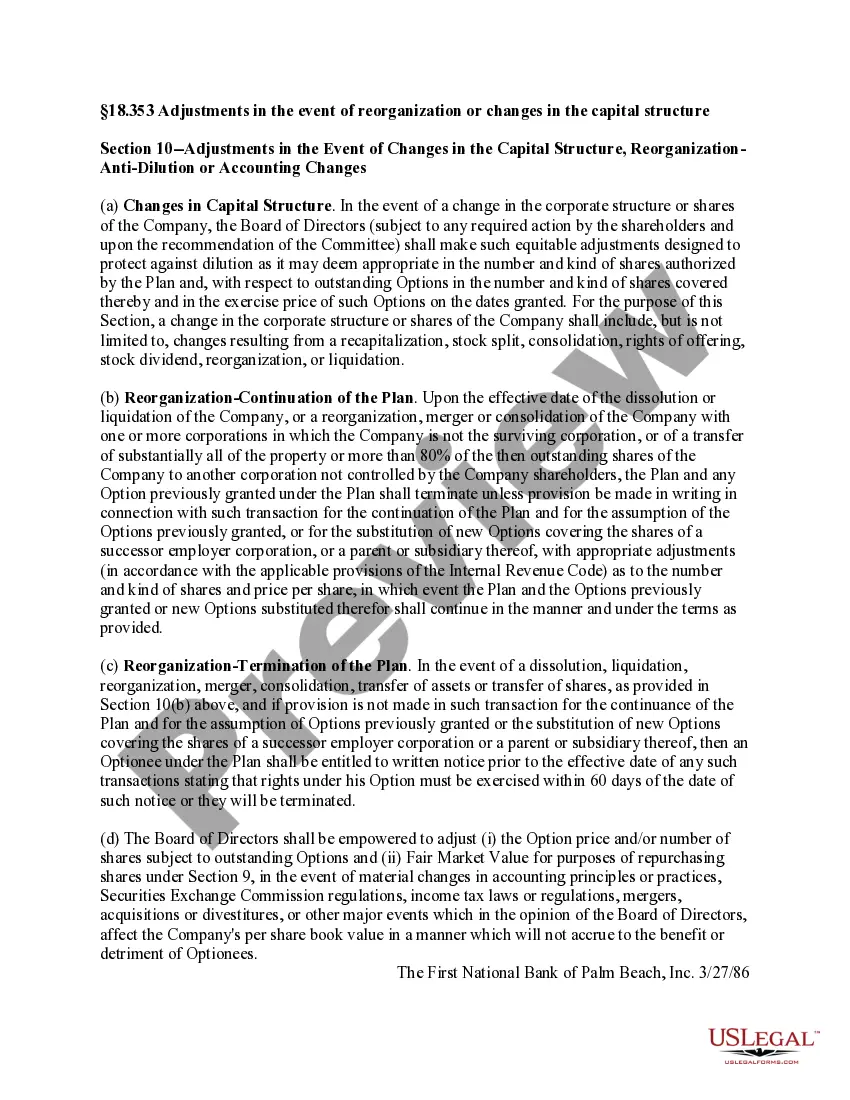

New Jersey Adjustments in the Event of Reorganization or Changes in the Capital Structure When a company undergoes reorganization or experiences changes in its capital structure, there are various adjustments that may need to be made in accordance with New Jersey's laws and regulations. These adjustments aim to ensure fairness and transparency during such transformative business activities. Let's explore these adjustments and the different types that may arise. 1. Debt Restructuring Adjustment: One common type of adjustment in New Jersey entails debt restructuring. When a company reorganizes itself or undergoes changes in its financial structure, it may need to modify its existing debt agreements. This adjustment can involve negotiating new terms, extending repayment schedules, reducing interest rates, or even seeking debt forgiveness. Such adjustments are made to facilitate the company's financial stability and revive its chances of success. 2. Stock Split or Reverse Stock Split Adjustment: Another adjustment associated with changes in the capital structure involves the manipulation of a company's stock or shares. When undergoing reorganization, a company may choose to split its existing stock into multiple shares or combine shares to reduce their number. This adjustment, also known as a stock split or reverse stock split, aims to adjust the company's stock price and improve liquidity or meet regulatory requirements. 3. Conversion of Securities Adjustment: In certain reorganization scenarios, a company may need to convert its existing securities, such as convertible debt or preferred stock, into common stock or other equity instruments. This conversion adjustment allows the restructured company to streamline its capital structure and align the rights and preferences of different stakeholders appropriately. 4. Asset Valuation Adjustment: During reorganization, it may become necessary to reevaluate the value of assets held by the company. This adjustment ensures that the company's financial statements reflect the fair value of its assets in the changed circumstances. Accurate asset valuation aids in determining the company's net worth and establishing an equitable framework for distributing value to various stakeholders. 5. Intangible Asset Impairment Adjustment: If a company's reorganization causes a significant change in its operations, it may result in the impairment of intangible assets. An adjustment is made to recognize this impairment by reducing the carrying value of the assets on the company's balance sheet. This adjustment helps maintain the accuracy and reliability of the company's financial statements. 6. Tax Liability Adjustment: Reorganization or changes in the capital structure can have implications for a company's tax liabilities. Adjustments are made to account for any potential changes in tax rates, tax credits, or deferred tax assets or liabilities arising from the restructuring. These adjustments ensure compliance with the relevant tax laws and prevent any adverse tax consequences. In conclusion, when organizations in New Jersey undergo reorganization or experience changes in their capital structure, various adjustments are made to accommodate these transformations. Debt restructuring, stock splits or reverse stock splits, conversion of securities, asset valuation, intangible asset impairment, and tax liability adjustments are some key types of adjustments that may come into play. Adhering to these adjustments ensures that businesses navigate through reorganizations smoothly while maintaining financial integrity and compliance with New Jersey's regulatory framework.

New Jersey Adjustments in the event of reorganization or changes in the capital structure

Description

How to fill out New Jersey Adjustments In The Event Of Reorganization Or Changes In The Capital Structure?

You may commit hrs online trying to find the legitimate record web template which fits the state and federal specifications you need. US Legal Forms offers 1000s of legitimate types which can be reviewed by specialists. You can actually download or print out the New Jersey Adjustments in the event of reorganization or changes in the capital structure from the support.

If you already have a US Legal Forms bank account, you can log in and then click the Download option. Following that, you can comprehensive, edit, print out, or sign the New Jersey Adjustments in the event of reorganization or changes in the capital structure. Every legitimate record web template you buy is your own property for a long time. To acquire one more backup of any purchased kind, visit the My Forms tab and then click the related option.

Should you use the US Legal Forms site for the first time, follow the simple recommendations beneath:

- Initially, be sure that you have chosen the best record web template for your county/area of your choosing. See the kind explanation to ensure you have picked out the proper kind. If available, take advantage of the Review option to look throughout the record web template as well.

- If you would like discover one more version of the kind, take advantage of the Search field to find the web template that meets your requirements and specifications.

- When you have discovered the web template you would like, just click Get now to move forward.

- Select the costs program you would like, enter your credentials, and register for a free account on US Legal Forms.

- Full the purchase. You can utilize your bank card or PayPal bank account to cover the legitimate kind.

- Select the structure of the record and download it to the product.

- Make adjustments to the record if required. You may comprehensive, edit and sign and print out New Jersey Adjustments in the event of reorganization or changes in the capital structure.

Download and print out 1000s of record layouts while using US Legal Forms site, which provides the largest collection of legitimate types. Use specialist and status-certain layouts to deal with your business or person demands.

Form popularity

FAQ

The section 163(j) limitation is applied at the partnership level. As provided in Q/A 1, the amount of deductible business interest expense in a taxable year cannot exceed the sum of the partnership's business interest income, 30% of the partnership's ATI, and the partnership's floor plan financing interest expense.

If you have losses in certain business-related categories of income, you may be able to use those losses to calculate an adjustment to your taxable income (Alternative Business Calculation Adjustment). In addition, you can carry forward unused losses in those categories for 20 years to calculate future adjustments.

174, research and experimental expenditures may be treated as expenses and deducted currently or, at the election of the taxpayer, may be amortized over a period of not less than 60 months, beginning with the month in which the taxpayer first realizes benefits from the expenditures.

Investment interest expense incurred by a partner to acquire a partnership interest can be deducted from distributive share of partnership income. New Jersey residents can deduct the full amount of qualified unreimbursed business expenses from their distributive share of partnership income.

§163(j). A combined return for New Jersey Corporation Business Tax purposes is treated as one return and taxpayers should make adjustments applying the I.R.C. §163(j) limitation as though they had been included on a single federal consolidated return.

Welcome to the New Jersey Opportunity Zones Reinvested capital gains are deferred from taxation until exit from a Qualified Opportunity Fund or December 31, 2026, whichever comes first.

As for conformity to the Internal Revenue Code, approximately 35 states currently adopt section 163(j) for purposes of their corporate income taxes. That conformity, however, is far from uniform.

Although losses cannot be deducted on New Jersey tax returns, they may be deductible for federal tax purposes.