New Jersey Stock Option Grants and Exercises and Fiscal Year-End Values

Description

How to fill out Stock Option Grants And Exercises And Fiscal Year-End Values?

If you wish to comprehensive, obtain, or produce legitimate papers web templates, use US Legal Forms, the most important selection of legitimate types, that can be found on-line. Use the site`s basic and hassle-free lookup to get the documents you want. Various web templates for business and specific reasons are sorted by categories and claims, or keywords and phrases. Use US Legal Forms to get the New Jersey Stock Option Grants and Exercises and Fiscal Year-End Values in a number of click throughs.

Should you be currently a US Legal Forms client, log in to your accounts and click the Obtain option to have the New Jersey Stock Option Grants and Exercises and Fiscal Year-End Values. You can also entry types you formerly acquired within the My Forms tab of your own accounts.

Should you use US Legal Forms the very first time, refer to the instructions beneath:

- Step 1. Be sure you have chosen the form for the correct area/country.

- Step 2. Use the Preview method to look over the form`s articles. Don`t forget to see the information.

- Step 3. Should you be unhappy with the develop, use the Search area on top of the display screen to get other models from the legitimate develop format.

- Step 4. Once you have identified the form you want, click on the Purchase now option. Select the pricing program you favor and include your accreditations to sign up to have an accounts.

- Step 5. Method the purchase. You can utilize your charge card or PayPal accounts to accomplish the purchase.

- Step 6. Find the file format from the legitimate develop and obtain it in your gadget.

- Step 7. Comprehensive, change and produce or indication the New Jersey Stock Option Grants and Exercises and Fiscal Year-End Values.

Every legitimate papers format you buy is your own forever. You might have acces to every single develop you acquired with your acccount. Click on the My Forms area and decide on a develop to produce or obtain once again.

Contend and obtain, and produce the New Jersey Stock Option Grants and Exercises and Fiscal Year-End Values with US Legal Forms. There are millions of expert and express-distinct types you can use to your business or specific needs.

Form popularity

FAQ

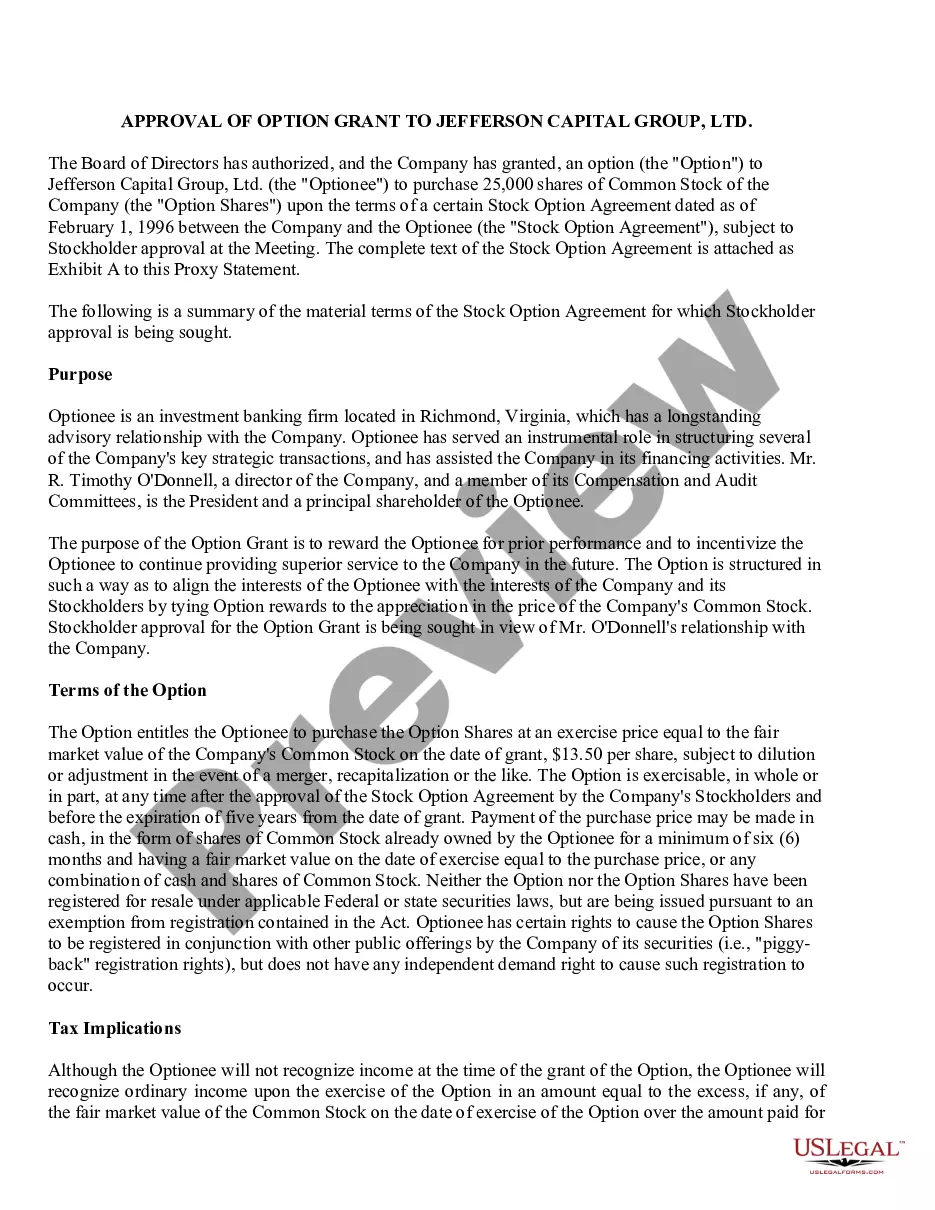

Both call and put options have an exercise price. Investors also refer to the exercise price as the strike price. The difference between the exercise price and the underlying security's price determines if an option is ?in the money? or ?out of the money."

You can calculate the aggregate exercise price by taking the strike price of the option and multiplying it by its contract size. In the case of a bond option, the exercise price is multiplied by the face value of the underlying bond.

You have taxable income or deductible loss when you sell the stock you bought by exercising the option. You generally treat this amount as a capital gain or loss. However, if you don't meet special holding period requirements, you'll have to treat income from the sale as ordinary income.

Exercising a stock option means purchasing the issuer's common stock at the price set by the option (grant price), regardless of the stock's price at the time you exercise the option.

A strike price, also known as a grant price or exercise price, is the fixed cost that you'll pay per share in order to exercise your stock options so you can own them.

Stock options are taxable as compensation on the date they are exercised or when any substantial restrictions lapse. The difference between the fair market value of the stock on the date the option...

Every stock option has an exercise price, also called the strike price, which is the price at which a share can be bought. In the US, the exercise price is typically set at the fair market value of the underlying stock as of the date the option is granted, in order to comply with certain requirements under US tax law.

Exercise Price ? Also known as the strike price, the grant price is the price at which you can buy the shares of stock. Regardless of the future value of that particular stock, the option holder will have the right to buy the shares at the grant price rather than the current, actual price.