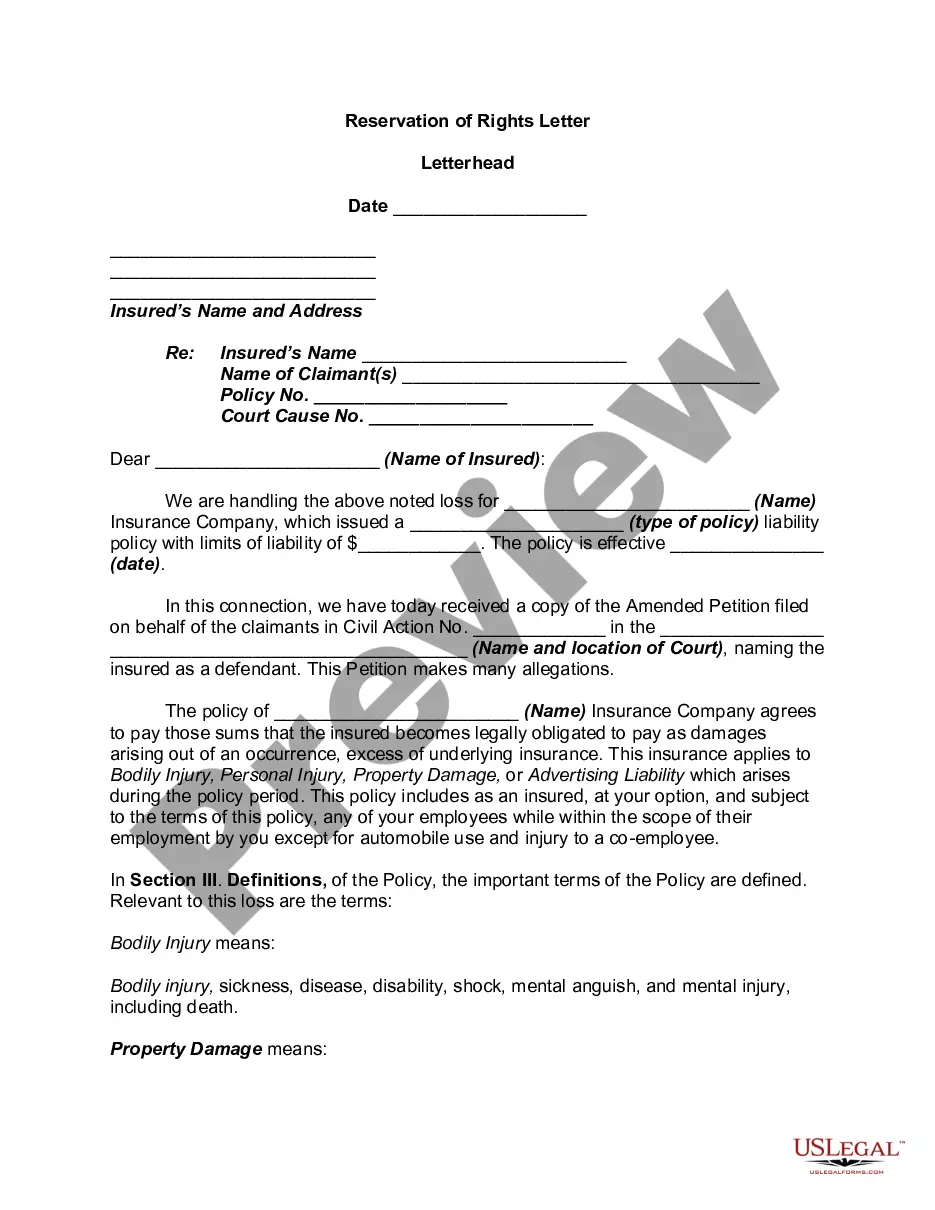

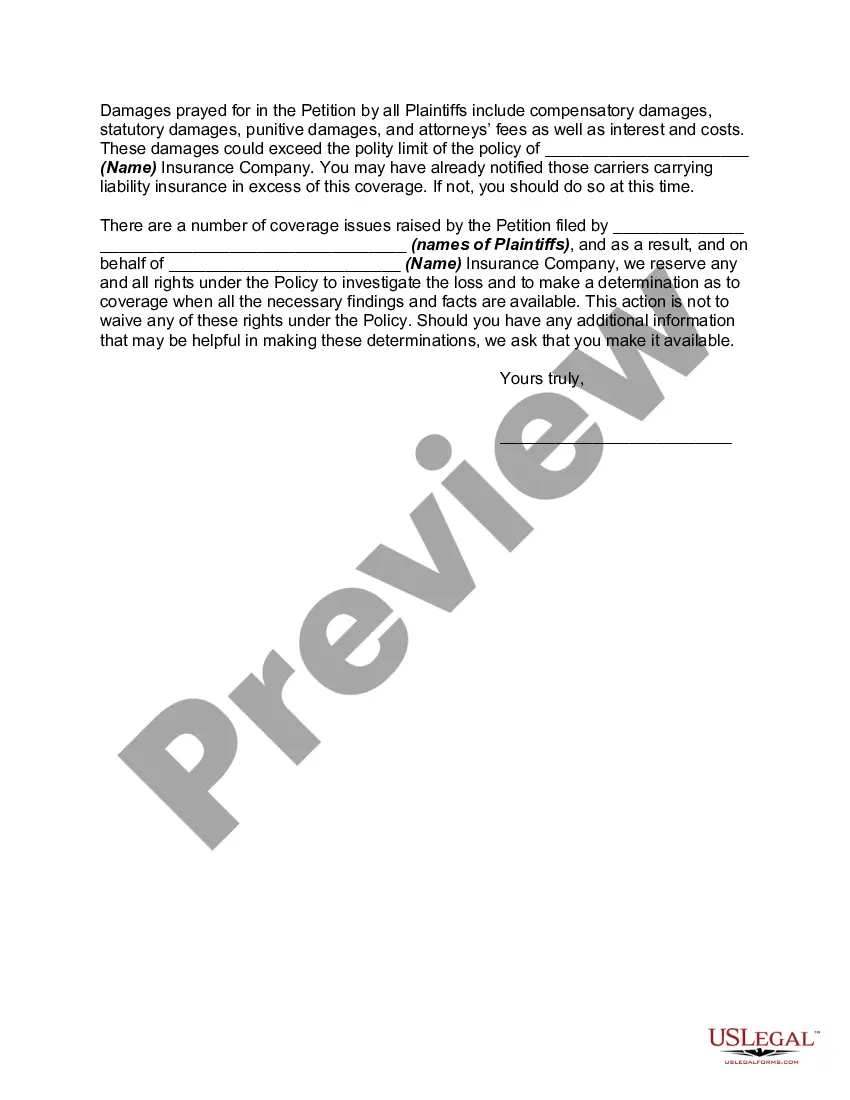

A reservation of rights defense is a means by which a liability insurance carrier agrees to protect and defend its insured against a claim or suit while reserving the right to further evaluate and perhaps even deny coverage for some or all of the claim. It is most commonly used when the claim or suit contains both covered and non-covered allegations, when the allegations are in excess of policy limits, or when the insurer is still investigating its defense and coverage obligations. For the insurer, a reservation of rights provides the flexibility to satisfy its duty to defend without committing to coverage. For the business owner who ultimately may have to pay for an adverse judgment, it requires careful monitoring and attention.

A Nevada Reservation of Rights Letter is a legal document that is typically sent by an insurance company to a policyholder or third party. This letter serves to inform the recipient that the insurance company is reserving its rights to deny coverage or defend claims made under an insurance policy. Keywords: Nevada, Reservation of Rights Letter, insurance company, policyholder, third party, coverage, defend claims. There are various types of Nevada Reservation of Rights Letters that may be issued by insurance companies. Some common types include: 1. Coverage Reservation of Rights Letter: This letter is sent by an insurance company to a policyholder when it believes that certain claims made under the policy may not be covered. It sets forth specific reasons for the potential denial of coverage and notifies the policyholder that the insurance company is reserving its right to deny payment for such claims. 2. Duty to Defend Reservation of Rights Letter: This type of letter is sent by an insurance company to a policyholder or third party when a claim is made under a liability insurance policy. It outlines the conditions under which the insurance company may or may not provide a legal defense for the insured. By issuing this letter, the insurance company typically reserves its right to withdraw from the duty to defend if it later determines that the claim falls outside the policy's coverage. 3. Timely Notice Reservation of Rights Letter: In Nevada, insurance policies often have provisions requiring policyholders to promptly report any potential claims or incidents that may give rise to a claim. When a policyholder fails to provide timely notice, an insurance company may send a Timely Notice Reservation of Rights Letter. This letter informs the policyholder that their failure to comply with the notice requirement may jeopardize their coverage rights, and reserves the insurance company's right to deny the claim based on the untimely notice. 4. Fraud or Misrepresentation Reservation of Rights Letter: If an insurance company suspects that the policyholder made fraudulent statements or misrepresented information at the time of purchasing the policy or filing a claim, it may send this type of letter. The letter alerts the policyholder to the insurance company's suspicion and states that it reserves its right to refuse coverage or pursue legal action if fraud or misrepresentation is proven. In conclusion, a Nevada Reservation of Rights Letter is a vital legal communication by insurance companies to establish their reservation of rights to deny coverage or defend against claims. These letters help maintain transparency and clarity between insurance companies and policyholders or third parties, ensuring appropriate procedures are followed in accordance with the insurance policy's terms and conditions.