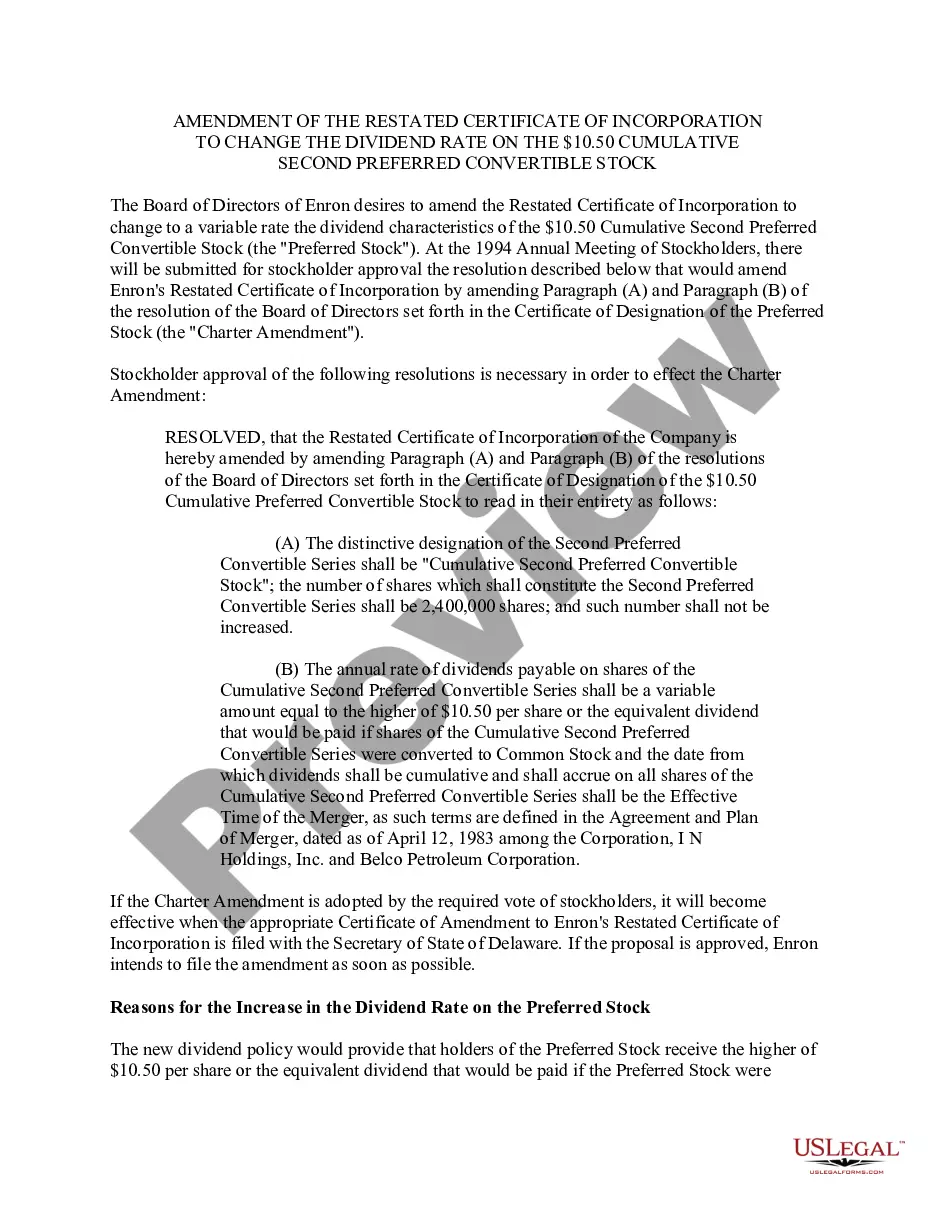

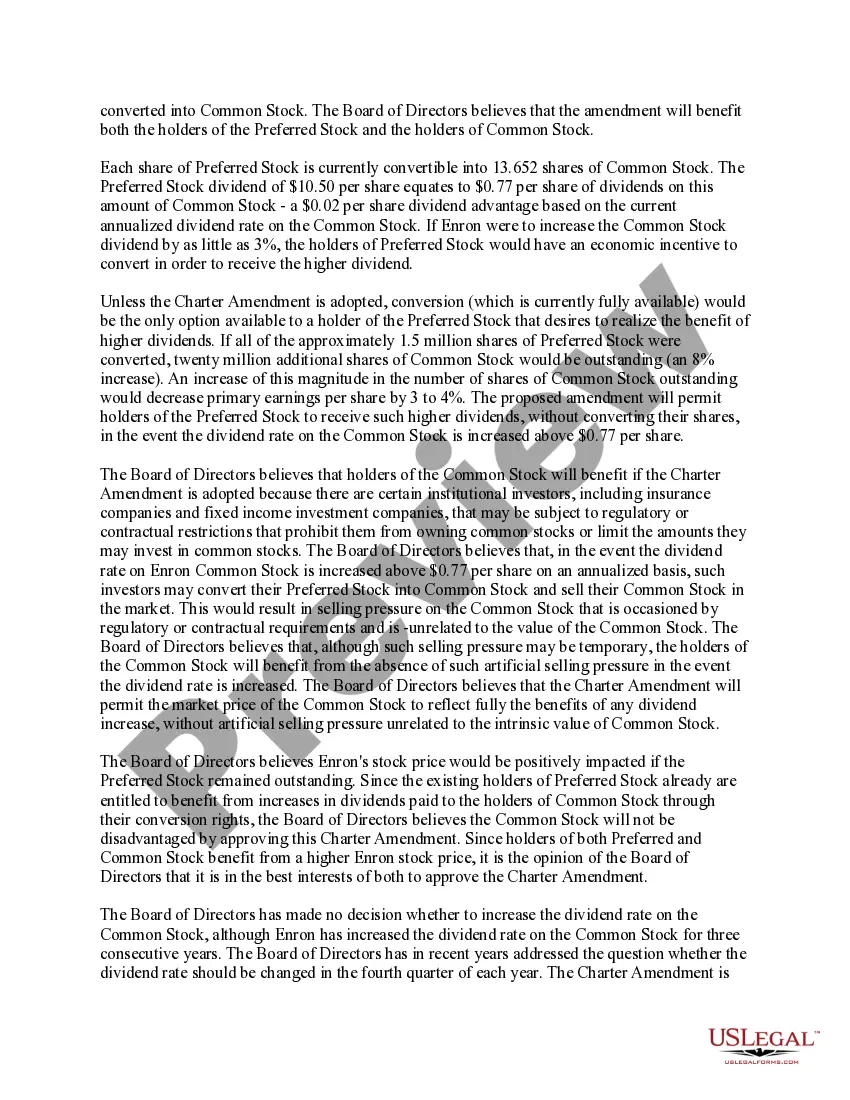

New Mexico Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock is a legal action taken by a corporation incorporated in New Mexico to modify the dividend rate associated with their $10.50 cumulative second preferred convertible stock. Keywords: New Mexico, Amendment, Restated Certificate of Incorporation, change, dividend rate, $10.50 cumulative second preferred convertible stock. This type of amendment allows the corporation to adjust the rate at which dividends are payable to shareholders holding the $10.50 cumulative second preferred convertible stock. By modifying the dividend rate, the corporation seeks to better align the returns provided to these specific shareholders in relation to the performance and profitability of the company. Different Types of New Mexico Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock: 1. Increase in Dividend Rate: This type of amendment seeks to raise the dividend rate on the $10.50 cumulative second preferred convertible stock. The corporation may choose to increase the rate due to improved financial performance, higher profitability, or as a means to attract investors seeking higher returns. 2. Decrease in Dividend Rate: In some cases, a corporation may decide to decrease the dividend rate on the $10.50 cumulative second preferred convertible stock. This action may be taken to conserve capital, reinvest funds into the business, or adapt to changing market conditions. 3. Fixed Dividend Rate: Another type of amendment could establish a fixed dividend rate on the $10.50 cumulative second preferred convertible stock. This fixed rate would remain unchanged regardless of the company's financial performance or dividends on other classes of stock. 4. Floating/Variable Dividend Rate: A floating or variable dividend rate amendment would enable the corporation to adjust the dividend rate on the $10.50 cumulative second preferred convertible stock periodically. This type of amendment often contains provisions that link the dividend rate to specific financial metrics, ensuring shareholders receive a fair return based on the company's performance. 5. Dividend Rate Elimination: In rare instances, a corporation may propose an amendment that eliminates the dividend rate altogether on the $10.50 cumulative second preferred convertible stock. This may occur if the company is experiencing significant financial difficulties, wants to reallocate capital for business expansion, or if the original terms of the stock agreement allowed for such elimination. In summary, the New Mexico Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock provides flexibility for corporations to adjust the dividend rate associated with this specific class of stock. These amendments can further enhance shareholder value, align dividends with financial performance, and adapt to changing market conditions.

New Mexico Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock

Description

How to fill out New Mexico Amendment Of Restated Certificate Of Incorporation To Change Dividend Rate On $10.50 Cumulative Second Preferred Convertible Stock?

Choosing the best legal document format might be a battle. Needless to say, there are a variety of layouts available online, but how do you discover the legal kind you want? Use the US Legal Forms site. The support gives thousands of layouts, including the New Mexico Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock, which can be used for organization and private requirements. All of the forms are checked by experts and satisfy federal and state requirements.

In case you are already listed, log in in your bank account and click the Acquire key to obtain the New Mexico Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock. Use your bank account to search with the legal forms you possess ordered formerly. Go to the My Forms tab of your bank account and get yet another duplicate in the document you want.

In case you are a whole new end user of US Legal Forms, allow me to share straightforward recommendations so that you can adhere to:

- First, ensure you have selected the appropriate kind for the town/county. You are able to look over the shape making use of the Preview key and read the shape outline to ensure this is the best for you.

- When the kind is not going to satisfy your requirements, take advantage of the Seach industry to discover the correct kind.

- When you are positive that the shape is proper, go through the Acquire now key to obtain the kind.

- Pick the costs prepare you want and type in the required info. Create your bank account and pay for the transaction using your PayPal bank account or credit card.

- Pick the data file file format and download the legal document format in your device.

- Complete, edit and print out and sign the acquired New Mexico Amendment of Restated Certificate of Incorporation to change dividend rate on $10.50 cumulative second preferred convertible stock.

US Legal Forms will be the biggest collection of legal forms for which you will find numerous document layouts. Use the service to download professionally-made paperwork that adhere to state requirements.