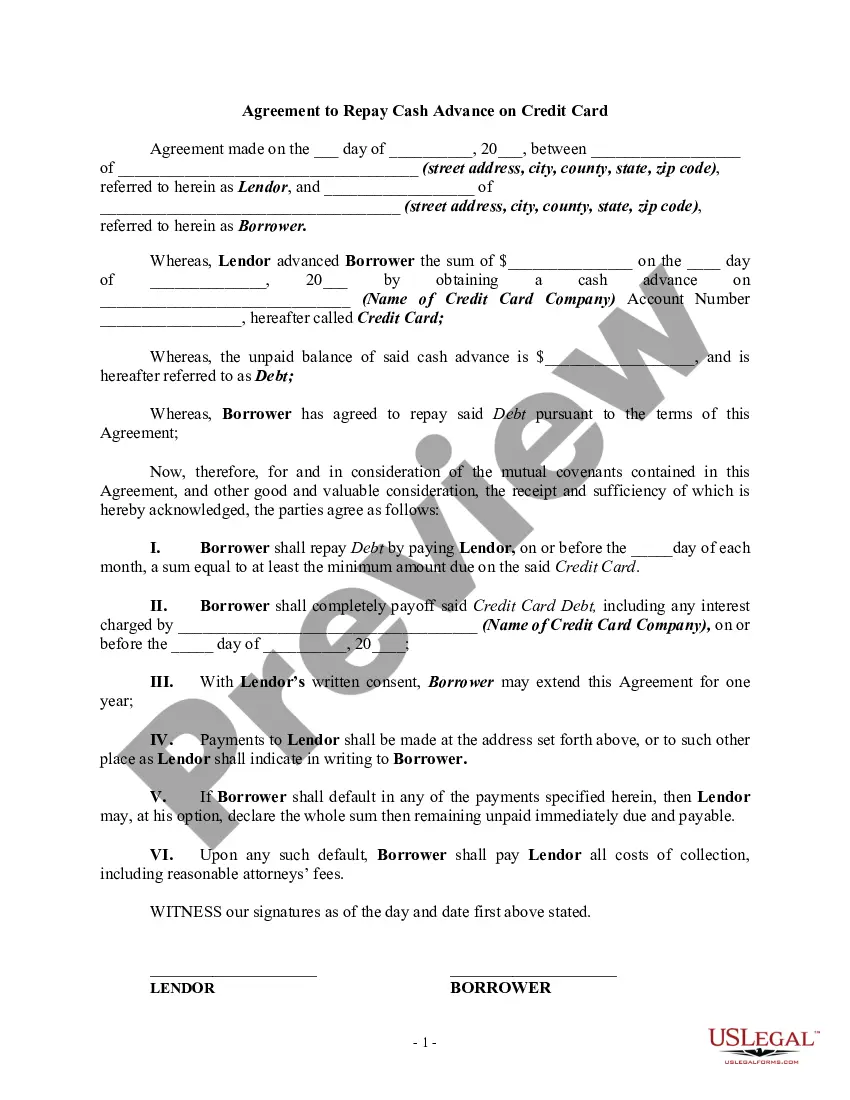

New Mexico Agreement to Repay Cash Advance on Credit Card is a legally binding contract designed for individuals who wish to borrow money in the form of a cash advance from their credit card issuer. This agreement outlines the terms and conditions of the loan, ensuring both the cardholder and the credit card company are protected throughout the repayment process. The primary purpose of a New Mexico Agreement to Repay Cash Advance on Credit Card is to establish the responsibilities of each party involved. It clearly specifies the amount borrowed, the interest rate, the repayment schedule, and any additional fees or charges applied. This agreement ensures transparency and prevents any misunderstandings or disputes that may arise in the future. There are several types of New Mexico Agreement to Repay Cash Advance on Credit Card available: 1. Standard Repayment Agreement: This is the most common type of agreement wherein the borrower agrees to repay the cash advance with interest within a predetermined period, usually ranging from a few months to several years. The repayment amount may be fixed or adjustable based on the terms outlined in the agreement. 2. Deferred Repayment Agreement: This type of agreement allows the borrower to delay the repayment of the cash advance for a specified period. The borrower may be required to pay only the interest during this period, with the principal amount due at a later date. 3. Balloon Payment Agreement: In this arrangement, the borrower agrees to make smaller periodic payments throughout the loan term, with a larger "balloon payment" due at the end. The balloon payment includes the remaining principal, accrued interest, and any additional fees. 4. Installment Agreement: This type of agreement breaks down the repayment into equal monthly installments over an agreed-upon period. The borrower pays a fixed amount each month, covering both the principal and the interest until the loan is fully repaid. Regardless of the type of New Mexico Agreement to Repay Cash Advance on Credit Card, borrowers must carefully review all the terms and conditions before signing. It is essential to ensure the agreement aligns with their repayment capabilities and financial goals. Failure to fulfill the obligations outlined in the agreement can result in penalties, increased interest rates, and potential damage to the borrower's credit score.

New Mexico Agreement to Repay Cash Advance on Credit Card

Description

How to fill out New Mexico Agreement To Repay Cash Advance On Credit Card?

It is possible to devote time on-line trying to find the legal document template that suits the federal and state needs you will need. US Legal Forms supplies thousands of legal forms which can be analyzed by specialists. It is possible to obtain or print out the New Mexico Agreement to Repay Cash Advance on Credit Card from my service.

If you already have a US Legal Forms account, you can log in and then click the Acquire button. Following that, you can complete, change, print out, or indication the New Mexico Agreement to Repay Cash Advance on Credit Card. Every legal document template you buy is your own for a long time. To get another duplicate of the purchased kind, visit the My Forms tab and then click the corresponding button.

Should you use the US Legal Forms site the first time, follow the easy guidelines below:

- Initial, make certain you have chosen the correct document template for the county/town that you pick. Read the kind information to ensure you have selected the proper kind. If readily available, make use of the Review button to search throughout the document template at the same time.

- If you would like get another variation of the kind, make use of the Lookup area to get the template that meets your requirements and needs.

- Upon having located the template you need, click Acquire now to carry on.

- Pick the pricing plan you need, type in your credentials, and register for your account on US Legal Forms.

- Total the deal. You can use your charge card or PayPal account to cover the legal kind.

- Pick the file format of the document and obtain it in your gadget.

- Make alterations in your document if possible. It is possible to complete, change and indication and print out New Mexico Agreement to Repay Cash Advance on Credit Card.

Acquire and print out thousands of document templates using the US Legal Forms Internet site, that provides the biggest variety of legal forms. Use specialist and status-specific templates to handle your business or person needs.