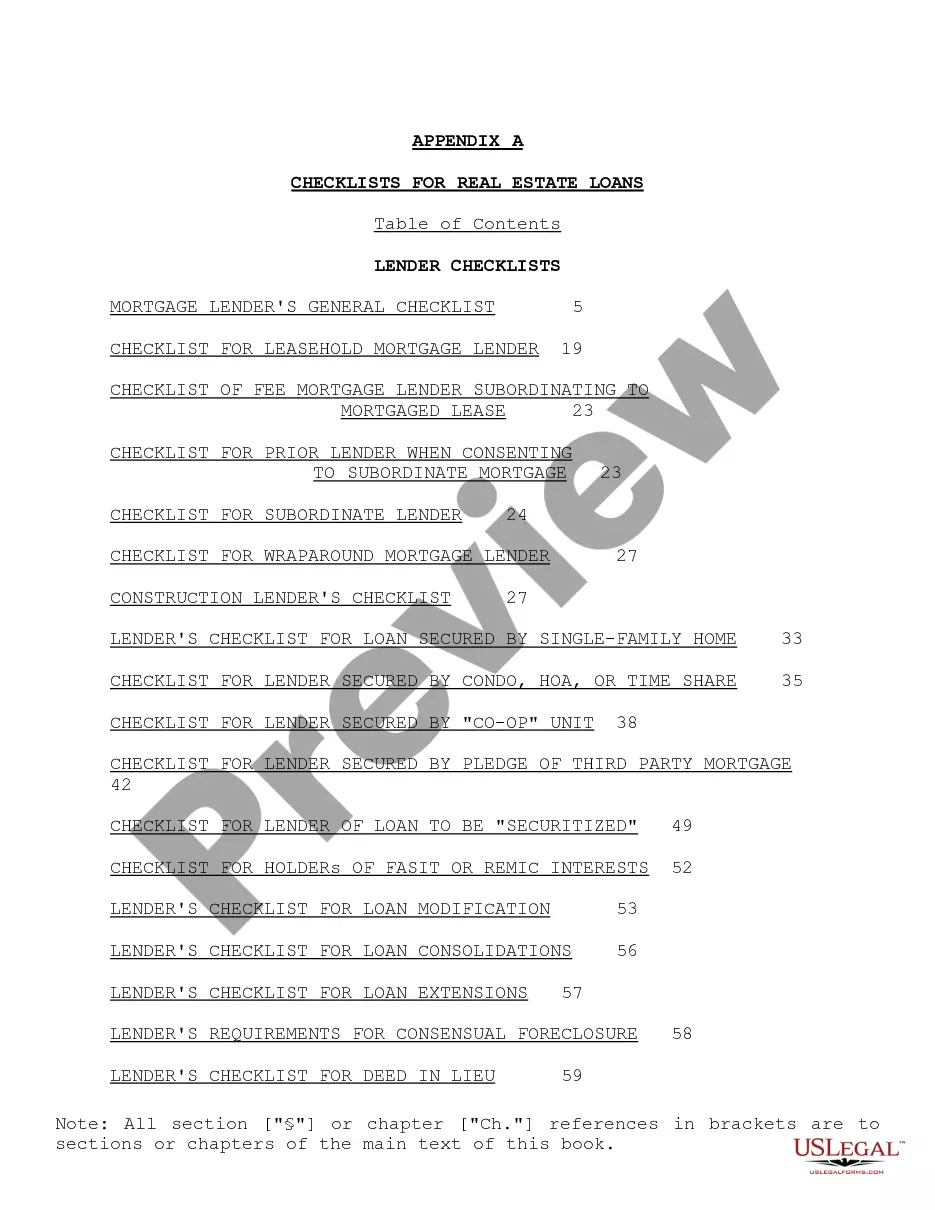

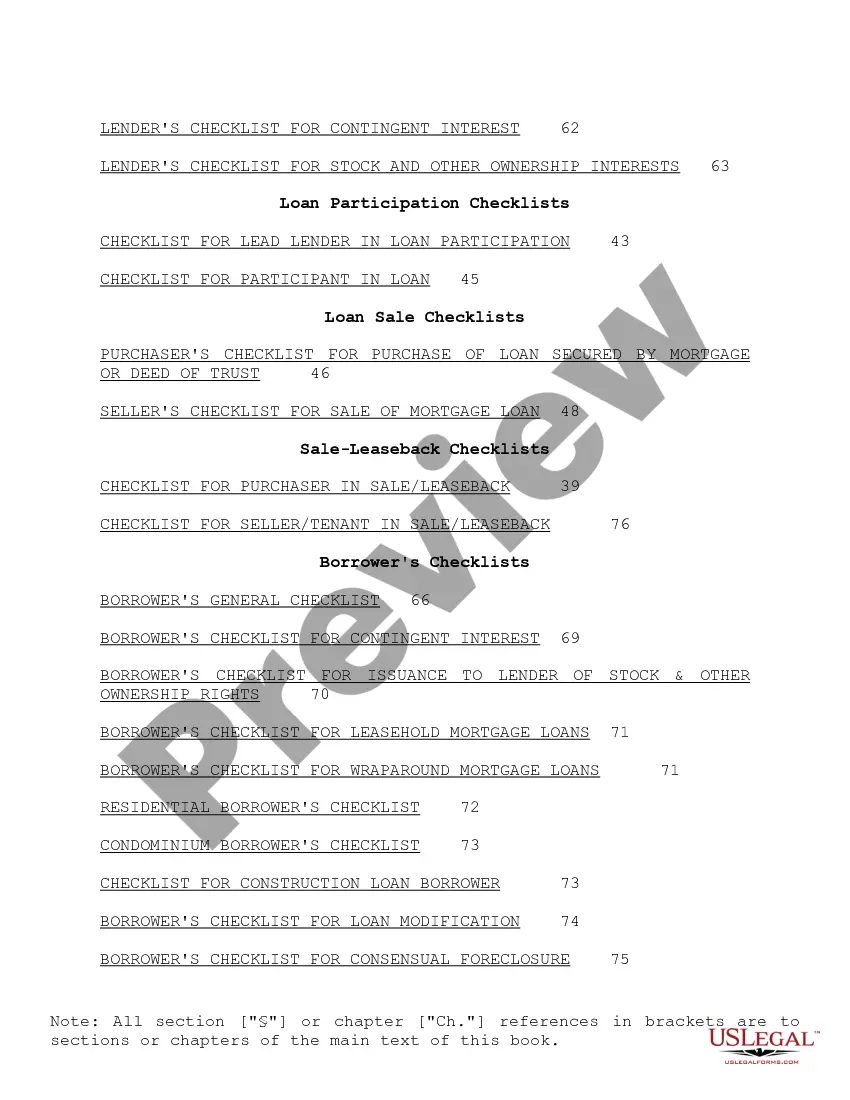

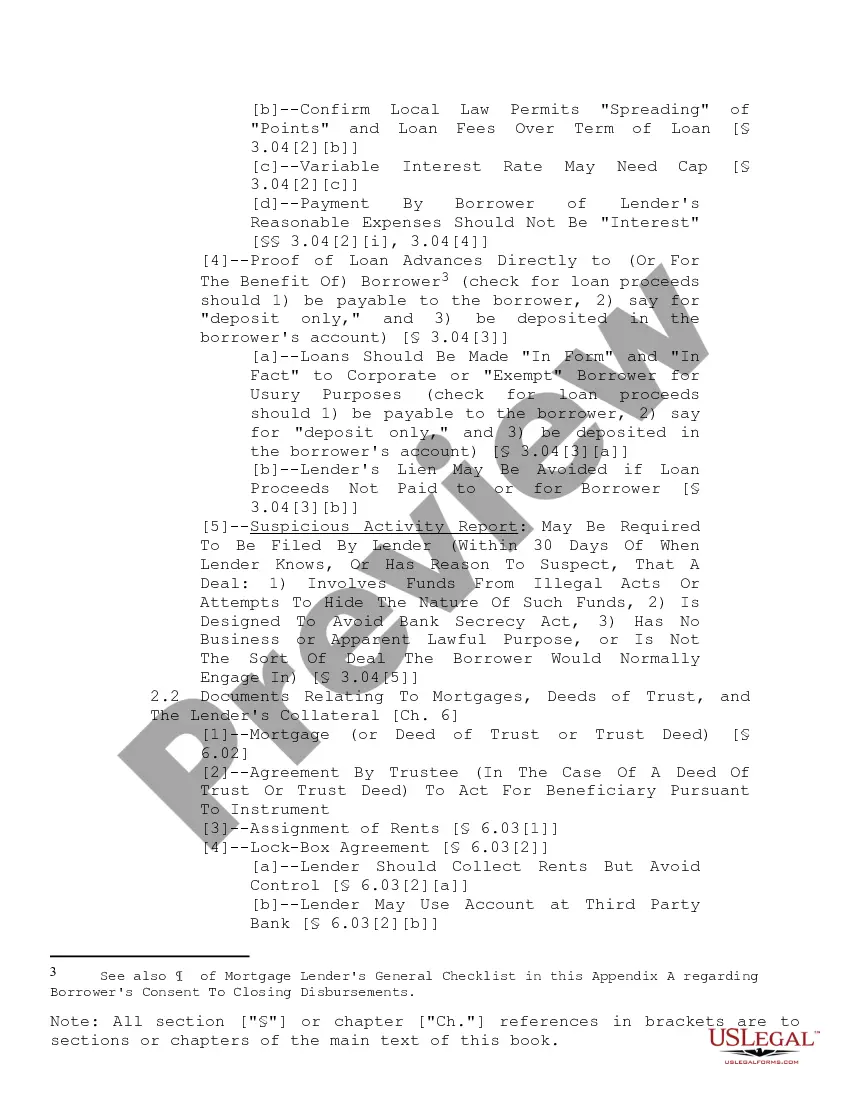

"Checklist for Real Estate Loans" is a American Lawyer Media form. This consist of many checklist that can be used for real estate loans.

Title: The Ultimate Guide to New Jersey Checklist for Real Estate Loans Introduction: Navigating through the intricacies of real estate loans can be a daunting task, particularly in the state of New Jersey. To ensure a smooth borrowing experience, it is crucial to familiarize yourself with the New Jersey Checklist for Real Estate Loans. In this comprehensive guide, we will delve into the finer details of this checklist, its significance, and different types of loan checklists relevant to the New Jersey real estate market. Key Terms: New Jersey, real estate loans, checklist, borrowing, loan requirements, property, mortgage lenders, financial institutions, credit score. I. Understanding the New Jersey Checklist for Real Estate Loans: 1. Purpose: The New Jersey Checklist for Real Estate Loans acts as a comprehensive guideline to assist borrowers, mortgage lenders, and financial institutions throughout the loan application process. 2. Standard Requirements: a. Creditworthiness: A credit score is evaluated to determine the borrower's financial stability and ability to make mortgage payments regularly. b. Employment Verification: Lenders verify the borrower's employment status and stability to mitigate potential default risks. c. Income Documentation: Comprehensive income documentation showcases the borrower's ability to repay the loan, typically requiring tax returns, pay stubs, and bank statements. d. Property Appraisal: A professional appraisal ensures the property's fair market value matches the loan amount requested. II. Different Types of New Jersey Checklist for Real Estate Loans: 1. Conventional Loan Checklist: Conventional loans adhere to the guidelines stipulated by government-sponsored entities like Fannie Mae and Freddie Mac. Key requirements: — Good credit score (typically 620 or higher) — Proof of stable employment anincomeom— - Down payment (typically 10-20% of the property's value) — Property appraisal aninspectionio— - Debt-to-income ratio within acceptable limits 2. FHA Loan Checklist (Federal Housing Administration): FHA loans are insured by the Federal Housing Administration, making them suitable for first-time homebuyers or borrowers with limited financial resources. Key requirements: — Decent credit score (580 or higher— - Affordable down payment (as low as 3.5%) — Property must meet minimum property standards — Stable employment anincomeom— - Debt-to-income ratio within acceptable limits 3. VA Loan Checklist (Veterans Affairs): Reserved for veterans, active-duty service members, and eligible surviving spouses, VA loans provide benefits such as now down payment and lower interest rates. Key requirements: — Certificate of Eligibility (COE— - Minimum credit score (typically 620 or higher) — Stable employment and sufficient income for monthly loan payments — Property must meet VA's Minimum Property Requirements (MPR) — Debt-to-income ratio within acceptable limits 4. USDA Loan Checklist (United States Department of Agriculture): USDA loans are designed to promote homeownership in rural and suburban areas. They offer low-interest rates and require now down payment. Key requirements: — Property must be located within eligible USDA areas — Minimum credit score (typically 640 or higher) — Proof of stablincomeom— - Property must meet USDA's Minimum Property Requirements (MPR) — Debt-to-income ratio within acceptable limits Conclusion: Whether you are a prospective buyer or a real estate agent, it is imperative to familiarize yourself with the New Jersey Checklist for Real Estate Loans. By understanding the specific requirements for each loan type, you can ensure a successful loan application and secure your dream property with confidence in the vibrant real estate market of New Jersey.Title: The Ultimate Guide to New Jersey Checklist for Real Estate Loans Introduction: Navigating through the intricacies of real estate loans can be a daunting task, particularly in the state of New Jersey. To ensure a smooth borrowing experience, it is crucial to familiarize yourself with the New Jersey Checklist for Real Estate Loans. In this comprehensive guide, we will delve into the finer details of this checklist, its significance, and different types of loan checklists relevant to the New Jersey real estate market. Key Terms: New Jersey, real estate loans, checklist, borrowing, loan requirements, property, mortgage lenders, financial institutions, credit score. I. Understanding the New Jersey Checklist for Real Estate Loans: 1. Purpose: The New Jersey Checklist for Real Estate Loans acts as a comprehensive guideline to assist borrowers, mortgage lenders, and financial institutions throughout the loan application process. 2. Standard Requirements: a. Creditworthiness: A credit score is evaluated to determine the borrower's financial stability and ability to make mortgage payments regularly. b. Employment Verification: Lenders verify the borrower's employment status and stability to mitigate potential default risks. c. Income Documentation: Comprehensive income documentation showcases the borrower's ability to repay the loan, typically requiring tax returns, pay stubs, and bank statements. d. Property Appraisal: A professional appraisal ensures the property's fair market value matches the loan amount requested. II. Different Types of New Jersey Checklist for Real Estate Loans: 1. Conventional Loan Checklist: Conventional loans adhere to the guidelines stipulated by government-sponsored entities like Fannie Mae and Freddie Mac. Key requirements: — Good credit score (typically 620 or higher) — Proof of stable employment anincomeom— - Down payment (typically 10-20% of the property's value) — Property appraisal aninspectionio— - Debt-to-income ratio within acceptable limits 2. FHA Loan Checklist (Federal Housing Administration): FHA loans are insured by the Federal Housing Administration, making them suitable for first-time homebuyers or borrowers with limited financial resources. Key requirements: — Decent credit score (580 or higher— - Affordable down payment (as low as 3.5%) — Property must meet minimum property standards — Stable employment anincomeom— - Debt-to-income ratio within acceptable limits 3. VA Loan Checklist (Veterans Affairs): Reserved for veterans, active-duty service members, and eligible surviving spouses, VA loans provide benefits such as now down payment and lower interest rates. Key requirements: — Certificate of Eligibility (COE— - Minimum credit score (typically 620 or higher) — Stable employment and sufficient income for monthly loan payments — Property must meet VA's Minimum Property Requirements (MPR) — Debt-to-income ratio within acceptable limits 4. USDA Loan Checklist (United States Department of Agriculture): USDA loans are designed to promote homeownership in rural and suburban areas. They offer low-interest rates and require now down payment. Key requirements: — Property must be located within eligible USDA areas — Minimum credit score (typically 640 or higher) — Proof of stablincomeom— - Property must meet USDA's Minimum Property Requirements (MPR) — Debt-to-income ratio within acceptable limits Conclusion: Whether you are a prospective buyer or a real estate agent, it is imperative to familiarize yourself with the New Jersey Checklist for Real Estate Loans. By understanding the specific requirements for each loan type, you can ensure a successful loan application and secure your dream property with confidence in the vibrant real estate market of New Jersey.