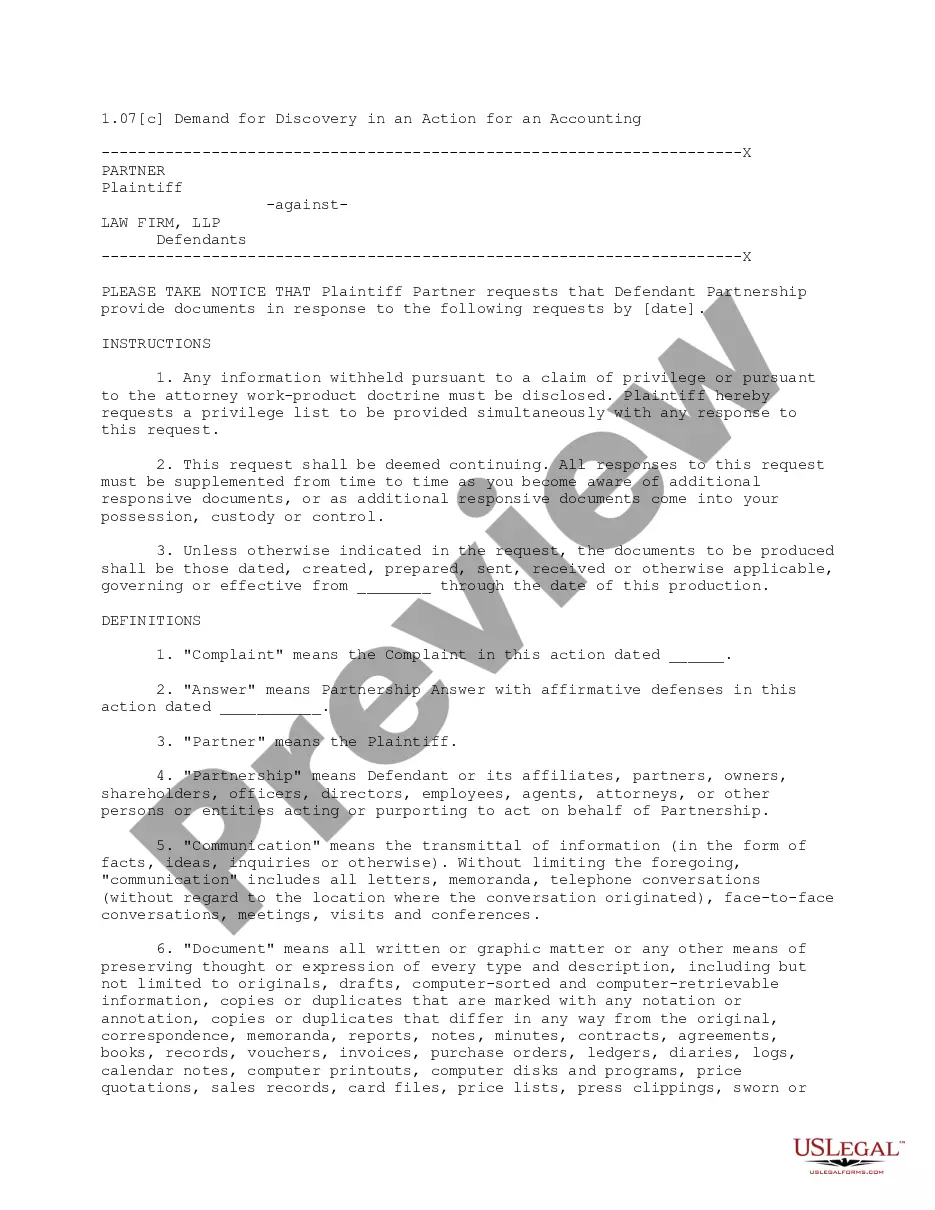

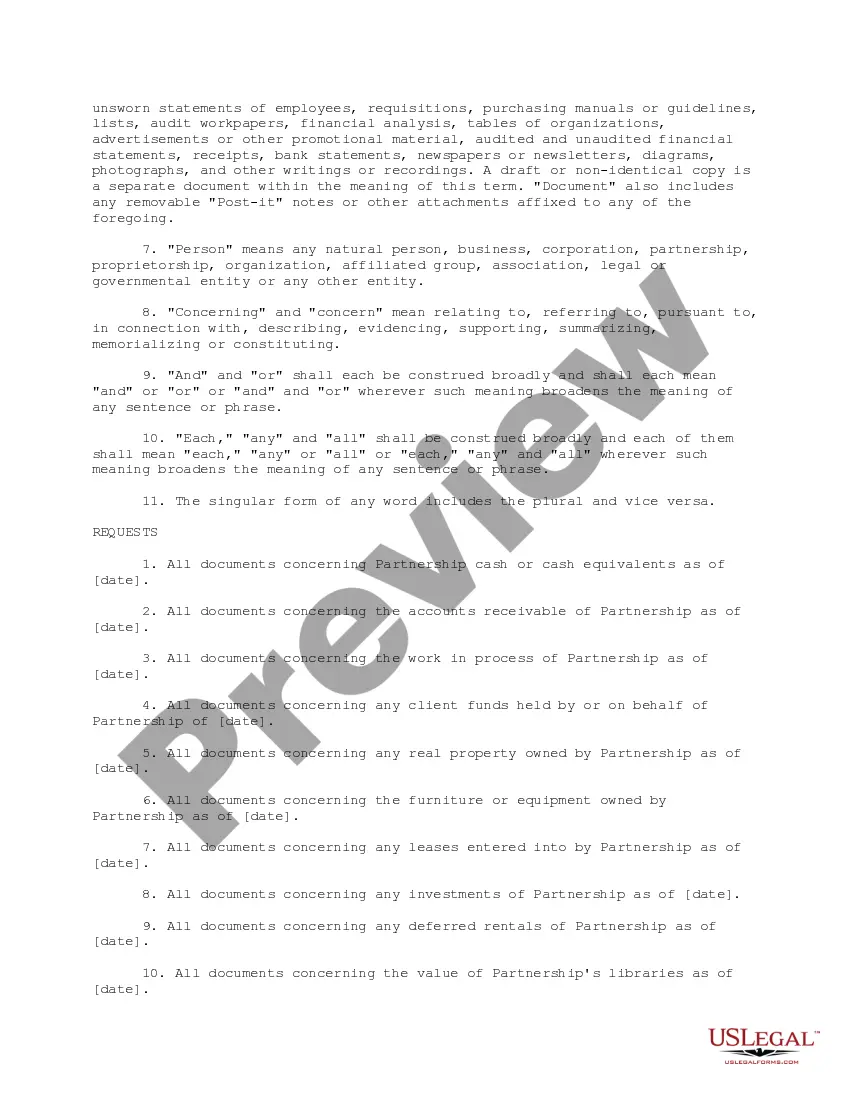

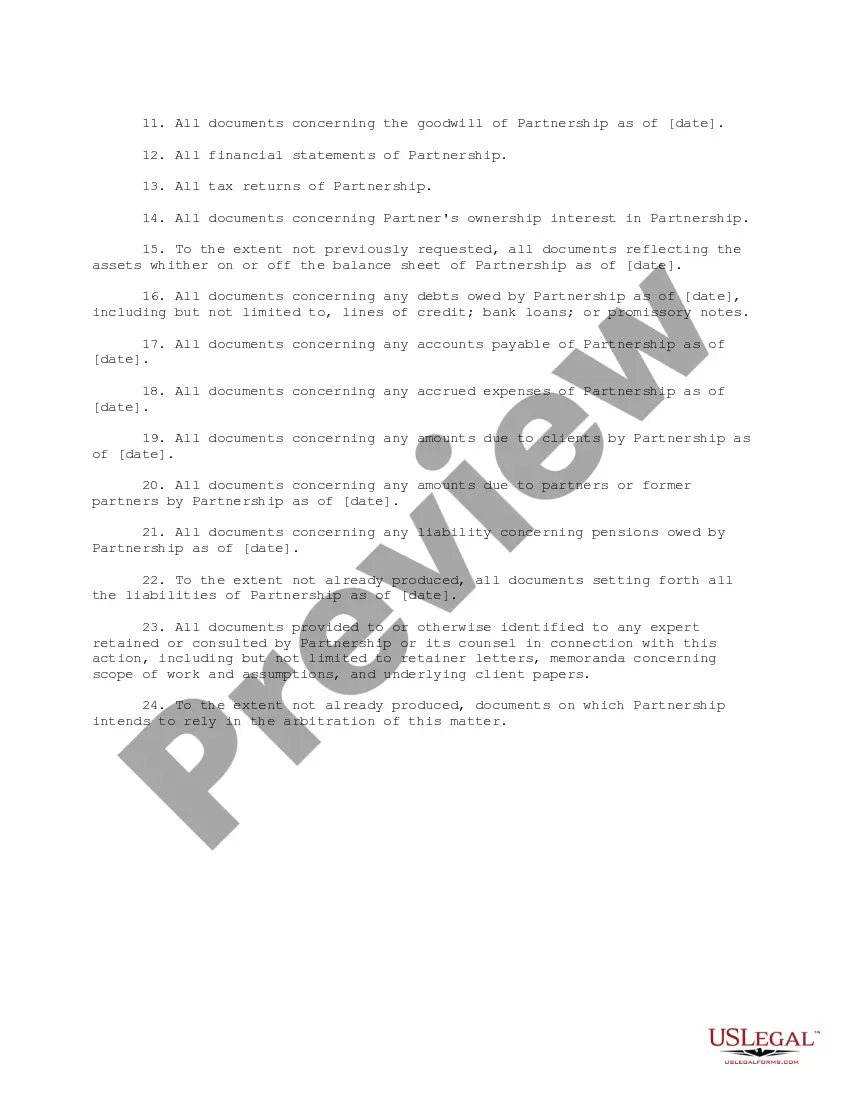

This document is the plaintiff's demand for discovery in a lawsuit filed by a former partner seeking an accounting of his former firm, when the partnership agreement did not provide for an accounting. It contains a request for production of documents.

New Jersey Demand for Discovery in an Action for an Accounting is a legal process that allows parties involved in a dispute related to accounting matters to gather information and evidence relevant to their case. This demand is made to ensure transparency and the disclosure of financial records or relevant documents necessary to assess the financials of the party being investigated. Keywords: New Jersey, demand for discovery, action for accounting, legal process, financial records, relevant documents, transparency. There are different types of New Jersey Demand for Discovery in an Action for an Accounting, including: 1. General Demand for Discovery: This is the most common type of demand and requires the party being investigated to disclose all relevant financial records, including balance sheets, income statements, financial statements, tax returns, bank statements, and any other documents related to the financial transactions in question. 2. Specific Demand for Discovery: In some cases, the party seeking an accounting may need to specify certain documents or information that they believe are crucial to their case. This type of demand allows the requesting party to target specific financial records or documents they believe will help prove their claims. 3. Interrogatories: Interrogatories are written questions presented to the opposing party, requesting detailed information about their financial transactions, business practices, and any other information relevant to the accounting matter at hand. These questions must be answered under oath. 4. Depositions: Depositions involve oral questioning of witnesses, including officers or employees of the party being investigated. This type of discovery method allows parties to gather testimonial evidence regarding financial matters or acquire additional information that may not be found in documents alone. 5. Subpoenas: A party may also issue a subpoena to acquire financial records or documents from a third party, such as banks, financial institutions, or other relevant entities. Subpoenas can be an effective way to obtain information that the opposing party may not willingly disclose. In conclusion, New Jersey Demand for Discovery in an Action for an Accounting is an essential legal process that enables parties involved in an accounting dispute to collect relevant financial records and documents. The different types of demands, including general and specific demands, interrogatories, depositions, and subpoenas, provide tools to obtain transparency and gather evidence for a successful resolution of the accounting dispute.

New Jersey Demand for Discovery in an Action for an Accounting is a legal process that allows parties involved in a dispute related to accounting matters to gather information and evidence relevant to their case. This demand is made to ensure transparency and the disclosure of financial records or relevant documents necessary to assess the financials of the party being investigated. Keywords: New Jersey, demand for discovery, action for accounting, legal process, financial records, relevant documents, transparency. There are different types of New Jersey Demand for Discovery in an Action for an Accounting, including: 1. General Demand for Discovery: This is the most common type of demand and requires the party being investigated to disclose all relevant financial records, including balance sheets, income statements, financial statements, tax returns, bank statements, and any other documents related to the financial transactions in question. 2. Specific Demand for Discovery: In some cases, the party seeking an accounting may need to specify certain documents or information that they believe are crucial to their case. This type of demand allows the requesting party to target specific financial records or documents they believe will help prove their claims. 3. Interrogatories: Interrogatories are written questions presented to the opposing party, requesting detailed information about their financial transactions, business practices, and any other information relevant to the accounting matter at hand. These questions must be answered under oath. 4. Depositions: Depositions involve oral questioning of witnesses, including officers or employees of the party being investigated. This type of discovery method allows parties to gather testimonial evidence regarding financial matters or acquire additional information that may not be found in documents alone. 5. Subpoenas: A party may also issue a subpoena to acquire financial records or documents from a third party, such as banks, financial institutions, or other relevant entities. Subpoenas can be an effective way to obtain information that the opposing party may not willingly disclose. In conclusion, New Jersey Demand for Discovery in an Action for an Accounting is an essential legal process that enables parties involved in an accounting dispute to collect relevant financial records and documents. The different types of demands, including general and specific demands, interrogatories, depositions, and subpoenas, provide tools to obtain transparency and gather evidence for a successful resolution of the accounting dispute.