A secured transaction is created when a buyer or borrower (debtor) grants a seller or lender (creditor or secured party) a security interest in personal property (collateral). A security interest allows a creditor to repossess and sell the collateral if a debtor fails to pay a secured debt.

The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use or business purposes.

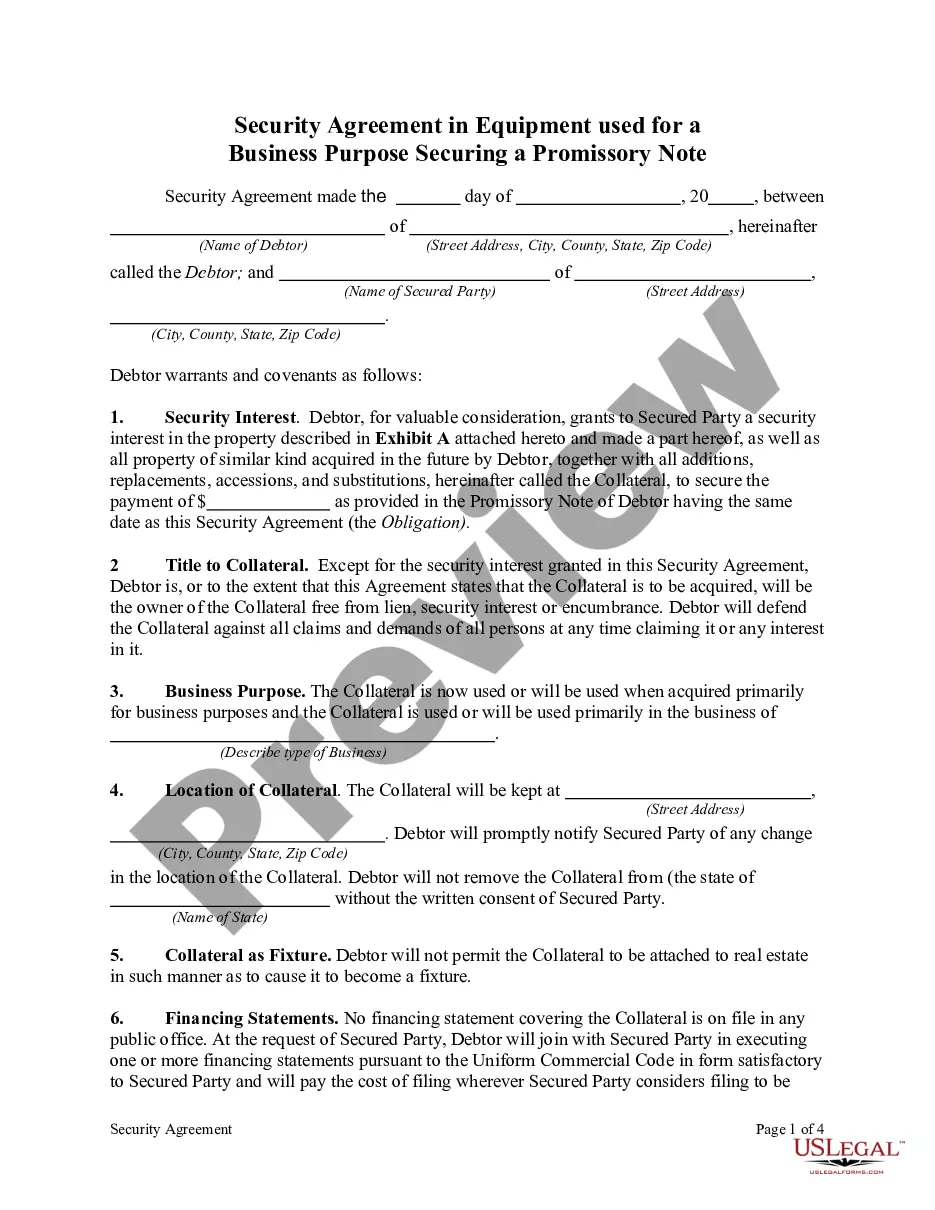

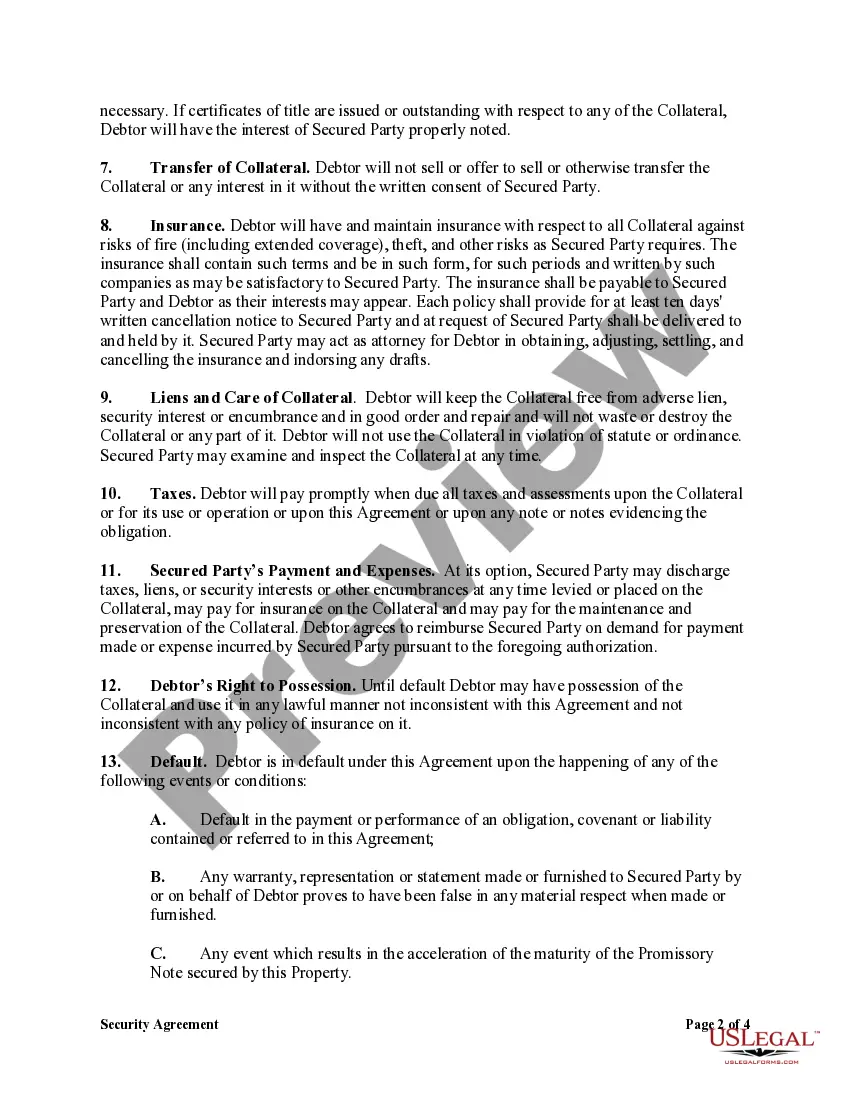

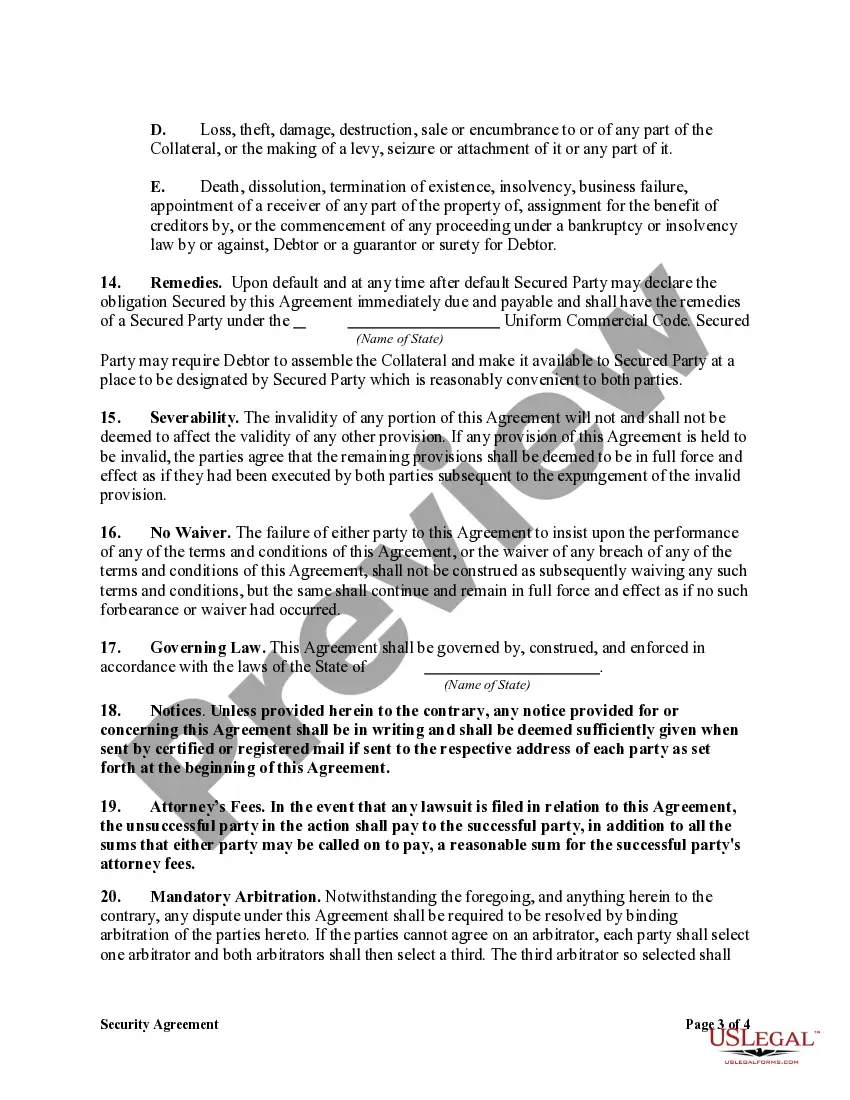

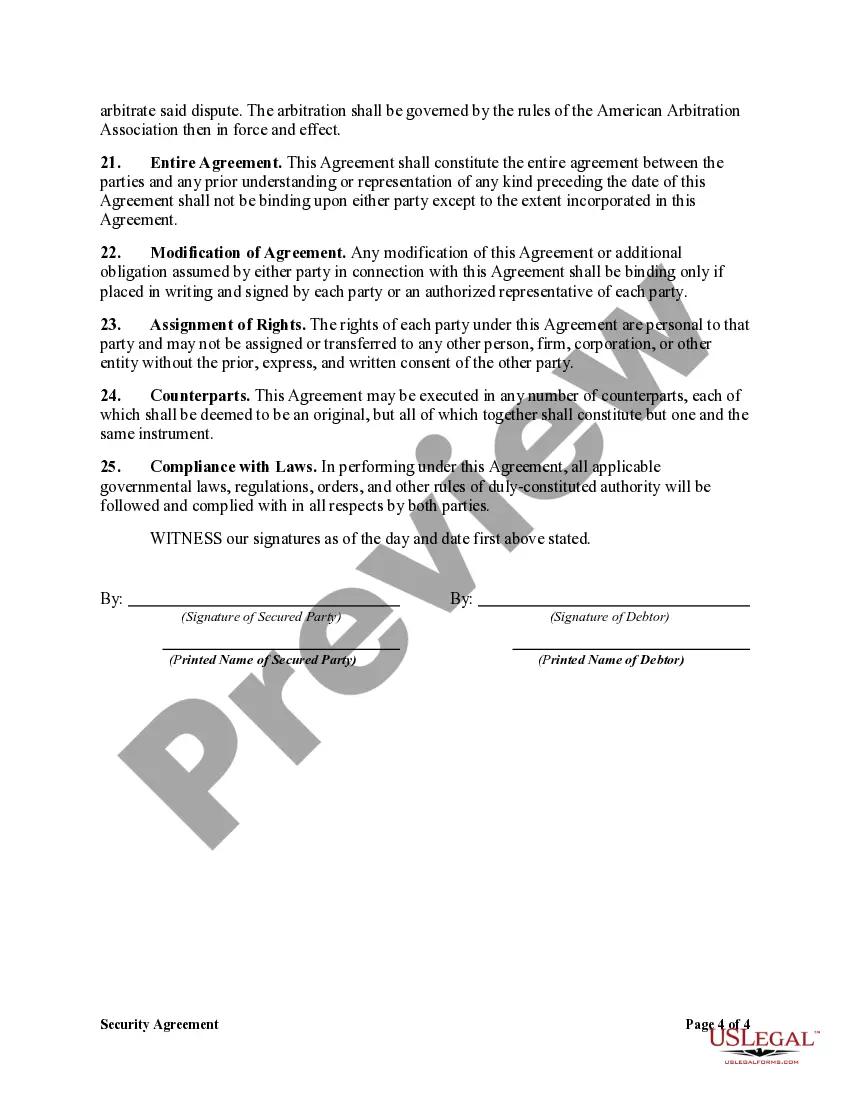

A Nevada Security Agreement in Equipment for Business Purposes is a legal document that outlines the terms and conditions of securing a promissory note using equipment as collateral. This agreement is commonly used when financing equipment purchases for a business, giving the lender the right to repossess and sell the equipment if the borrower fails to repay the loan according to the agreed-upon terms. The Nevada Security Agreement in Equipment for Business Purposes is crucial for both the borrower and the lender, as it protects the interests of each party involved. By securing the promissory note with equipment, the lender has some assurance that they can recoup their investment in case of default. In Nevada, there are two main types of Security Agreements in Equipment for Business Purposes — Securing Promissory Note: 1. Specific Equipment Security Agreement: This type of agreement lists specific equipment that acts as collateral for the promissory note. The equipment is identified with detailed descriptions, such as make, model, serial numbers, and any other relevant identification information. This type of agreement ensures that the lender has a direct claim over the specified equipment in case of default. 2. Blanket Equipment Security Agreement: Unlike specific equipment security agreements, a blanket equipment security agreement covers a broader range of equipment owned by the borrower. Instead of individually listing each item, this agreement includes a detailed and comprehensive description of the equipment class or type. This type of agreement allows the borrower to use any equipment included within the defined class as collateral for the promissory note. It provides flexibility in securing loans while covering a range of equipment assets. It is essential for both parties to review and understand the terms and provisions of a Nevada Security Agreement in Equipment for Business Purposes before signing. Clear and precise language should be used to address matters such as default, repossession rights, insurance requirements, maintenance obligations, and dispute resolution mechanisms. By using a Nevada Security Agreement in Equipment for Business Purposes — Securing Promissory Note, businesses can obtain financing to acquire essential equipment while lenders can protect their investment and have recourse in case of default. Consulting with a legal professional is highly recommended ensuring compliance with Nevada state laws and to tailor the agreement to specific business needs.A Nevada Security Agreement in Equipment for Business Purposes is a legal document that outlines the terms and conditions of securing a promissory note using equipment as collateral. This agreement is commonly used when financing equipment purchases for a business, giving the lender the right to repossess and sell the equipment if the borrower fails to repay the loan according to the agreed-upon terms. The Nevada Security Agreement in Equipment for Business Purposes is crucial for both the borrower and the lender, as it protects the interests of each party involved. By securing the promissory note with equipment, the lender has some assurance that they can recoup their investment in case of default. In Nevada, there are two main types of Security Agreements in Equipment for Business Purposes — Securing Promissory Note: 1. Specific Equipment Security Agreement: This type of agreement lists specific equipment that acts as collateral for the promissory note. The equipment is identified with detailed descriptions, such as make, model, serial numbers, and any other relevant identification information. This type of agreement ensures that the lender has a direct claim over the specified equipment in case of default. 2. Blanket Equipment Security Agreement: Unlike specific equipment security agreements, a blanket equipment security agreement covers a broader range of equipment owned by the borrower. Instead of individually listing each item, this agreement includes a detailed and comprehensive description of the equipment class or type. This type of agreement allows the borrower to use any equipment included within the defined class as collateral for the promissory note. It provides flexibility in securing loans while covering a range of equipment assets. It is essential for both parties to review and understand the terms and provisions of a Nevada Security Agreement in Equipment for Business Purposes before signing. Clear and precise language should be used to address matters such as default, repossession rights, insurance requirements, maintenance obligations, and dispute resolution mechanisms. By using a Nevada Security Agreement in Equipment for Business Purposes — Securing Promissory Note, businesses can obtain financing to acquire essential equipment while lenders can protect their investment and have recourse in case of default. Consulting with a legal professional is highly recommended ensuring compliance with Nevada state laws and to tailor the agreement to specific business needs.