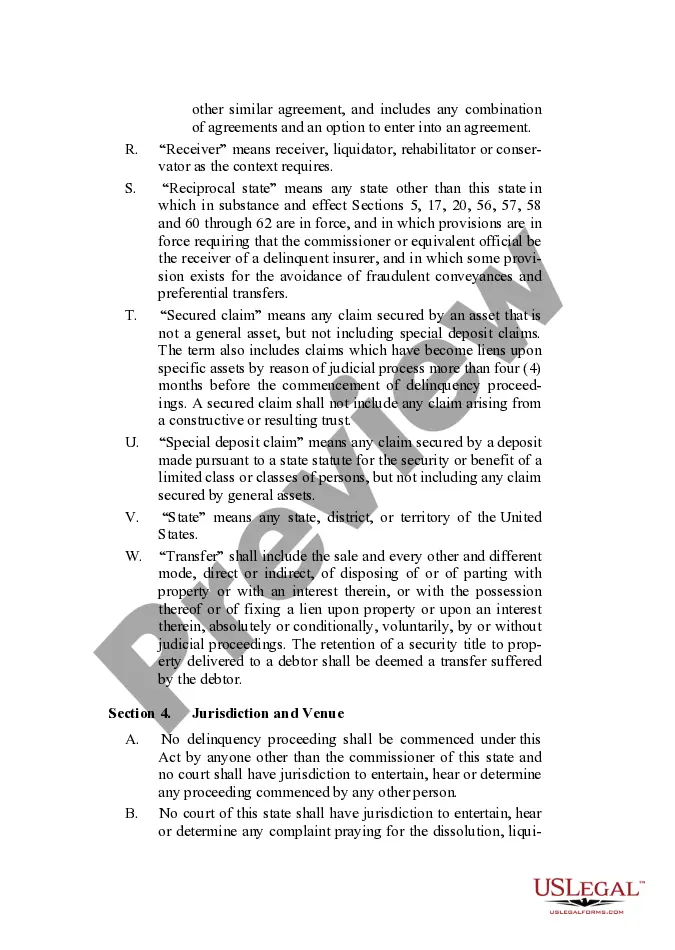

Full text and statutory guidelines for the Insurers Rehabilitation and Liquidation Model Act.

The New Mexico Insurers Rehabilitation and Liquidation Model Act is an essential piece of legislation that governs the rehabilitation and liquidation processes for insurance companies operating within the state. This act outlines the procedures to be followed when insolvent insurance companies are placed under rehabilitation or liquidation, aiming to protect policyholders and safeguard the stability of the insurance industry. The New Mexico Insurers Rehabilitation and Liquidation Model Act consists of several important provisions: 1. Rehabilitation Process: The act provides detailed guidelines for the rehabilitation of insolvent insurance companies. Rehabilitation is a process wherein the company's operations are restructured to overcome financial difficulties and restore solvency. Various steps are outlined, including the appointment of a rehabilitation receiver, the formulation of a rehabilitation plan, and the implementation of necessary measures to improve the insurer's financial condition. 2. Liquidation Process: When rehabilitation efforts fail, the act regulates the liquidation of an insolvent insurance company. Liquidation involves winding up the affairs of the insurer, selling its assets, and distributing the proceeds to policyholders and other claimants. The act defines the powers and duties of the liquidator, who is responsible for overseeing the liquidation process in an orderly manner. 3. Protection of Policyholders: One of the primary objectives of the act is to protect policyholders' interests. It establishes a mechanism to identify and pay policyholder claims promptly and efficiently. The act ensures that policyholders' claims are given priority over other creditors during the rehabilitation or liquidation process. 4. Guaranty Association: The act recognizes the role of the New Mexico Life and Health Insurance Guaranty Association and the New Mexico Property and Casualty Insurance Guaranty Association. These associations provide a safety net for policyholders by guaranteeing the payment of certain policy claims in instances of an insurer's insolvency. The act establishes the responsibilities and obligations of these associations in relation to rehabilitation and liquidation proceedings. 5. Judicial Oversight: The New Mexico Insurers Rehabilitation and Liquidation Model Act emphasizes the importance of judicial oversight throughout the rehabilitation and liquidation processes. It outlines the procedures for initiating rehabilitation or liquidation proceedings, including the submission of petitions to the court, notice requirements, and the appointment and supervision of receivers or liquidators. There aren't different types of the New Mexico Insurers Rehabilitation and Liquidation Model Act, but various states may adopt similar acts with slight variations. However, the core principles of protecting policyholders, ensuring efficient rehabilitation and liquidation processes, and providing legal frameworks for the involvement of guaranty associations and judicial oversight remain consistent across these acts.The New Mexico Insurers Rehabilitation and Liquidation Model Act is an essential piece of legislation that governs the rehabilitation and liquidation processes for insurance companies operating within the state. This act outlines the procedures to be followed when insolvent insurance companies are placed under rehabilitation or liquidation, aiming to protect policyholders and safeguard the stability of the insurance industry. The New Mexico Insurers Rehabilitation and Liquidation Model Act consists of several important provisions: 1. Rehabilitation Process: The act provides detailed guidelines for the rehabilitation of insolvent insurance companies. Rehabilitation is a process wherein the company's operations are restructured to overcome financial difficulties and restore solvency. Various steps are outlined, including the appointment of a rehabilitation receiver, the formulation of a rehabilitation plan, and the implementation of necessary measures to improve the insurer's financial condition. 2. Liquidation Process: When rehabilitation efforts fail, the act regulates the liquidation of an insolvent insurance company. Liquidation involves winding up the affairs of the insurer, selling its assets, and distributing the proceeds to policyholders and other claimants. The act defines the powers and duties of the liquidator, who is responsible for overseeing the liquidation process in an orderly manner. 3. Protection of Policyholders: One of the primary objectives of the act is to protect policyholders' interests. It establishes a mechanism to identify and pay policyholder claims promptly and efficiently. The act ensures that policyholders' claims are given priority over other creditors during the rehabilitation or liquidation process. 4. Guaranty Association: The act recognizes the role of the New Mexico Life and Health Insurance Guaranty Association and the New Mexico Property and Casualty Insurance Guaranty Association. These associations provide a safety net for policyholders by guaranteeing the payment of certain policy claims in instances of an insurer's insolvency. The act establishes the responsibilities and obligations of these associations in relation to rehabilitation and liquidation proceedings. 5. Judicial Oversight: The New Mexico Insurers Rehabilitation and Liquidation Model Act emphasizes the importance of judicial oversight throughout the rehabilitation and liquidation processes. It outlines the procedures for initiating rehabilitation or liquidation proceedings, including the submission of petitions to the court, notice requirements, and the appointment and supervision of receivers or liquidators. There aren't different types of the New Mexico Insurers Rehabilitation and Liquidation Model Act, but various states may adopt similar acts with slight variations. However, the core principles of protecting policyholders, ensuring efficient rehabilitation and liquidation processes, and providing legal frameworks for the involvement of guaranty associations and judicial oversight remain consistent across these acts.