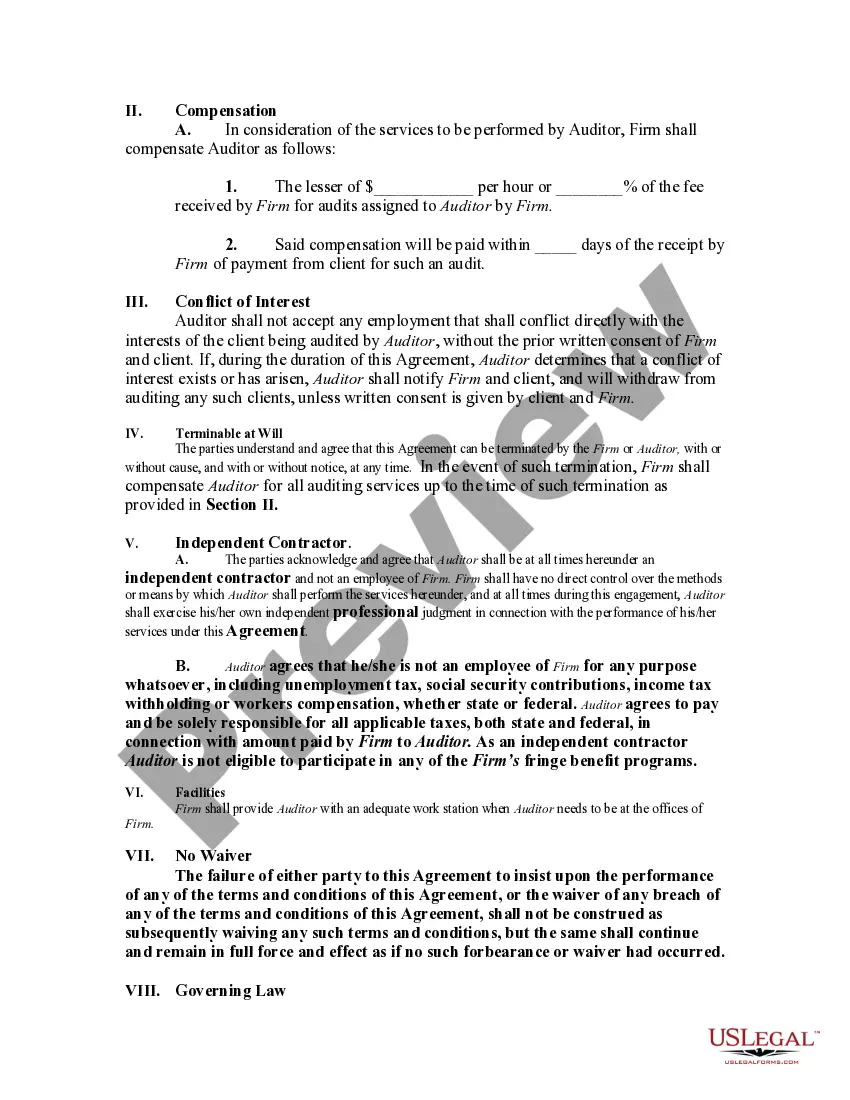

Although no definite rule exists for determining whether one is an independent contractor or an employee, certain indicia of the status of an independent contractor are recognized, and the insertion of provisions embodying these indicia in the contract will help to insure that the relationship reflects the intention of the parties. These indicia generally relate to the basic issue of control. The general test of what constitutes an independent contractor relationship involves which party has the right to direct what is to be done, and how and when. Another important test involves the method of payment of the contractor.

Title: New Mexico Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor Keywords: New Mexico, agreement, accounting firm, employ auditor, self-employed, independent contractor Introduction: The New Mexico Agreement by Accounting Firm to Employ Auditor as a Self-Employed Independent Contractor is a legally binding agreement between an accounting firm, operating in the state of New Mexico, and an auditor who is seeking employment as a self-employed independent contractor. This agreement outlines the terms and conditions of the employment arrangement, ensuring clarity and mutual understanding between the accounting firm and the auditor. Types of New Mexico Agreements by Accounting Firms to Employ Auditors as Self-Employed Independent Contractors: 1. Standard New Mexico Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: This is the most common type of agreement used by accounting firms in New Mexico when hiring auditors as self-employed independent contractors. It covers the general terms and conditions applicable to the employment arrangement, such as compensation, work schedule, performance expectations, and confidentiality obligations. 2. New Mexico Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor with Non-Compete Clause: In certain cases, accounting firms may require auditors to sign an agreement that includes a non-compete clause. This clause restricts the auditor from engaging in similar or competing work with another accounting firm within a specific geographic area or for a particular duration. This type of agreement protects the accounting firm's interests and ensures the continuity of client relationships. 3. New Mexico Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor with Confidentiality Agreement: To maintain the confidentiality of sensitive client information, accounting firms may include a separate confidentiality agreement within the employment agreement. This agreement emphasizes the importance of maintaining client confidentiality and imposes certain obligations on the auditor to safeguard the firm's intellectual property, trade secrets, and client data. 4. New Mexico Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor with Scope of Work Addendum: In cases where the auditor's role involves specific projects or tasks, accounting firms may add a scope of work addendum to the agreement. This addendum provides a detailed description of the specific responsibilities, deliverables, and timelines associated with the auditor's engagement. It ensures that both parties have a clear understanding of the scope of work agreed upon. Conclusion: The New Mexico Agreement by Accounting Firm to Employ Auditor as a Self-Employed Independent Contractor is a vital document that establishes the working relationship between accounting firms and auditors in New Mexico. By crafting different types of agreements tailored to their specific needs, accounting firms can ensure efficient, transparent, and legally compliant employment arrangements with self-employed independent contractors.Title: New Mexico Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor Keywords: New Mexico, agreement, accounting firm, employ auditor, self-employed, independent contractor Introduction: The New Mexico Agreement by Accounting Firm to Employ Auditor as a Self-Employed Independent Contractor is a legally binding agreement between an accounting firm, operating in the state of New Mexico, and an auditor who is seeking employment as a self-employed independent contractor. This agreement outlines the terms and conditions of the employment arrangement, ensuring clarity and mutual understanding between the accounting firm and the auditor. Types of New Mexico Agreements by Accounting Firms to Employ Auditors as Self-Employed Independent Contractors: 1. Standard New Mexico Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: This is the most common type of agreement used by accounting firms in New Mexico when hiring auditors as self-employed independent contractors. It covers the general terms and conditions applicable to the employment arrangement, such as compensation, work schedule, performance expectations, and confidentiality obligations. 2. New Mexico Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor with Non-Compete Clause: In certain cases, accounting firms may require auditors to sign an agreement that includes a non-compete clause. This clause restricts the auditor from engaging in similar or competing work with another accounting firm within a specific geographic area or for a particular duration. This type of agreement protects the accounting firm's interests and ensures the continuity of client relationships. 3. New Mexico Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor with Confidentiality Agreement: To maintain the confidentiality of sensitive client information, accounting firms may include a separate confidentiality agreement within the employment agreement. This agreement emphasizes the importance of maintaining client confidentiality and imposes certain obligations on the auditor to safeguard the firm's intellectual property, trade secrets, and client data. 4. New Mexico Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor with Scope of Work Addendum: In cases where the auditor's role involves specific projects or tasks, accounting firms may add a scope of work addendum to the agreement. This addendum provides a detailed description of the specific responsibilities, deliverables, and timelines associated with the auditor's engagement. It ensures that both parties have a clear understanding of the scope of work agreed upon. Conclusion: The New Mexico Agreement by Accounting Firm to Employ Auditor as a Self-Employed Independent Contractor is a vital document that establishes the working relationship between accounting firms and auditors in New Mexico. By crafting different types of agreements tailored to their specific needs, accounting firms can ensure efficient, transparent, and legally compliant employment arrangements with self-employed independent contractors.