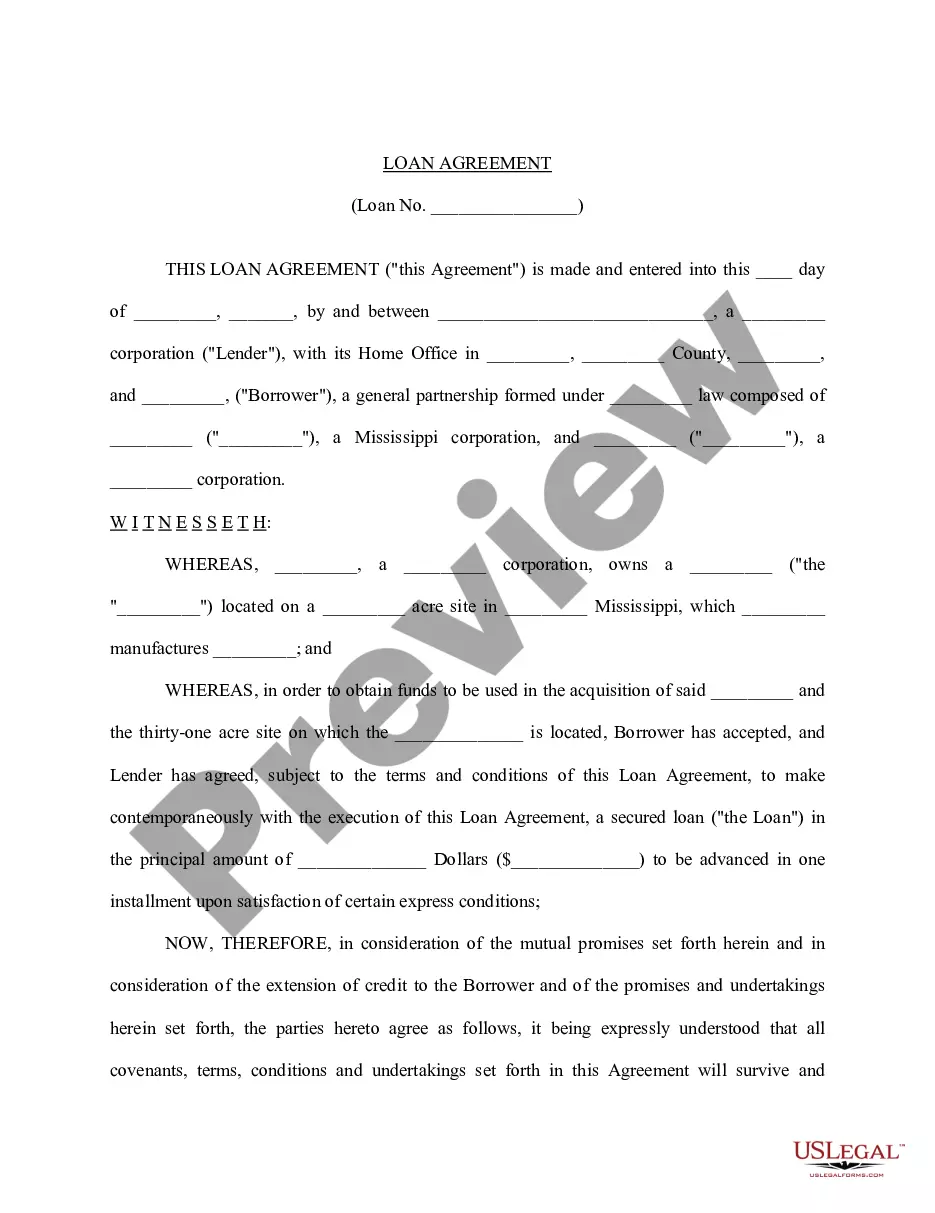

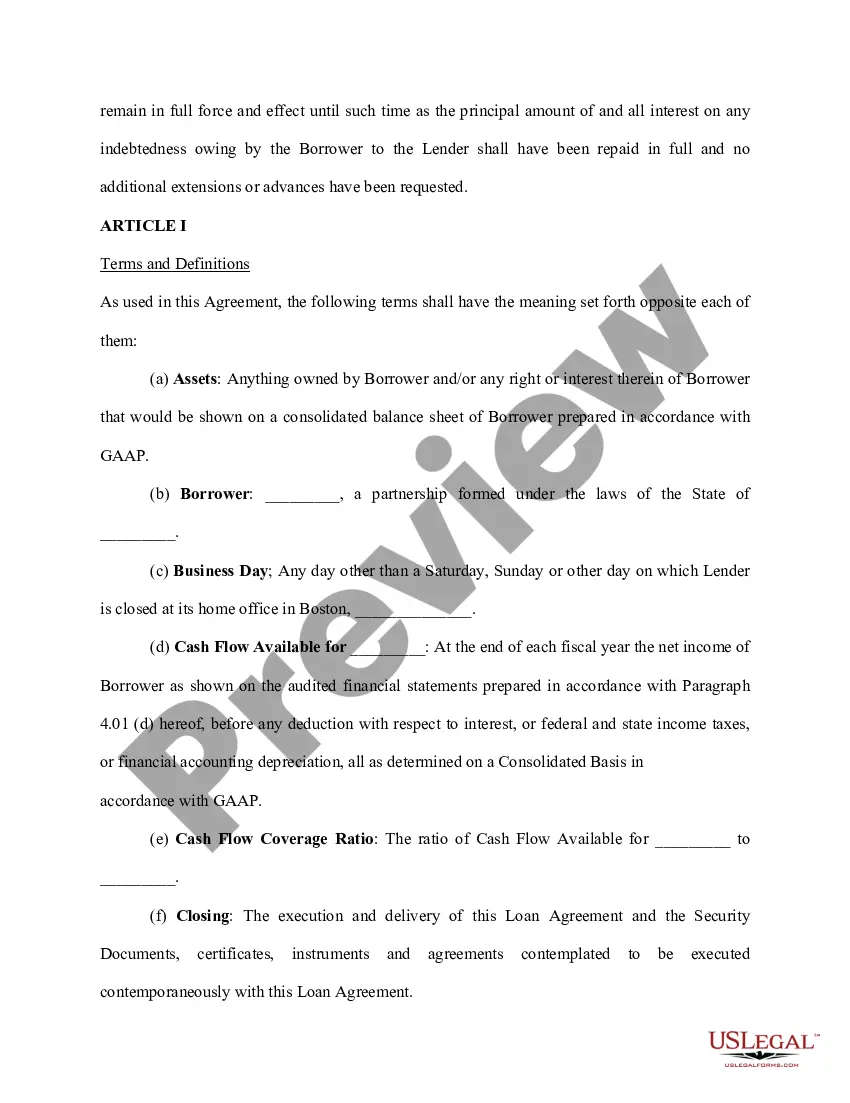

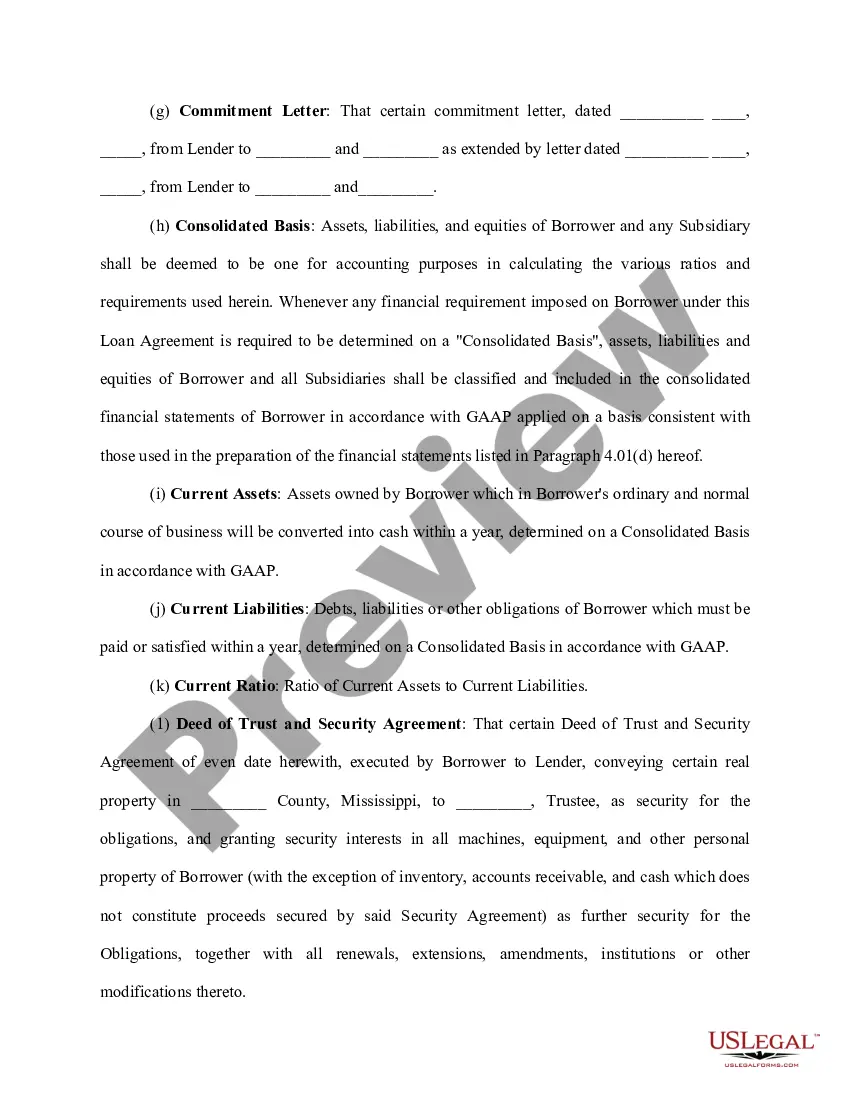

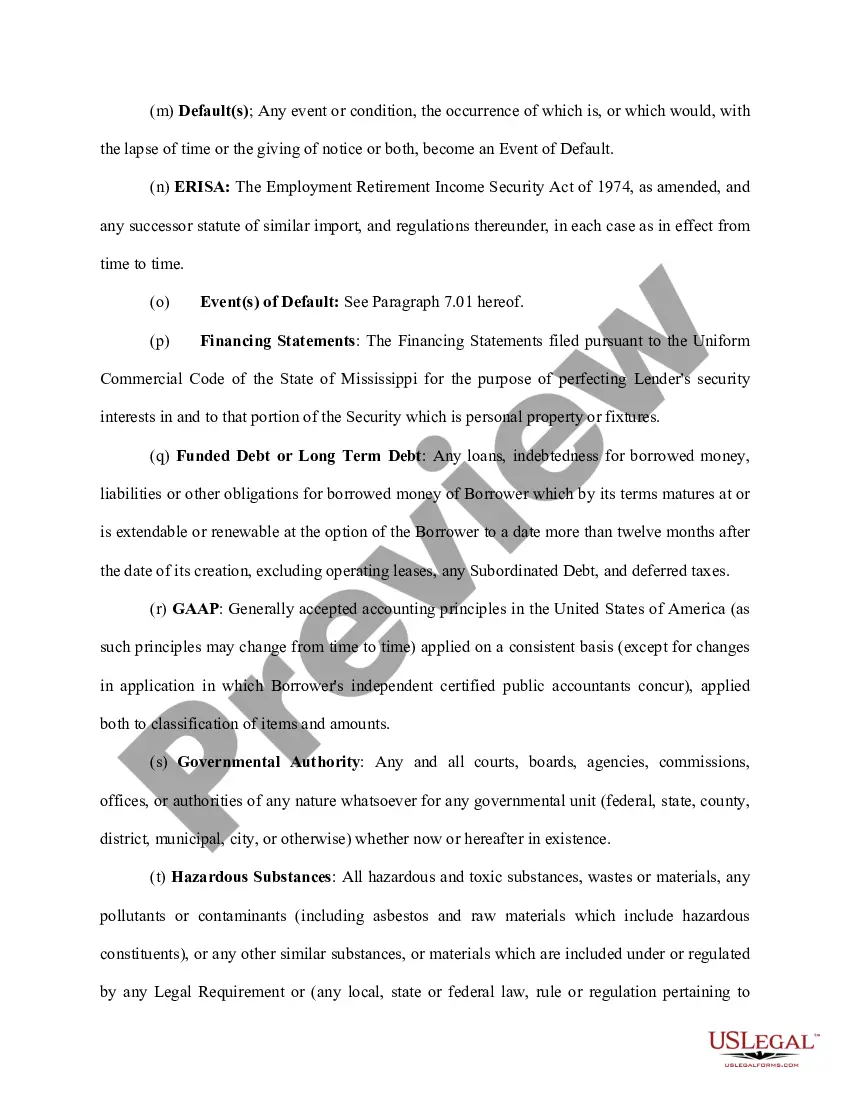

A New Mexico Loan Agreement for Family Member is a legally binding contract that outlines the terms and conditions of a loan between family members in the state of New Mexico. It ensures that both parties are protected and have a clear understanding of their financial obligations. This type of loan agreement is commonly used to provide financial assistance within families or close relatives, while establishing trust and maintaining transparency. Keywords: New Mexico, Loan Agreement, Family Member, legally binding, terms and conditions, financial obligations, financial assistance, trust, transparency. There are various types of Loan Agreements for Family Members that may exist in New Mexico, including: 1. Personal Loan Agreement: This agreement outlines a loan between family members that is meant for personal use, such as paying off debts, funding education, or covering medical expenses. It lays out details like the loan amount, repayment terms, interest (if any), and consequences for defaulting on the loan. 2. Down Payment Loan Agreement: This type of loan agreement is commonly used to help a family member finance the down payment for a home or other property. It specifies the loan amount, repayment terms, and any interest or ownership rights associated with the loan. 3. Business Loan Agreement: If a family member is starting or expanding a business, this agreement can be utilized to formalize a loan. It typically includes details like the loan purpose, loan amount, repayment terms, interest rate (if applicable), and how the loan will be used to support the business. 4. Emergency Loan Agreement: In situations where a family member is facing an unexpected financial crisis, an emergency loan agreement can be established to provide immediate financial assistance. It typically outlines the loan amount, repayment terms, and any interest or collateral involved. 5. Education Loan Agreement: This type of loan agreement focuses on financing educational expenses for a family member, such as tuition fees, textbooks, or living expenses. It specifies the loan amount, repayment terms, and any interest or conditions associated with the loan. Regardless of the specific type, a New Mexico Loan Agreement for Family Member should always include essential elements like the names and contact information of both parties, the loan amount, repayment terms, interest rate (if applicable), and any collateral or guarantees involved. Note: It is important to consult with a legal professional or attorney when drafting or entering into a loan agreement to ensure compliance with state laws and to address any specific requirements or concerns.

New Mexico Loan Agreement for Family Member

Description

How to fill out New Mexico Loan Agreement For Family Member?

US Legal Forms - one of many largest libraries of lawful kinds in America - offers a wide array of lawful record web templates you are able to download or print out. While using internet site, you may get a huge number of kinds for enterprise and person purposes, sorted by classes, says, or keywords.You will discover the most up-to-date variations of kinds much like the New Mexico Loan Agreement for Family Member in seconds.

If you already have a subscription, log in and download New Mexico Loan Agreement for Family Member in the US Legal Forms collection. The Down load key can look on every type you view. You have accessibility to all formerly saved kinds within the My Forms tab of your accounts.

If you wish to use US Legal Forms for the first time, allow me to share simple instructions to obtain started out:

- Be sure you have chosen the correct type for your personal area/county. Click on the Preview key to review the form`s content. Read the type outline to ensure that you have selected the right type.

- If the type doesn`t fit your demands, take advantage of the Search area on top of the monitor to obtain the one that does.

- When you are satisfied with the shape, affirm your selection by clicking on the Acquire now key. Then, opt for the pricing plan you like and supply your accreditations to register for an accounts.

- Process the financial transaction. Use your bank card or PayPal accounts to accomplish the financial transaction.

- Find the format and download the shape in your system.

- Make modifications. Complete, modify and print out and indicator the saved New Mexico Loan Agreement for Family Member.

Each and every web template you put into your money lacks an expiration particular date and is yours for a long time. So, if you wish to download or print out one more backup, just check out the My Forms segment and click on in the type you require.

Obtain access to the New Mexico Loan Agreement for Family Member with US Legal Forms, by far the most comprehensive collection of lawful record web templates. Use a huge number of expert and express-distinct web templates that fulfill your company or person requires and demands.

Form popularity

FAQ

How to make a family loan agreement The amount borrowed and how it will be used. Repayment terms, including payment amounts, frequency and when the loan will be repaid in full. The loan's interest rate. ... If the loan can be repaid early without penalty, and how much interest will be saved by early repayment.

What should be in a personal loan contract? Names and addresses of the lender and the borrower. Information about the loan co-borrower or cosigner, if it's a joint personal loan. Loan amount and the method for disbursement (lump sum, installments, etc.) Date the loan was provided. Expected repayment date.

The IRS mandates that any loan between family members be made with a signed written agreement, a fixed repayment schedule, and a minimum interest rate. (The IRS publishes Applicable Federal Rates (AFRs) monthly.)

Once executed a loan agreement will be legally binding and in effect.

If you loan a significant amount of money to your kids ? over $10,000 ? you should consider charging interest. If you don't, the IRS can say the interest you should have charged was a gift. In that case, the interest money goes toward your annual gift-giving limit of $17,000 per individual (as of tax year 2023).

The IRS mandates that any loan between family members be made with a signed written agreement, a fixed repayment schedule, and a minimum interest rate. (The IRS publishes Applicable Federal Rates (AFRs) monthly.)

You can take a tax deduction for a nonbusiness bad debt if: The money you gave your nephew was intended as a loan, not a gift. You must have actually loaned cash to your nephew. The entire debt is uncollectible.