After the filing of the bankruptcy petition, the debtor needs protection from the collection efforts of its creditors. Therefore, the bankruptcy law provides that the filing of either a voluntary or involuntary petition operates as an automatic stay which prevents creditors from taking action against the debtor. This is similar to an injunction against the creditors of the debtor. The automatic stay ends when the bankruptcy case is closed or dismissed or when the debtor is granted a discharge.

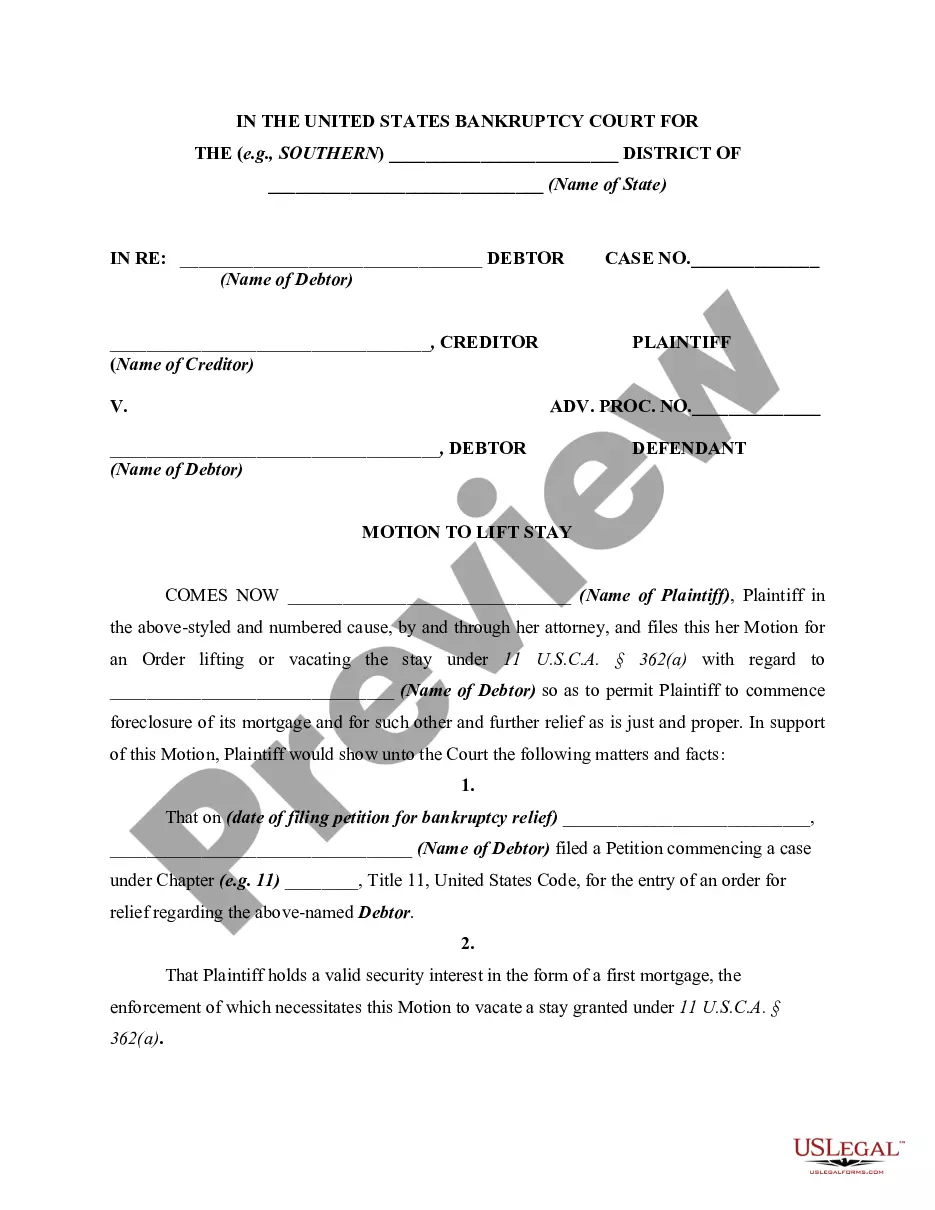

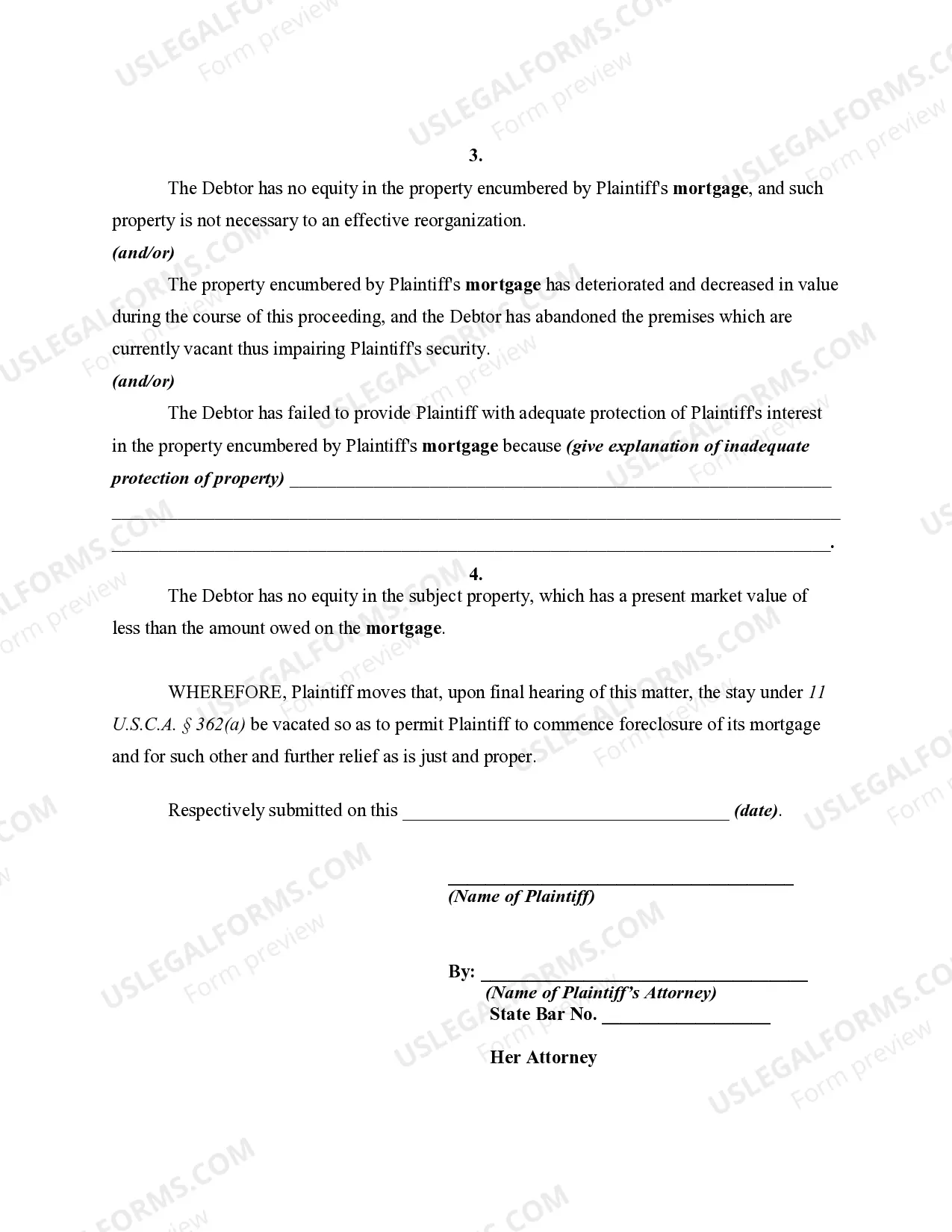

New Mexico Motion in Bankruptcy Court by Mortgagee to Vacate Stay to Permit Foreclosure of Mortgage on Debtor's Real Property is a legal process that allows a mortgage lender to request permission from a bankruptcy court to proceed with foreclosure proceedings on a debtor's property. This motion is typically filed when the mortgagee believes that the debtor is not adequately protecting the property's value or is in default of their mortgage payments. There are several types of motions that may be filed by a mortgagee in New Mexico bankruptcy court to vacate the stay and proceed with foreclosure: 1. Motion to Vacate Stay: This motion requests the court to lift the automatic stay, which is an injunction that halts any foreclosure proceedings or collection efforts against the debtor upon filing for bankruptcy. The mortgagee argues that lifting the stay is necessary to protect their rights and interests in the property. 2. Motion for Relief from Stay: This motion seeks relief from the automatic stay, allowing the mortgagee to continue with foreclosure outside the bankruptcy proceedings. It is typically filed when the mortgagee believes that the debtor has no equity in the property and cannot maintain mortgage payments. 3. Motion to Vacate Stay and Reconsider: In some cases, a mortgagee may file this motion to request both the lifting of the stay and reconsideration of the debtor's bankruptcy protection. The mortgagee may argue that the debtor has no feasible plan to reorganize their finances, and foreclosure is the best course of action. 4. Motion to Modify Stay: This motion asks the court to modify the automatic stay to allow the mortgagee to proceed with specific actions related to foreclosure, such as conducting an appraisal or property inspection. 5. Motion for Expedited Consideration: In urgent cases, where the mortgagee believes there is an immediate need to proceed with foreclosure to prevent further loss, a motion for expedited consideration may be filed. The mortgagee must demonstrate compelling reasons for the court to prioritize the motion over other pending matters. 6. Motion for Relief from Co-debtor Stay: If the bankruptcy involves co-debtors, the mortgagee may file this motion to seek relief from the automatic stay applied to co-debtors. This allows the mortgagee to initiate or continue foreclosure proceedings against the co-debtor's interested in the property. To successfully argue for the vacating of the stay and permit foreclosure, the mortgagee must provide supporting evidence, such as the debtor's failure to make mortgage payments or prospects of preserving the property's value through other means. The court will evaluate the motion and consider factors like the debtor's ability to reorganize their finances and potential harm to the creditor if the stay is not lifted. Ultimately, the court will decide whether to allow the mortgagee to proceed with foreclosure on the debtor's real property.