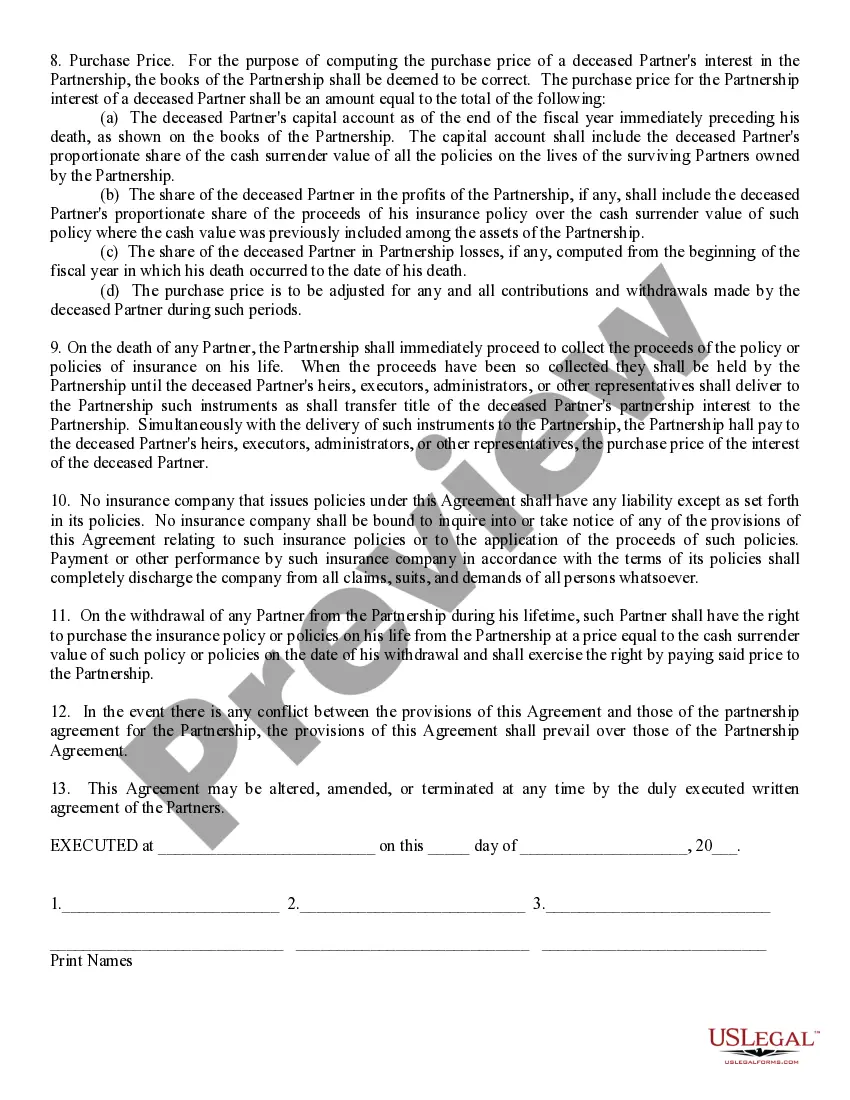

Title: Nevada Sale of Deceased Partner's Interest: Exploring the Process and Types Introduction: The Nevada Sale of Deceased Partner's Interest refers to the legal process of transferring the ownership share of a deceased partner in a partnership or business to a surviving partner or third party. This comprehensive guide aims to provide a detailed description of what this procedure entails in Nevada, along with different types of transfers that can occur. 1. Overview of Nevada Sale of Deceased Partner's Interest: Nevada recognizes the importance of establishing clear guidelines for the sale and transfer of a deceased partner's interest in a business. This process ensures smooth succession and protects the interests of all parties involved. The state's laws provide specific guidelines to govern this procedure. 2. Process of Nevada Sale of Deceased Partner's Interest: a. Determining the deceased partner's interest: The first step involves assessing the overall value and percentage of ownership that the deceased partner held in the partnership or business. This valuation is critical in determining the appropriate price for the share. b. Agreement review: The existing partnership agreement or buy-sell agreement should be reviewed thoroughly, as it may include provisions regarding the sale and transfer of a deceased partner's interest. It is crucial to follow the agreed-upon terms and conditions outlined in these documents. c. Consent of surviving partners: The surviving partners must consent to the sale or transfer of the deceased partner's interest. If they exercise their right of first refusal, they may directly purchase the interest or offer it to third parties. d. Valuation of interest: An independent valuation expert can determine the fair market value of the deceased partner's interest. This assessment ensures a fair price is set for the transaction. e. Negotiating terms: Surviving partners or potential buyers must negotiate the terms and conditions of the sale, including the payment method, transfer of assets, and any associated timelines. f. Closing the transaction: Once both parties agree on the terms, a purchase agreement or contract should be formalized, signed, and executed. This contract acts as legal documentation of the sale and serves to protect the interests of all parties involved. g. Filing with the Secretary of State: In Nevada, the sale or transfer of a deceased partner's interest typically requires the filing of specific documents with the Secretary of State or other applicable state agencies. 3. Types of Nevada Sale of Deceased Partner's Interest: a. Sale to surviving partner(s): If the partnership agreement or buy-sell agreement permits, surviving partner(s) may have the right to purchase the deceased partner's interest directly. The purchase price is commonly determined based on a pre-determined valuation formula or through negotiation. b. Sale to third party(IES): In cases where surviving partner(s) waive their right of first refusal, the deceased partner's interest can be sold to an external buyer or group of buyers. The agreement for such a transaction must comply with the partnership agreement and state laws. c. Proportional redistribution: Another option is the proportional redistribution of the deceased partner's interest among the existing partners, maintaining the original percentage of ownership for each partner. d. Conversion to cash or assets: In some situations, the deceased partner's interest can be liquidated and converted into cash or specific assets equivalent to the valuation amount. Conclusion: Navigating the Nevada Sale of Deceased Partner's Interest entails careful consideration of partnership agreements, valuations, negotiations, and legal requirements. By understanding the process and various types of transfers possible within Nevada, affected parties can ensure a fair and smooth transition of a deceased partner's interest in a partnership or business.

Nevada Sale of Deceased Partner's Interest

Description

How to fill out Nevada Sale Of Deceased Partner's Interest?

Finding the correct sanctioned document template can be rather a challenge.

Of course, there are numerous templates accessible online, but how do you obtain the sanctioned form you require.

Utilize the US Legal Forms website. The service offers thousands of templates, including the Nevada Sale of Deceased Partner's Interest, which can be used for both business and personal purposes.

You can preview the form using the Preview button and review the form details to confirm it is suitable for you.

- All of the documents are reviewed by experts and comply with federal and state regulations.

- If you are already registered, Log In to your account and then click the Download button to obtain the Nevada Sale of Deceased Partner's Interest.

- Use your account to browse through the legal forms you have previously purchased.

- Visit the My documents tab of your account and retrieve another copy of the document you need.

- If you are a new user of US Legal Forms, here are simple steps for you to follow.

- First, ensure that you have selected the correct form for your region/location.

Form popularity

FAQ

A general rule of thumb is the more complicated the estate in question, the longer Grant of Probate will take to obtain. Prepare to wait anywhere between six to 12 weeks if the estate you are dealing with happens to be complex and taxable.

Recording a quitclaim deed in Nevada serves to provide notice to third persons (NRS 111.315). An unrecorded quitclaim deed is valid only between the parties to the conveyance.

The sale must be confirmed by the Probate Court. This means that the sales contract has to be submitted to the Probate Court in advance of the sale. The Personal Representative will also need to provide the Probate Court with an appraisal of the property to be sold.

In Nevada, you can make a living trust to avoid probate for virtually any asset you ownreal estate, bank accounts, vehicles, and so on. You need to create a trust document (it's similar to a will), naming someone to take over as trustee after your death (called a successor trustee).

How Long Do You Have to File Probate After a Death in Nevada? The will must be filed with the court within 30 days of the person's death even if a petition to file probate is not submitted at the same time. There is no deadline or statute of limitations to file probate in Nevada.

In Nevada, if the total amount of the deceased person's assets exceeds $20,000, or if real estate is involved, probate (or administration) will be required and there is normally no reason to delay starting the process.

Generally speaking, if you are unmarried and die intestate in Nevada and have children, your children will inherit your estate in equal shares. If you die with no children but with living parents, your estate will pass on to your parents. If your parents are not alive, the estate then goes to your siblings.

According to Nevada probate law, all estates with a total value of $20,000 or more, as well as any estates with real estate included in their inventory of assets, must go through probate court.

Based upon the author's 20 plus years of experience in probating estates in Nevada, the average summary administration (assuming no matters occur outside the Ordinary Course) takes around 7-8 months. If you have to confirm a sale of a house or other real property, add at a minimum another month.

It usually takes six to eight weeks for probate to come through, although it can take longer in more complex cases.

Interesting Questions

More info

The Wolters Kluwer® brand has been providing quality products, service and support for more than 100 years. Our products include technical support, customizations and training tools, including Interconnect®, Interconnect+®, and Interconnect Plus®.