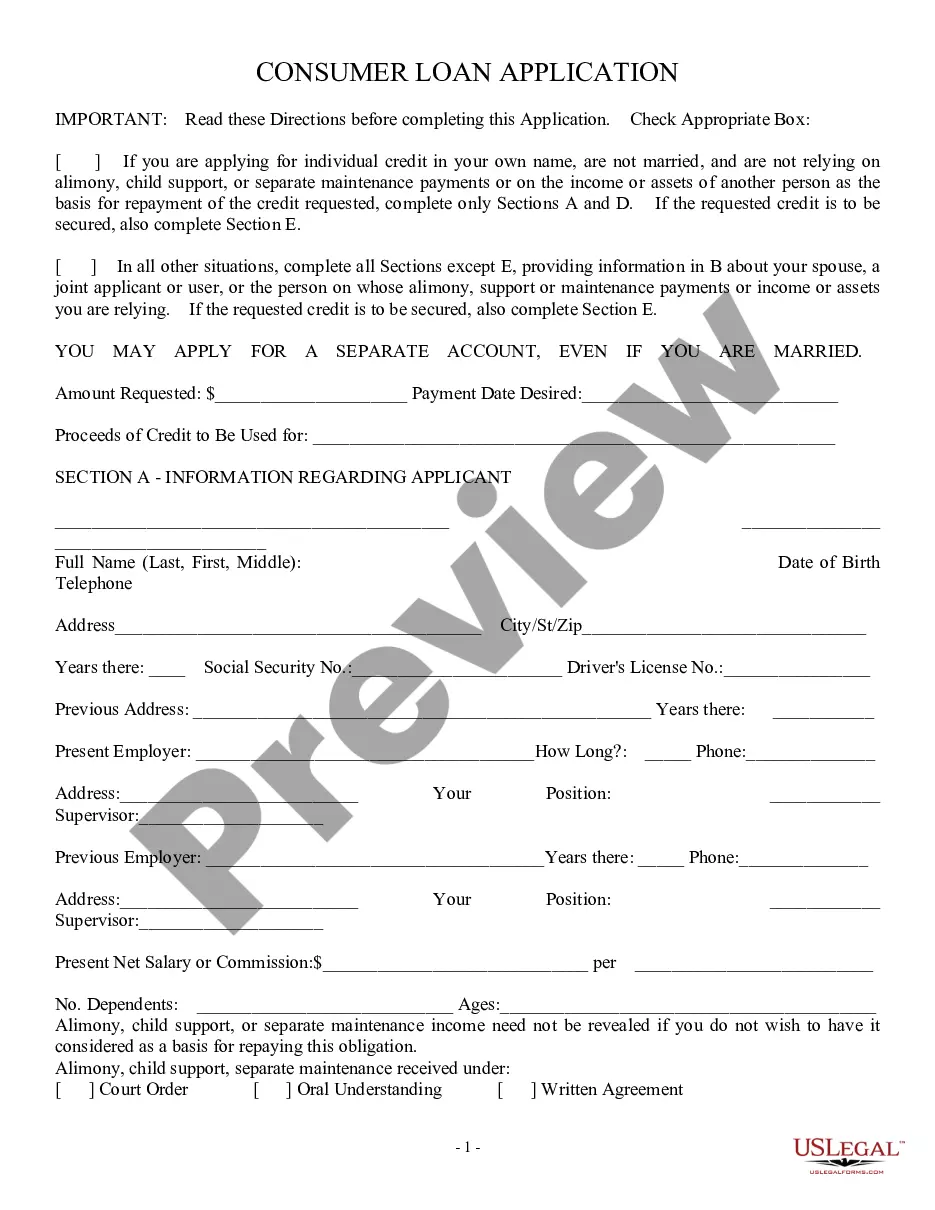

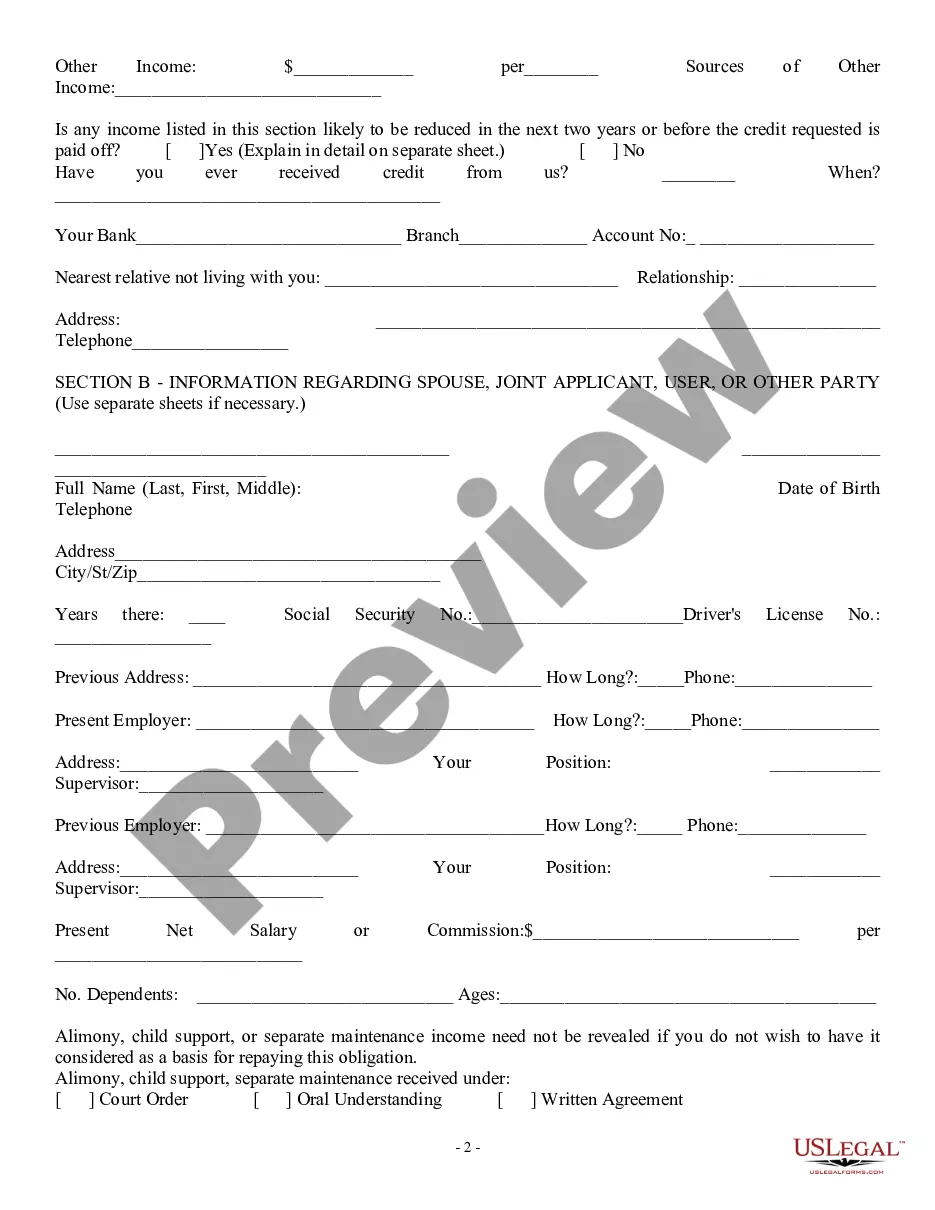

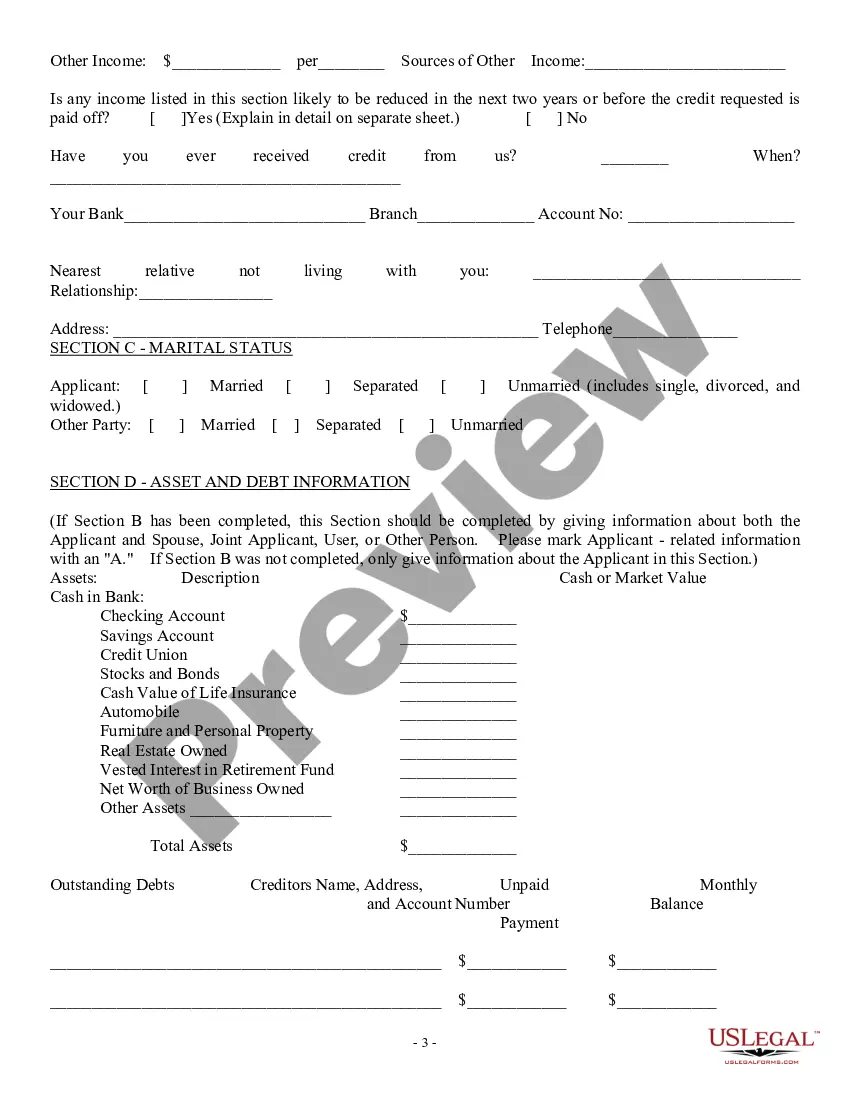

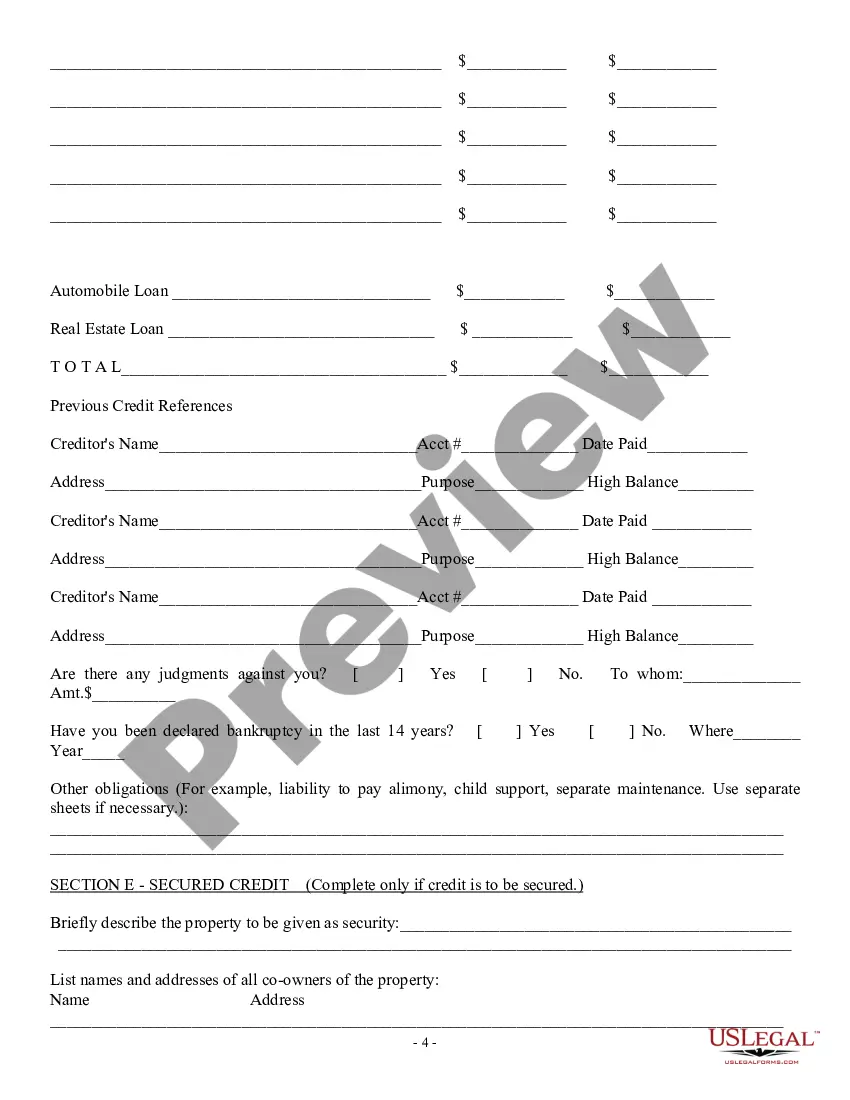

The Nevada Consumer Loan Application — Personal Loan Agreement is a legally binding document that outlines the terms and conditions between a lender and a borrower for a personal loan in the state of Nevada. This agreement is used by individuals seeking financial assistance for various purposes such as debt consolidation, home improvements, medical expenses, or educational needs. When applying for a personal loan in Nevada, it is important to have a thorough understanding of the loan agreement as it governs the borrower's responsibilities and the lender's obligations. The agreement typically includes the following key details: 1. Loan Amount: The agreement specifies the amount of money being borrowed by the borrower and the repayment terms associated with it. 2. Interest Rate: The interest rate is the cost of borrowing the funds and represents the percentage of the loan amount that the borrower will pay as interest over the loan term. 3. Payment Schedule: This section outlines the repayment schedule including the frequency of payments (such as monthly or bi-weekly), the due dates, and the total number of payments required. 4. Late Payment Fees: The agreement may include details about late payment penalties or fees that the borrower will incur if they fail to make timely repayments. 5. Prepayment or Early Repayment Options: Some loan agreements allow borrowers to make early repayments without incurring additional charges. This section provides clarity on whether such options are available and any associated fees. 6. Collateral: Depending on the loan type, borrowers may be required to provide collateral to secure the loan. This can be in the form of personal property or real estate. The agreement will outline the details of the collateral and the consequences of non-repayment. Different types of Consumer Loan Applications — Personal Loan Agreements in Nevada may include: 1. Secured Personal Loan Agreement: This type of loan requires the borrower to provide collateral as security for the loan, reducing the lender's risk. Common collateral types include a vehicle, real estate property, or other valuable assets. 2. Unsecured Personal Loan Agreement: Unlike secured loans, unsecured personal loans do not require collateral. This type of loan relies solely on the borrower's creditworthiness and repayment capacity. Lenders typically assess the borrower's credit history and income to determine eligibility and interest rates. 3. Installment Personal Loan Agreement: Installment loans are repaid over a set period in fixed monthly installments. This agreement details the loan amount, interest rate, and the specified repayment term. 4. Payday Loan Agreement: Payday loans are short-term loans typically due on the borrower's next payday. This type of loan generally has higher interest rates and may have different requirements compared to traditional personal loans. It is important for borrowers to thoroughly review and understand the terms and conditions outlined in the Nevada Consumer Loan Application — Personal Loan Agreement before signing, ensuring they are comfortable with the financial obligations and repayment terms. Seeking legal or financial advice is always recommended ensuring complete understanding and protection of one's rights and obligations.

Nevada Consumer Loan Application - Personal Loan Agreement

Description

How to fill out Nevada Consumer Loan Application - Personal Loan Agreement?

Are you currently in the position in which you need to have files for both business or person reasons nearly every day? There are a lot of legal papers web templates available on the Internet, but finding versions you can rely on is not simple. US Legal Forms gives a large number of form web templates, such as the Nevada Consumer Loan Application - Personal Loan Agreement, which can be published to fulfill federal and state requirements.

When you are currently acquainted with US Legal Forms website and get a merchant account, basically log in. Afterward, you may acquire the Nevada Consumer Loan Application - Personal Loan Agreement template.

Unless you come with an accounts and need to begin using US Legal Forms, abide by these steps:

- Discover the form you need and make sure it is for your correct metropolis/state.

- Make use of the Preview button to check the form.

- Look at the outline to actually have chosen the correct form.

- In case the form is not what you`re looking for, make use of the Research area to find the form that suits you and requirements.

- When you obtain the correct form, click Purchase now.

- Pick the costs prepare you need, fill out the specified information and facts to make your account, and pay money for an order with your PayPal or charge card.

- Choose a hassle-free data file format and acquire your duplicate.

Discover all of the papers web templates you might have bought in the My Forms menu. You may get a additional duplicate of Nevada Consumer Loan Application - Personal Loan Agreement any time, if required. Just go through the needed form to acquire or print out the papers template.

Use US Legal Forms, probably the most substantial variety of legal kinds, to save efforts and prevent errors. The assistance gives skillfully produced legal papers web templates that can be used for an array of reasons. Produce a merchant account on US Legal Forms and start producing your daily life easier.