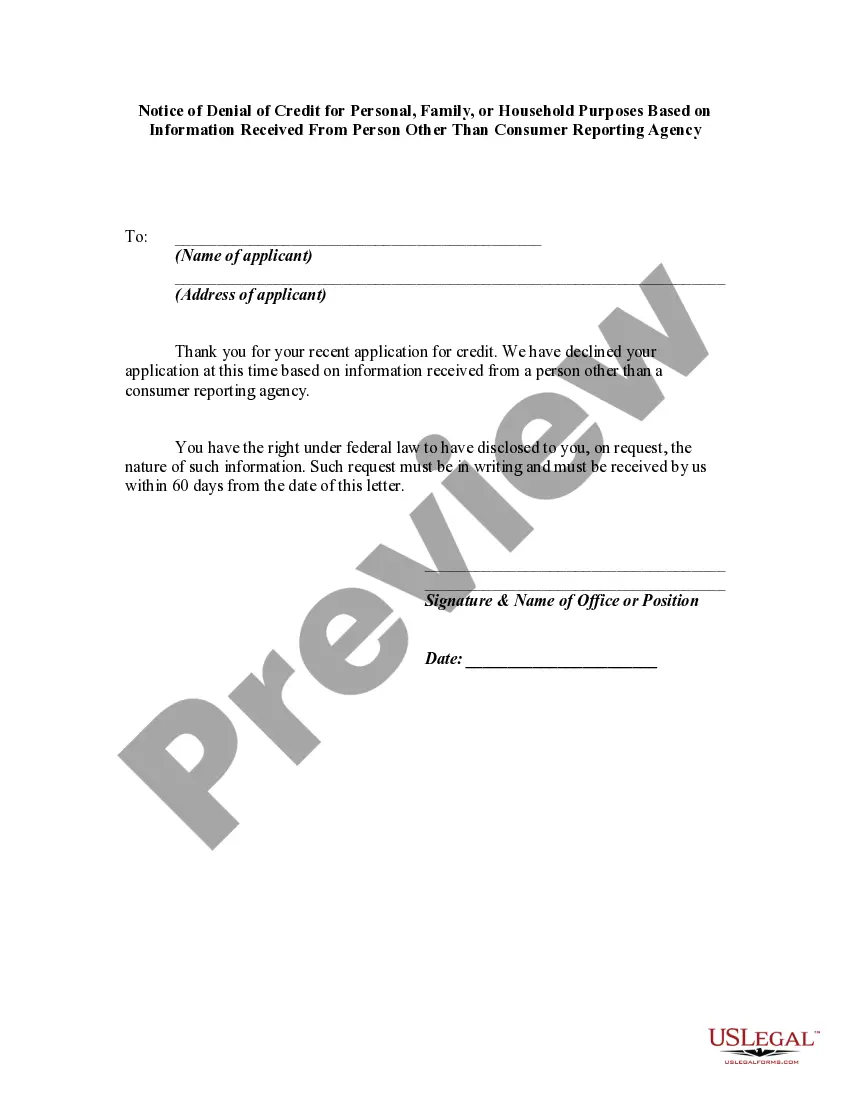

Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information.

Title: Understanding the Nevada Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency Introduction: The Nevada Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency is an essential document that consumers should be aware of. It outlines the legal requirements and procedures that financial institutions must adhere to when denying credit applications based on information obtained from a source other than a consumer reporting agency. This article aims to provide a detailed description of this notice and its various types. Types of Nevada Notice of Denial of Credit: 1. General Explanation: The Nevada Notice of Denial of Credit for Personal, Family, or Household Purposes is a broad term covering several specific circumstances. It mainly refers to the situation where an individual's credit application is declined based on information received from a person or entity other than a consumer reporting agency. This notice is designed to ensure transparency and fairness in the lending process, allowing consumers to understand the factors influencing their denial. 2. Specific Denial Reasons: Within the Nevada Notice of Denial of Credit for Personal, Family, or Household Purposes, specific reasons for the denial must be provided. These may include factors such as insufficient income, high debt-to-income ratio, poor credit history, or inadequate collateral. The notice should clearly outline the reason(s) responsible for the denial while avoiding generic statements. 3. Separate Notices for Joint Accounts: In cases where multiple individuals jointly apply for credit, each applicant is entitled to receive a separate Notice of Denial. This ensures that each co-applicant is aware of the reasons behind the denial and can take appropriate action if necessary. 4. Timely Delivery and Content: Nevada law requires that the Notice of Denial be delivered to the consumer no later than 30 days after the credit application's rejection. The notice must contain specific details, including the consumer's name, the reason(s) for denial, the source(s) of information utilized other than a consumer reporting agency, and the consumer's right to obtain a free copy of their credit report within 60 days. 5. Remedies and Consumer Rights: Upon receiving the Nevada Notice of Denial of Credit, consumers have the right to request a copy of their credit report within 60 days. They can review the report, verify its accuracy, and dispute any incorrect or incomplete information. Furthermore, the notice should provide information on how individuals can contact the person or entity that provided the adverse information, allowing them to rectify any potential errors. Conclusion: The Nevada Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency is an essential document that safeguards consumers' rights and ensures fair lending practices. By understanding the different types of notices, individuals can take appropriate actions to resolve any issues and improve their creditworthiness.Title: Understanding the Nevada Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency Introduction: The Nevada Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency is an essential document that consumers should be aware of. It outlines the legal requirements and procedures that financial institutions must adhere to when denying credit applications based on information obtained from a source other than a consumer reporting agency. This article aims to provide a detailed description of this notice and its various types. Types of Nevada Notice of Denial of Credit: 1. General Explanation: The Nevada Notice of Denial of Credit for Personal, Family, or Household Purposes is a broad term covering several specific circumstances. It mainly refers to the situation where an individual's credit application is declined based on information received from a person or entity other than a consumer reporting agency. This notice is designed to ensure transparency and fairness in the lending process, allowing consumers to understand the factors influencing their denial. 2. Specific Denial Reasons: Within the Nevada Notice of Denial of Credit for Personal, Family, or Household Purposes, specific reasons for the denial must be provided. These may include factors such as insufficient income, high debt-to-income ratio, poor credit history, or inadequate collateral. The notice should clearly outline the reason(s) responsible for the denial while avoiding generic statements. 3. Separate Notices for Joint Accounts: In cases where multiple individuals jointly apply for credit, each applicant is entitled to receive a separate Notice of Denial. This ensures that each co-applicant is aware of the reasons behind the denial and can take appropriate action if necessary. 4. Timely Delivery and Content: Nevada law requires that the Notice of Denial be delivered to the consumer no later than 30 days after the credit application's rejection. The notice must contain specific details, including the consumer's name, the reason(s) for denial, the source(s) of information utilized other than a consumer reporting agency, and the consumer's right to obtain a free copy of their credit report within 60 days. 5. Remedies and Consumer Rights: Upon receiving the Nevada Notice of Denial of Credit, consumers have the right to request a copy of their credit report within 60 days. They can review the report, verify its accuracy, and dispute any incorrect or incomplete information. Furthermore, the notice should provide information on how individuals can contact the person or entity that provided the adverse information, allowing them to rectify any potential errors. Conclusion: The Nevada Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency is an essential document that safeguards consumers' rights and ensures fair lending practices. By understanding the different types of notices, individuals can take appropriate actions to resolve any issues and improve their creditworthiness.