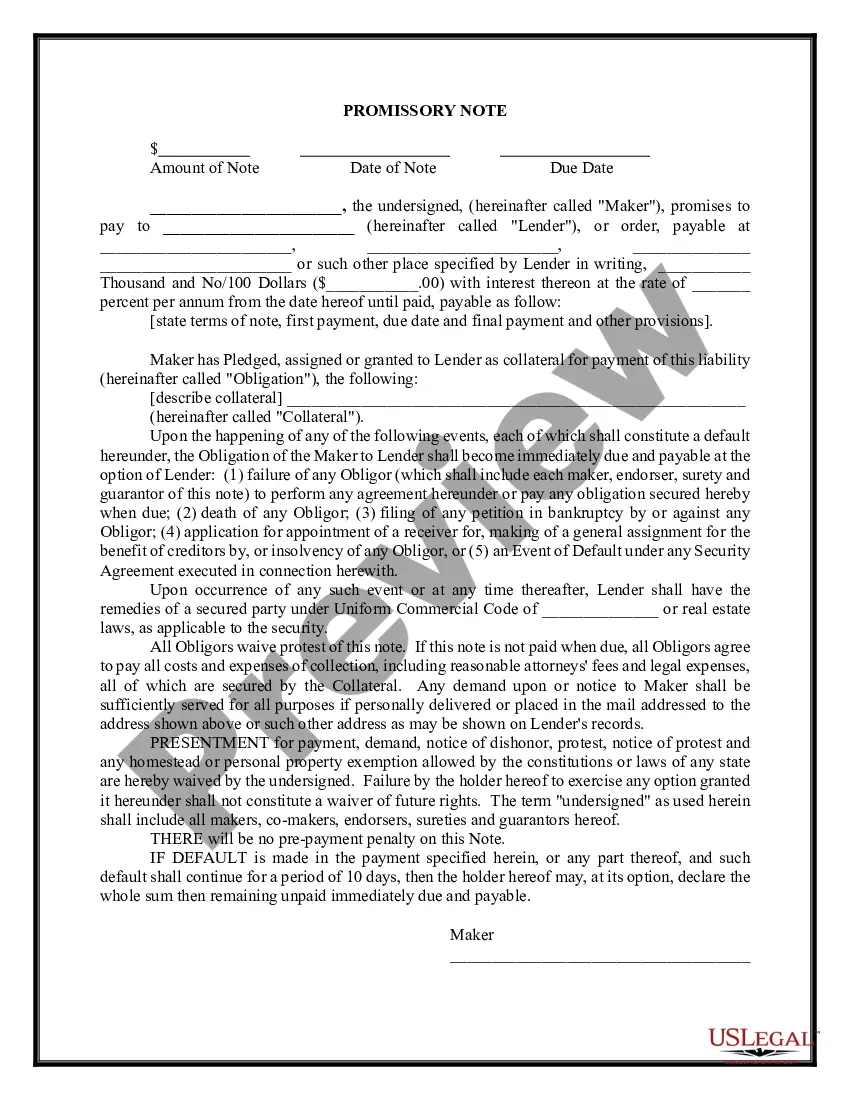

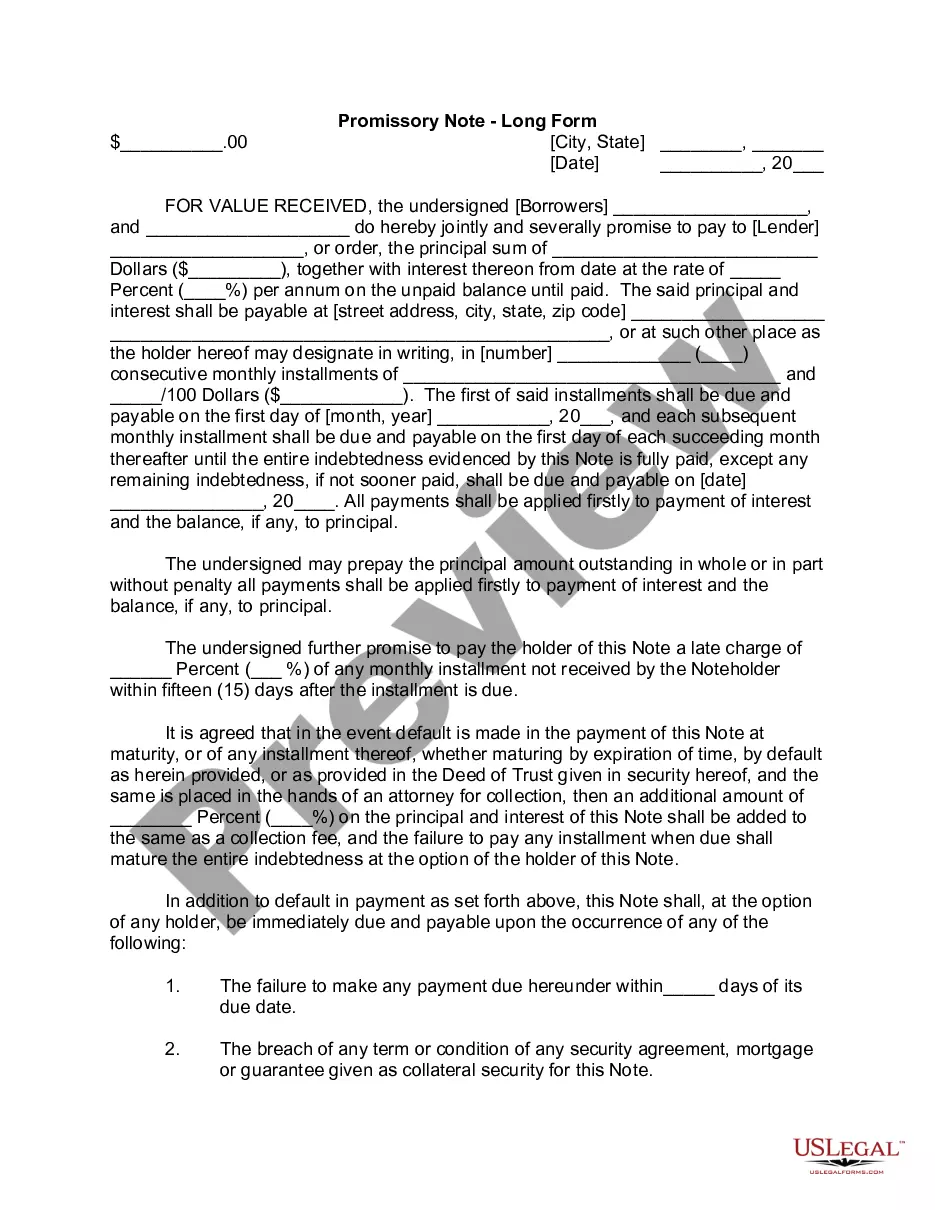

A promissory note is a written promise to pay a debt. An unconditional promise to pay on demand or at a fixed or determined future time a particular sum of money to or to the order of a specified person or to the bearer.

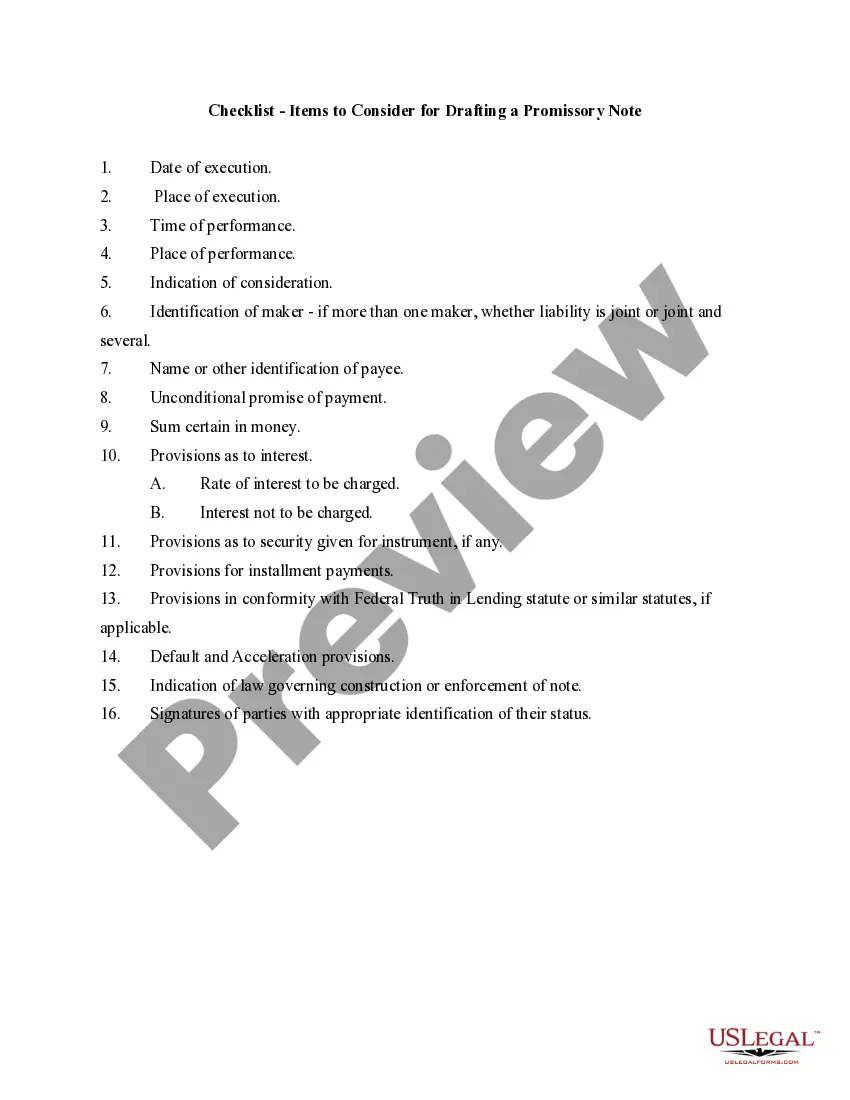

Nevada Checklist - Items to Consider for Drafting a Promissory Note

Category:

State:

Multi-State

Control #:

US-03060BG

Format:

Word;

Rich Text

Instant download

Description

How to fill out Checklist - Items To Consider For Drafting A Promissory Note?

You might devote numerous hours on the web searching for the valid documents template that aligns with the state and federal requirements you need.

US Legal Forms offers a vast array of legal templates that are examined by specialists.

You can easily download or print the Nevada Checklist - Items to Consider for Drafting a Promissory Note from our services.

First, ensure that you have selected the correct document template for your area of choice. Review the form information to confirm you have picked the right one. If available, use the Review button to preview the document template as well. If you wish to find another version of the form, utilize the Search field to seek out the template that meets your requirements.

- If you already have a US Legal Forms account, you can Log In and click the Download button.

- Then, you can complete, modify, print, or sign the Nevada Checklist - Items to Consider for Drafting a Promissory Note.

- Every legal document template you acquire is yours indefinitely.

- To get another copy of any obtained form, visit the My documents tab and click the corresponding button.

- If you are using the US Legal Forms website for the first time, follow the straightforward directions below.

Form popularity

FAQ

A promissory note should include essential components such as the principal amount, interest rate, payment schedule, and any penalties for late payments. It's also important to note the rights and responsibilities of both parties. Including these elements ensures clarity and reduces the potential for disputes. Use the Nevada Checklist - Items to Consider for Drafting a Promissory Note to help you cover all necessary aspects.

The format of a promissory note usually includes a title, date, amount borrowed, interest rates, and repayment terms. It should be clear and concise to avoid confusion. Typically, it contains both the borrower's and lender's names and signatures at the end. Following the Nevada Checklist - Items to Consider for Drafting a Promissory Note can guide you in structuring this important document.

Promissory notes can take various forms, depending on the nature of the agreement. For instance, unsecured personal loans and student loans are common examples. Additionally, promissory notes may be used in real estate transactions or business loans. When considering these documents, refer to the Nevada Checklist - Items to Consider for Drafting a Promissory Note to ensure completeness.

Promissory notes must follow specific rules to be valid. They should clearly state the terms, including payment schedules, interest rates, and any penalties for late payments. Utilizing the Nevada Checklist - Items to Consider for Drafting a Promissory Note ensures you include all critical elements of the agreement. Following these rules protects both parties and strengthens the legal enforceability of the note.

A promissory note is legally binding when it includes essential elements such as an agreed amount, a scheduled repayment date, and the signatures of both the borrower and lender. To ensure compliance with the law, refer to the Nevada Checklist - Items to Consider for Drafting a Promissory Note. This checklist helps you understand requirements and protect your interests. Properly drafted notes reduce disputes and clarify obligations.

A promissory note does not necessarily need to be notarized to be legal, provided it meets all other requirements. However, notarization can serve as additional proof of authenticity if disputes arise. Reviewing the Nevada Checklist - Items to Consider for Drafting a Promissory Note will help you understand when notarization may be beneficial. Consider using our platform to generate documents that meet all legal standards.

Whether you need a witness for a promissory note can vary by state and situation. In Nevada, it is usually not a requirement, but having a witness can add an extra layer of protection. Consulting the Nevada Checklist - Items to Consider for Drafting a Promissory Note can provide clarity on this. If in doubt, it’s wise to consult a legal expert for guidance.

For a promissory note to be valid, it must include the essential terms and be signed by the maker. Following the Nevada Checklist - Items to Consider for Drafting a Promissory Note, you will ensure your note meets local laws. The parties involved should also understand their rights and obligations as outlined in the document. Ensuring proper execution adds to the document's enforceability.

Legal requirements for a promissory note include a clear statement of the amount owed, terms of repayment, and signatures from both parties. Reviewing the Nevada Checklist - Items to Consider for Drafting a Promissory Note ensures you include all necessary components. You may also want to consider whether you need a witness or not, depending on local laws. This attention to detail can prevent disputes in the future.

To legalize a promissory note, ensure it meets the local and state laws outlined in your Nevada Checklist - Items to Consider for Drafting a Promissory Note. This often involves having the document properly signed by all parties involved. In some cases, you may want to include a witness, though this is not always necessary. Additionally, keeping a copy for your records can be very beneficial.