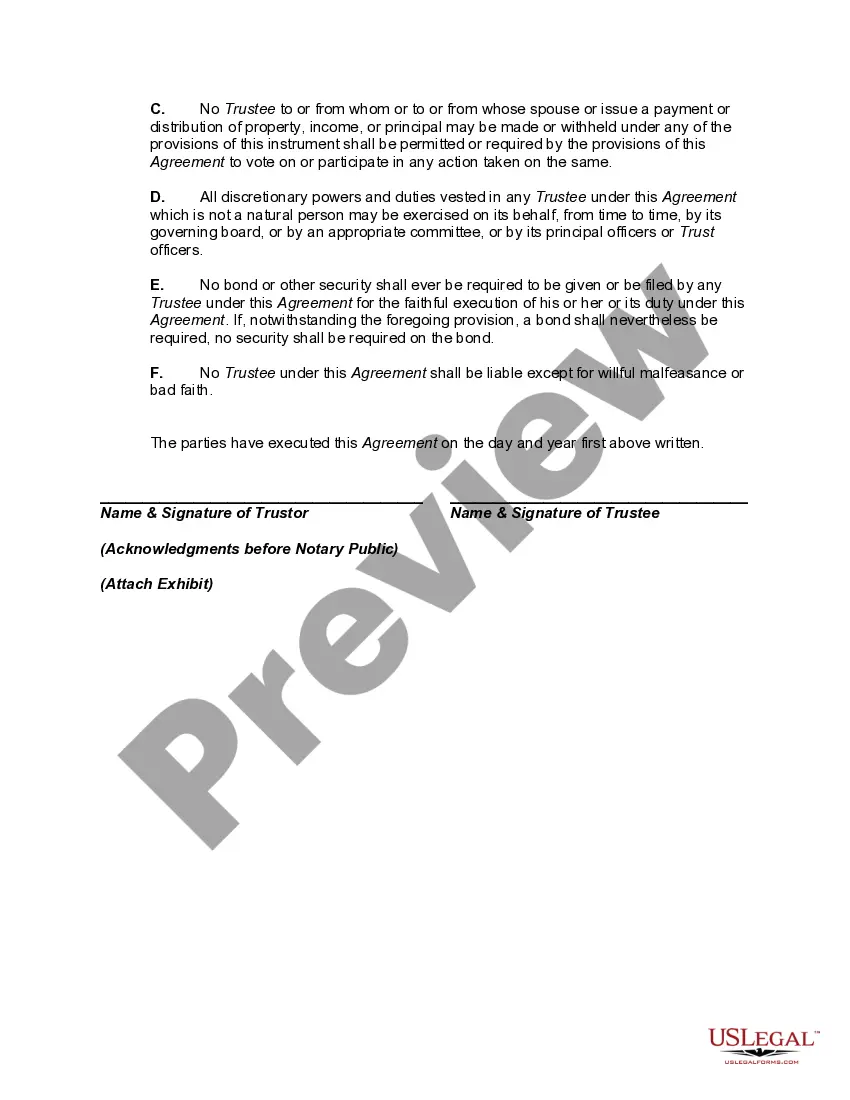

An irrevocable trust is an arrangement in which the grantor departs with ownership and control of property. Usually this involves a gift of the property to the trust. The trust then stands as a separate taxable entity and pays tax on its accumulated income.

A discretionary trust is a trust where the beneficiaries and/or their entitlements to the trust fund are not fixed, but are determined by the criteria set out in the trust instrument by trustor. Discretionary trusts can be discretionary in two respects. First, the trustees usually have the power to determine which beneficiaries (from within the class) will receive payments from the trust. Second, trustees can select the amount of trust property that the beneficiary receives. Although most discretionary trusts allow both types of discretion, either can be allowed on its own. It is permissible in most legal systems for a trust to have a fixed number of beneficiaries and for the trustees to have discretion as to how much each beneficiary receives.

A New Mexico Irrevocable Trust Agreement for the Benefit of Trust or's Children with Discretionary Distributions of Income and Principal is a legal document that establishes a trust in the state of New Mexico for the benefit of the trust or's children. It provides a comprehensive framework for managing and distributing the trust's assets while allowing flexibility for the trustee to make discretionary distributions of both income and principal based on the best interests and needs of the beneficiaries. This trust agreement safeguards the trust assets and ensures that they are utilized solely for the long-term benefit of the children. By designating the trust as irrevocable, the trust or relinquishes control and ownership over the assets, offering protection against potential creditors, divorce settlements, or estate taxes. Utilizing discretionary distributions of income and principal gives the trustee the authority to make decisions regarding the disbursement of funds. This allows the trustee to consider various factors, including the individual needs of the beneficiaries, educational expenses, medical bills, and other extraordinary circumstances. By maintaining discretion, the trustee can adapt to changing circumstances and ensure the trust's assets are utilized in the most beneficial manner. Different types of New Mexico Irrevocable Trust Agreements for the Benefit of Trust or's Children with Discretionary Distributions of Income and Principal may include: 1. Revolving Discretionary Trust: This type of trust allows the trustee to determine the amount and frequency of discretionary distributions, ensuring flexibility in meeting the beneficiaries' changing needs over time. 2. Education Trust: Specifically designed to provide for the educational expenses of the children, this trust focuses on funding tuition, books, supplies, and other educational needs. The trustee retains discretion to adjust distributions as necessary. 3. Special Needs Trust: A trust arrangement to benefit children with special needs, this type of irrevocable trust ensures that the beneficiaries receive necessary support while preserving their eligibility for government benefits. 4. Supplemental Needs Trust: Similar to a special needs trust, this type of trust allows additional discretionary distributions to enhance the beneficiaries' quality of life without affecting their eligibility for means-tested government programs. 5. Health and Wellness Trust: Focused primarily on covering health insurance premiums, medical expenses, preventive care, and other health-related needs to promote the well-being of the children. Creating a New Mexico Irrevocable Trust Agreement for the Benefit of Trust or's Children with Discretionary Distributions of Income and Principal can provide peace of mind for the trust or, knowing that their children's financial needs will be met with the utmost care and consideration. Consultation with a qualified attorney familiar with New Mexico trust laws is essential to ensure the specific goals, requirements, and intentions of the trust or are appropriately addressed.