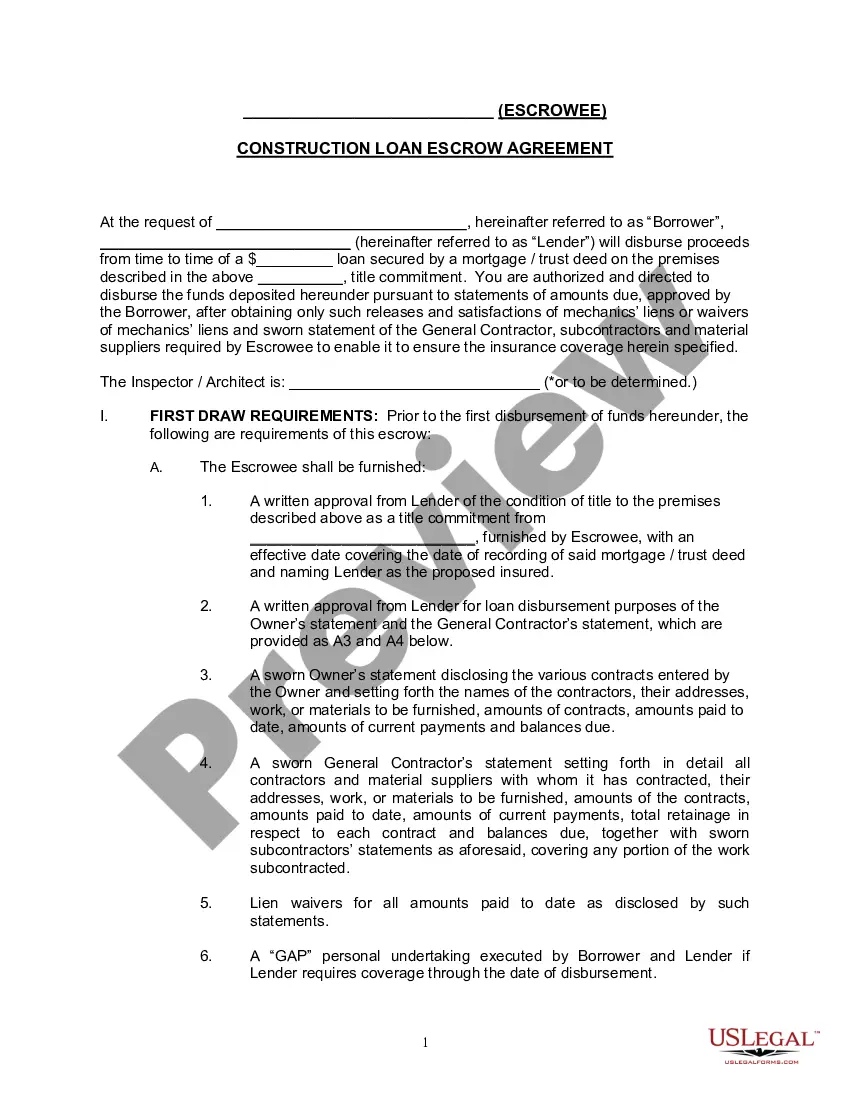

"A construction loan agreement isa legally binding contract between the lender and the borrower, detailing the promises and commitments both parties have to uphold through successful project completion.

A Loan Agreement is a document between a borrower and lender that details the loan repayment schedule.

The Loan Agreement protects the lender by enforcing the borrower's pledge to repay the loan; payment via regular payments or lump sums. The borrower may also find the loan contract useful because it records the details of the loan for their records and helps keep track of payments.

Loan agreements generally include information about:

* The location.

* The loan amount.

* Interest and late fees.

* Repayment method.

* Collateral and insurance."

New Jersey Construction Loan Agreement

Category:

State:

Multi-State

Control #:

US-ENTREP-0065-1

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Construction Loan Agreement?

Choosing the right legal papers design can be a have difficulties. Needless to say, there are tons of web templates available online, but how will you find the legal form you require? Use the US Legal Forms web site. The support delivers a huge number of web templates, for example the New Jersey Construction Loan Agreement, that can be used for company and private needs. Each of the varieties are checked out by specialists and satisfy federal and state needs.

Should you be previously listed, log in in your accounts and then click the Obtain key to have the New Jersey Construction Loan Agreement. Utilize your accounts to look from the legal varieties you have bought in the past. Visit the My Forms tab of your accounts and obtain another backup of the papers you require.

Should you be a fresh consumer of US Legal Forms, here are straightforward instructions for you to adhere to:

- Initial, make certain you have selected the right form for your personal metropolis/area. You can check out the form using the Preview key and study the form information to ensure this is basically the best for you.

- In case the form does not satisfy your needs, take advantage of the Seach field to discover the proper form.

- Once you are positive that the form is suitable, go through the Get now key to have the form.

- Pick the costs prepare you would like and enter in the necessary information. Design your accounts and pay for your order utilizing your PayPal accounts or credit card.

- Opt for the submit structure and down load the legal papers design in your product.

- Complete, revise and print and signal the acquired New Jersey Construction Loan Agreement.

US Legal Forms will be the biggest catalogue of legal varieties for which you can discover different papers web templates. Use the service to down load skillfully-made documents that adhere to state needs.

Form popularity

FAQ

Loan agreements typically include covenants, value of collateral involved, guarantees, interest rate terms and the duration over which it must be repaid. Default terms should be clearly detailed to avoid confusion or potential legal court action.

A loan agreement should be structured to include information about the borrower and the lender, the loan amount, and repayment terms, including interest charges and a timeline for repaying the loan. It should also spell out penalties for late payments or default and should be clear about expectations between parties.

A Promissory note is essentially an unconditional written promise to repay a loan or other debts, at a fixed or determinable future date. Although it is legally enforceable, a promissory note is less formal than a loan agreement and is suitable where smaller sums of money are involved.

Include key terms of the loan, such as the lender and borrower's contact information, the reason for the loan, what is being loaned, the interest rate, the repayment plan, what would happen if the borrower can't make the payments, and more. The amount of the loan, also known as the principal amount.

Construction Loans Compared Type of loanBest forConstruction-to-permanent loanHomeowners who want to save on closing costs and lock in mortgage financingConstruction-only loanThose who have a large amount of cash on hand or who intend to pay off the construction loan with the sale of their previous home2 more rows ?

Take the following steps to write a business loan application letter: Include a header. ... Add a subject line. ... Start with a greeting. ... Give a summary of the request. ... Provide necessary business information. ... Explain the purpose of the business loan. ... Describe the plan to repay the loan. ... Close the letter.

What should be in a personal loan contract? Names and addresses of the lender and the borrower. Information about the loan co-borrower or cosigner, if it's a joint personal loan. Loan amount and the method for disbursement (lump sum, installments, etc.) Date the loan was provided. Expected repayment date.

The purpose for which funds may be used. Loan funding mechanics, and applicable interest. Repayment obligations. Representations, warranties and undertakings.