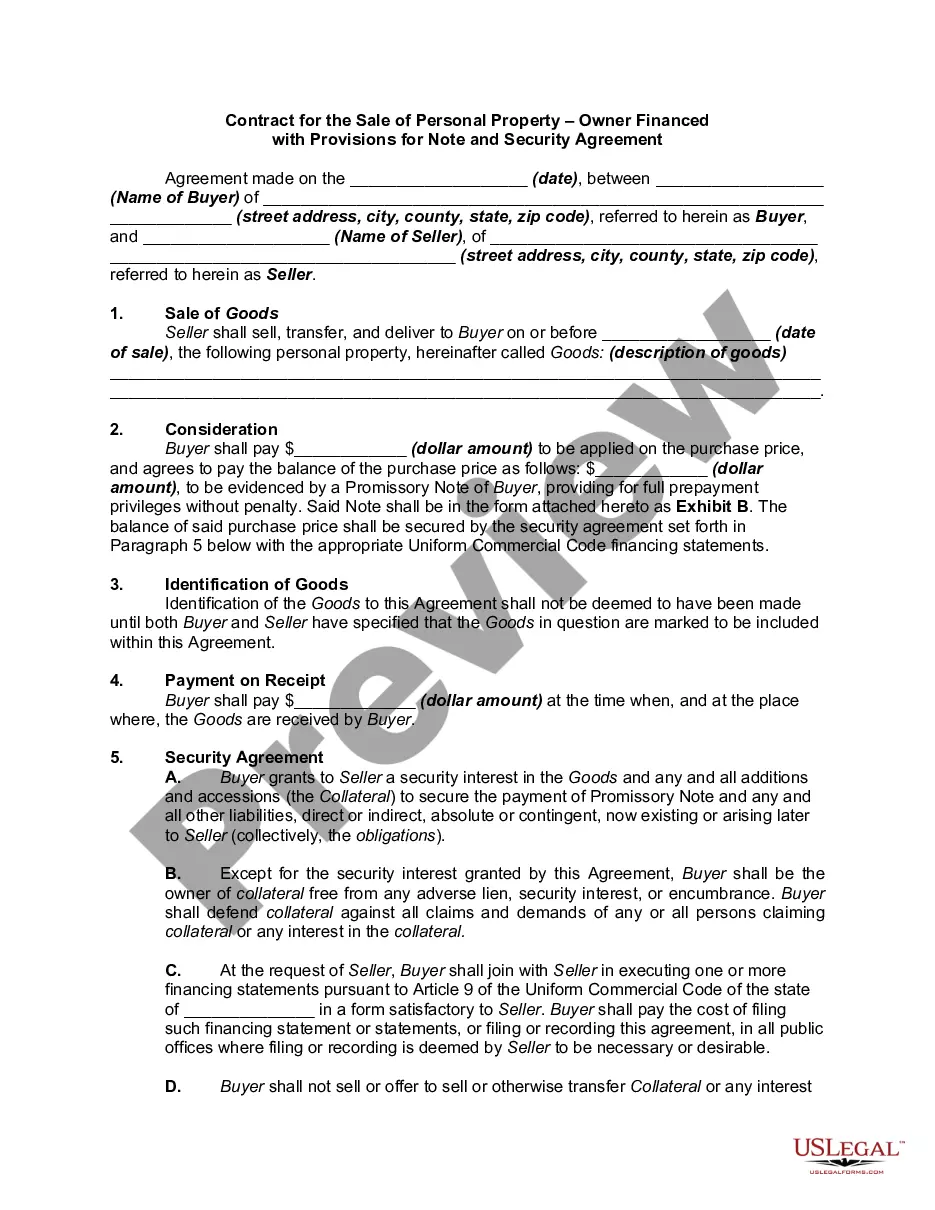

Nevada Loan Agreement for Car

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Loan Agreement For Car?

You can invest time on-line attempting to find the authorized record format that fits the federal and state demands you need. US Legal Forms offers 1000s of authorized kinds that are analyzed by specialists. You can easily acquire or print the Nevada Loan Agreement for Car from your service.

If you have a US Legal Forms bank account, you can log in and then click the Down load button. Next, you can full, modify, print, or indication the Nevada Loan Agreement for Car. Every single authorized record format you acquire is your own property forever. To acquire yet another backup for any bought form, proceed to the My Forms tab and then click the related button.

If you are using the US Legal Forms site initially, stick to the straightforward instructions listed below:

- Initially, be sure that you have chosen the correct record format for the area/city of your choice. Look at the form information to make sure you have picked the right form. If offered, utilize the Review button to appear through the record format too.

- In order to discover yet another edition from the form, utilize the Research industry to get the format that suits you and demands.

- Once you have discovered the format you want, click Buy now to carry on.

- Select the costs program you want, enter your accreditations, and register for your account on US Legal Forms.

- Full the transaction. You should use your bank card or PayPal bank account to fund the authorized form.

- Select the format from the record and acquire it to the gadget.

- Make alterations to the record if required. You can full, modify and indication and print Nevada Loan Agreement for Car.

Down load and print 1000s of record templates making use of the US Legal Forms web site, that provides the largest collection of authorized kinds. Use skilled and express-particular templates to take on your business or individual requirements.

Form popularity

FAQ

Usually, an IOU and a promissory note form are only signed by the borrower, although they may be signed by both parties. A loan agreement is a single document that contains all of the terms of the loan, and is signed by both parties.

What a personal loan agreement should include Legal names and address of both parties. Names and address of the loan cosigner (if applicable). Amount to be borrowed. Date the loan is to be provided. Repayment date. Interest rate to be charged (if applicable). Annual percentage rate (if applicable).

First and foremost, understand that personal loan agreements fall into the classification of contracts. Technically, you don't have to notarize these documents. But if you want to make this document legally binding, then notarization is the best course of action.

Promissory notes don't have to be notarized in most cases. You can typically sign a legally binding promissory note that contains unconditional pledges to pay a certain sum of money. However, you can strengthen the legality of a valid promissory note by having it notarized.

To draft a Loan Agreement, you should include the following: The addresses and contact information of all parties involved. The conditions of use of the loan (what the money can be used for) Any repayment options. The payment schedule. The interest rates.

In most cases, a contract does not have to be notarized since the signed contract itself is enforceable and legally binding in state or federal courts. Many types of written contracts don't require a notary public to be valid.

For a personal loan agreement to be enforceable, it must be documented in writing, as well as signed and dated by all parties involved. It's also a good idea to have the document notarized or signed by a witness.

Loan agreements typically include covenants, value of collateral involved, guarantees, interest rate terms and the duration over which it must be repaid.