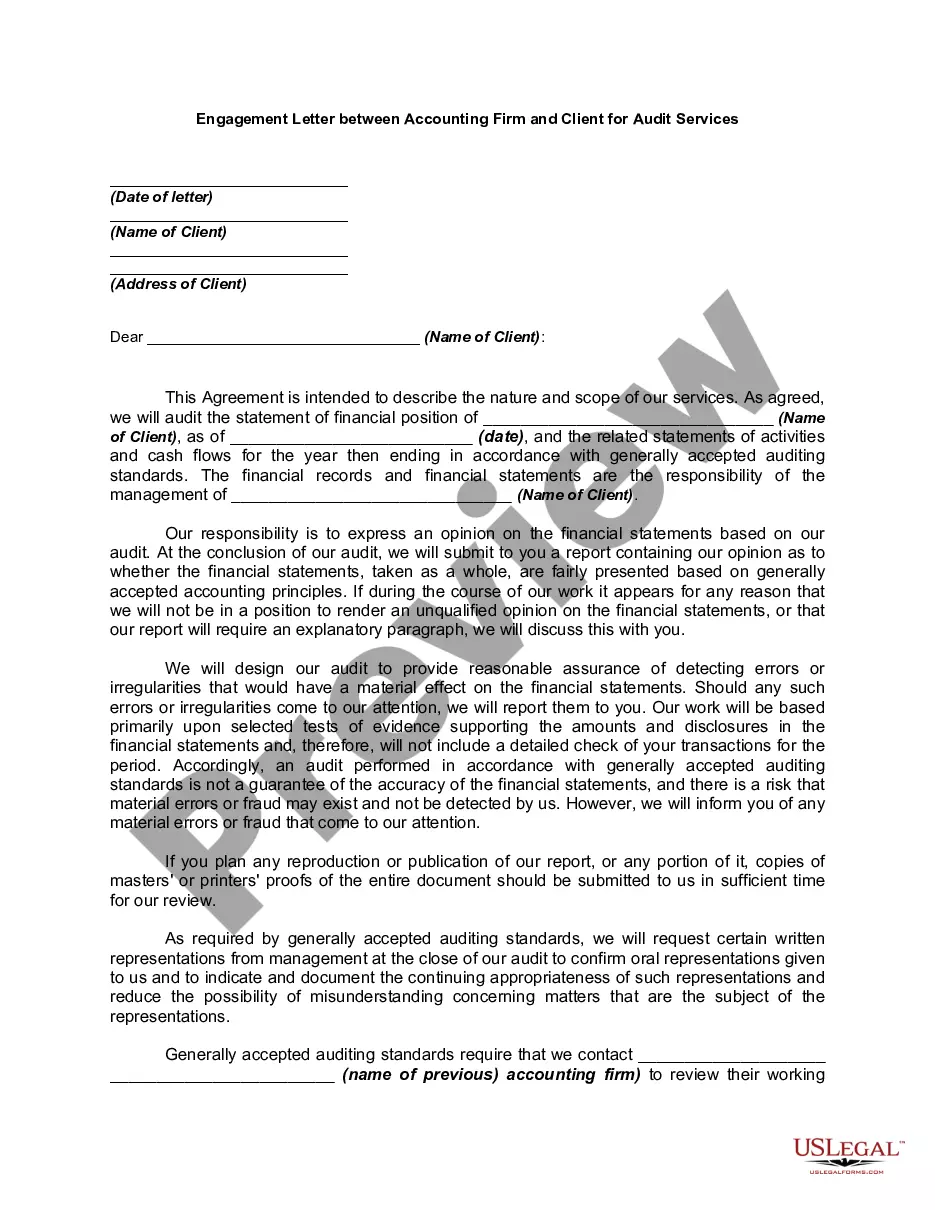

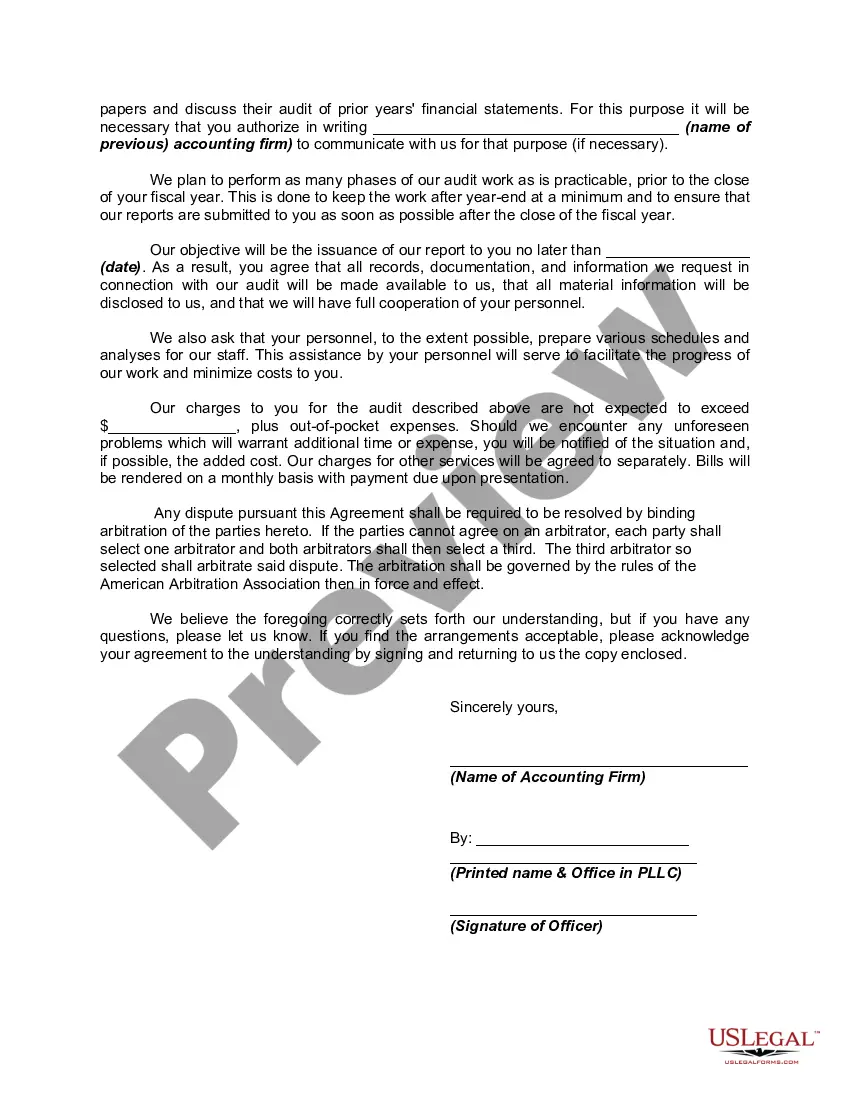

Generally, a contract to employ a certified public accountant need not be in writing.

However, such contracts often call for services of a highly complex and technical nature, and hence they should be explicit in their terms, and they should be in writing. In particular, a written employment contract is necessary in order to avoid misunderstanding with the employer regarding the amount of the accountant's fee or compensation and the nature of its computation. As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books.

This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

The Nevada Engagement Letter between an accounting firm and a client for audit services is a crucial document that outlines the terms and conditions of the engagement. This legal agreement helps establish a clear understanding between the accounting firm and the client regarding the scope of the audit, responsibilities, expectations, and compensation. Key components typically included in a Nevada Engagement Letter for Audit Services are: 1. Parties involved: This clause specifies the names, addresses, and contact information of both the accounting firm and the client. It ensures that the engagement is between the correct parties and helps facilitate effective communication. 2. Purpose and scope of the audit: This section defines the purpose of the audit engagement, which is an independent examination of the client's financial statements. It outlines the extent of the audit, whether it includes a full audit, specific accounts, or certain periods. 3. Responsibilities: This clause outlines the responsibilities of both the accounting firm and the client. It includes the client's duty to provide accurate and complete financial records and internal controls, and the accounting firm's obligation to perform the audit in accordance with professional standards and provide an unbiased opinion. 4. Timing and timeline: This section specifies the expected start and end dates, and the timeline for delivering the final audit report. It may also include milestones, such as periodic meetings or interim reporting, to ensure effective progress monitoring. 5. Fees and payment terms: This component covers the audit fees, billing arrangements, and the payment terms. It may include details about hourly rates, estimated timeframes, and any additional expenses that may be incurred during the audit. 6. Confidentiality: This clause emphasizes the importance of maintaining the confidentiality of client information obtained during the audit process. It ensures that all parties involved understand their obligations to handle sensitive data with the utmost care and prevents unauthorized disclosure. 7. Termination clause: This section outlines the conditions under which either party can terminate the engagement before completion. It may include reasons for termination, any notice period required, and the associated consequences or liabilities. Different types of Nevada Engagement Letters for Audit Services may include: 1. Full-Scope Audit Engagement: This type of engagement letter covers a comprehensive examination of the client's financial statements, including balance sheets, income statements, and cash flow statements. It involves detailed testing of transactions and account balances. 2. Limited-Scope Audit Engagement: In certain cases, a client may request a limited-scope audit that focuses on specific accounts, areas, or transactions. This engagement letter clearly defines the limitations and exclusions associated with the scope of the audit. 3. Review Engagement or Compilation Engagement: While not technically audits, review engagements or compilation engagements also require engagement letters. These engagements provide limited assurance or no assurance, respectively, on the financial statements and have less extensive procedures compared to a full audit. In conclusion, the Nevada Engagement Letter for Audit Services is a critical document that establishes the foundation for a successful audit engagement. It ensures a clear understanding between the accounting firm and the client, setting expectations, responsibilities, and terms for the audit.