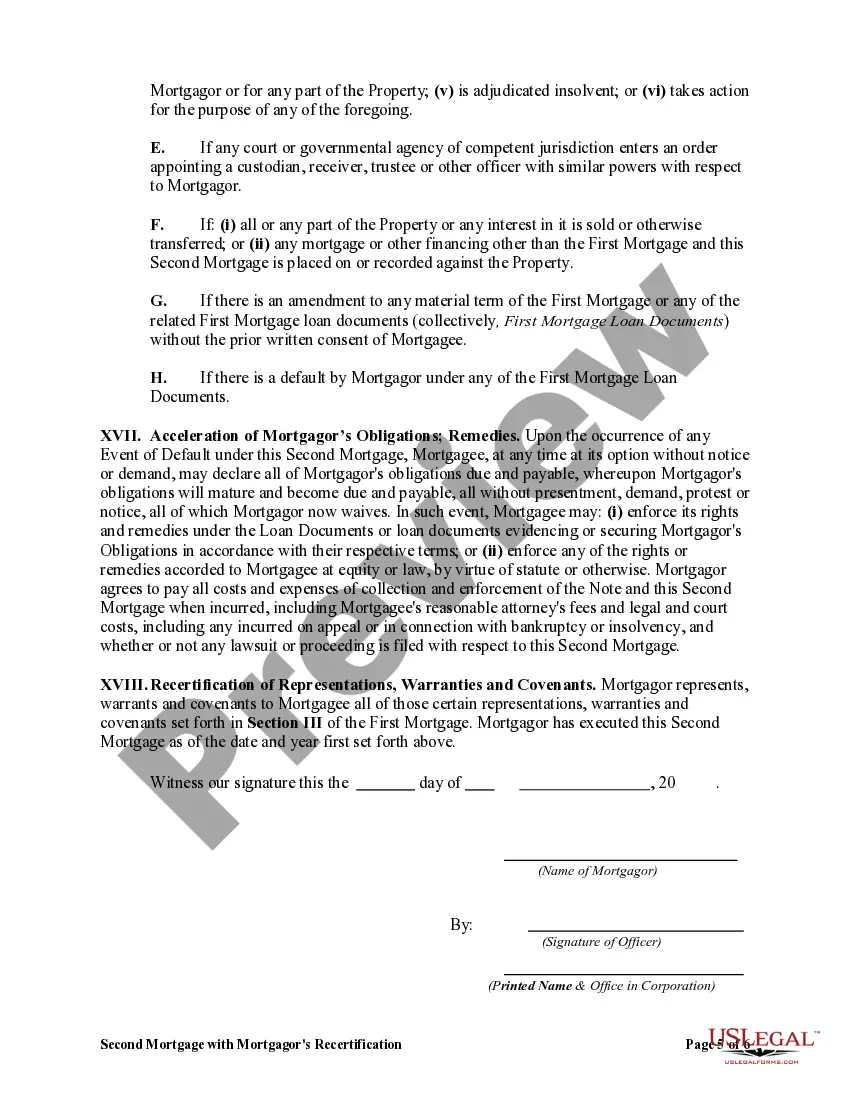

Nevada Second Mortgage with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage A Nevada Second Mortgage with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage is a legal document that pertains to a second mortgage taken out by a borrower in the state of Nevada. This mortgage instrument comprises certain clauses and provisions that require the mortgagor to reaffirm their previous representations, warranties, and covenants made in the first mortgage. Keywords: Nevada, Second Mortgage, Mortgagor's Recertification, Representations, Warranties, Covenants, First Mortgage This type of mortgage is commonly used when a borrower needs to access additional funds while keeping their existing first mortgage intact. By taking out a second mortgage, the borrower pledges additional collateral, typically the same property used to secure the primary mortgage, to secure the new loan. The use of the term "Mortgagor's Recertification of Representations, Warranties, and Covenants" refers to the mortgagor (borrower) providing a renewed confirmation of the accuracy and truthfulness of the statements made in the initial mortgage agreement. Representations generally include statements regarding the borrower's financial status, employment, and creditworthiness. Warranties refer to guarantees provided by the borrower regarding the property's condition, title, and legal compliance. Covenants are obligations the borrower agrees to fulfill during the mortgage term, such as making timely mortgage installment payments. Different types of Nevada Second Mortgage with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage may exist depending on the specific terms and conditions agreed upon between the lender and the borrower, such as: 1. Fixed-Rate Second Mortgage: In this type of second mortgage, the interest rate remains constant throughout the loan term, providing the borrower with predictable payment amounts. 2. Adjustable-Rate Second Mortgage: This mortgage structure involves an interest rate that may change periodically, typically based on an index or market conditions. The variation in interest rates can lead to fluctuating payments for the borrower. 3. Home Equity Line of Credit (HELOT): A HELOT is a type of revolving credit where the borrower can access funds up to a predetermined limit. The borrower can withdraw and repay funds multiple times, typically within a specified draw period. The interest charged is typically variable. 4. Closed-End Second Mortgage: This type of mortgage provides the borrower with a lump sum payment, often used for specific purposes, such as financing home improvements or consolidating other debts. The loan is repaid over a fixed term. It is important for borrowers to carefully review and understand the terms and conditions outlined in the Nevada Second Mortgage with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage document before signing. Seeking professional legal advice may be helpful to ensure compliance and clarity of obligations.

Nevada Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage

Description

How to fill out Nevada Second Mortgage With Mortgagor's Recertification Of Representations, Warranties And Covenants In First Mortgage?

Are you in a placement in which you need paperwork for possibly business or person reasons nearly every day? There are tons of legal document web templates available online, but discovering kinds you can rely on isn`t easy. US Legal Forms offers a large number of kind web templates, such as the Nevada Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage, that are created to satisfy federal and state specifications.

Should you be previously familiar with US Legal Forms web site and also have a free account, merely log in. Next, you can obtain the Nevada Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage template.

Should you not provide an profile and want to start using US Legal Forms, follow these steps:

- Find the kind you will need and ensure it is for the proper town/area.

- Use the Review button to examine the form.

- Read the explanation to actually have selected the proper kind.

- In the event the kind isn`t what you are looking for, make use of the Look for field to discover the kind that meets your requirements and specifications.

- Whenever you get the proper kind, click Get now.

- Opt for the prices plan you would like, fill out the desired information and facts to make your money, and pay money for an order using your PayPal or bank card.

- Select a practical file format and obtain your version.

Locate all of the document web templates you have bought in the My Forms food list. You can get a additional version of Nevada Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage any time, if necessary. Just click the needed kind to obtain or produce the document template.

Use US Legal Forms, the most considerable variety of legal kinds, to save efforts and steer clear of mistakes. The service offers skillfully made legal document web templates which you can use for a variety of reasons. Generate a free account on US Legal Forms and start making your life easier.