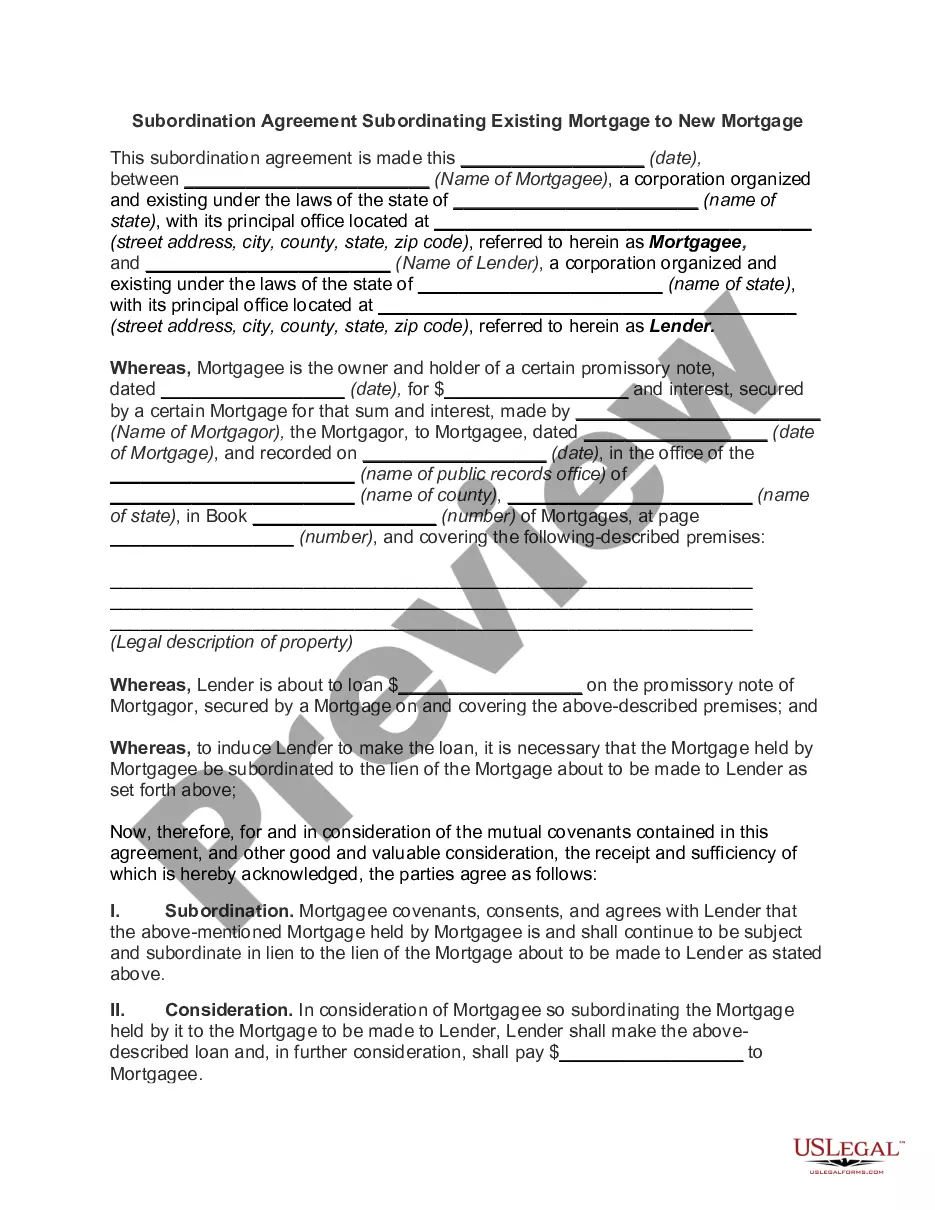

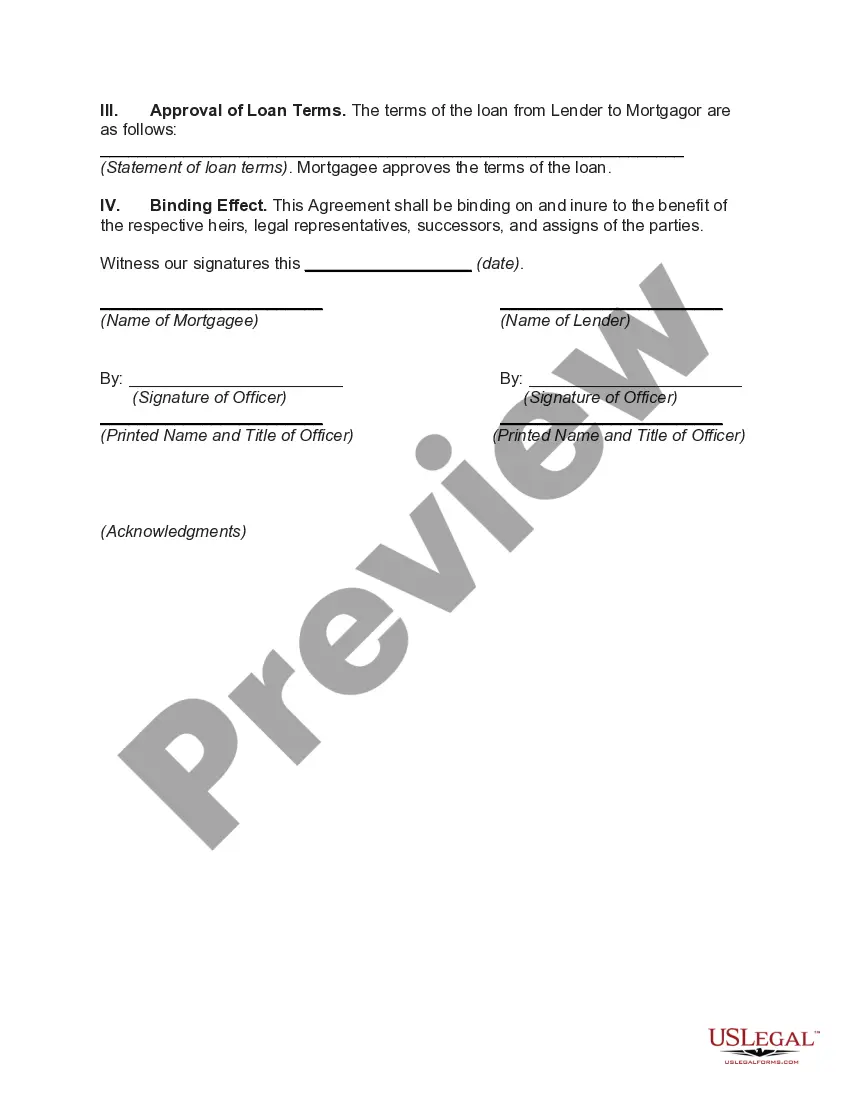

A Nevada Subordination Agreement Subordinating Existing Mortgage to New Mortgage is a legal document used in real estate transactions to establish the priority of different mortgages on a property. This agreement allows the borrower to obtain a new loan while maintaining the existing mortgage. In Nevada, there are two types of Subordination Agreements that can be used to subordinate an existing mortgage to a new mortgage: 1. Nevada Subordination Agreement for Home Equity Line of Credit (HELOT): This type of agreement is commonly used when a homeowner wants to take out a second mortgage or a home equity line of credit. By subordinating the existing mortgage, the lender of the new loan takes priority in case of a foreclosure. 2. Nevada Subordination Agreement for Refinancing: This type of agreement is used when a homeowner wants to refinance their existing mortgage with a new loan. By signing this agreement, the lender of the new loan becomes the primary lien holder, and the existing mortgage is subordinated to the new one. The Nevada Subordination Agreement is a critical document when multiple loans are involved in a real estate transaction. It ensures that the lenders are aware of the priority of their liens on the property. Without this agreement, the order of priority can create complications during foreclosure or in case of default. When drafting a Nevada Subordination Agreement Subordinating Existing Mortgage to New Mortgage, it is important to include details such as the names of the borrower, the lender of the existing mortgage, the lender of the new mortgage, the loan amounts, the property in question, and the terms of the subordination. By signing this agreement, the borrower acknowledges and agrees to the priority of the new mortgage over the existing one. It also grants permission for the lenders to exchange information and communicate regarding the loans. In conclusion, a Nevada Subordination Agreement Subordinating Existing Mortgage to New Mortgage is a crucial legal document used in real estate transactions involving multiple mortgages. It establishes the priority of the loans and ensures a clear understanding between lenders and borrowers.

Nevada Subordination Agreement Subordinating Existing Mortgage to New Mortgage

Description

How to fill out Nevada Subordination Agreement Subordinating Existing Mortgage To New Mortgage?

You can spend hours online attempting to find the legitimate file format that meets the state and federal needs you will need. US Legal Forms supplies a huge number of legitimate types that are reviewed by specialists. You can easily download or print out the Nevada Subordination Agreement Subordinating Existing Mortgage to New Mortgage from my assistance.

If you already have a US Legal Forms account, you may log in and click on the Obtain button. Following that, you may total, edit, print out, or sign the Nevada Subordination Agreement Subordinating Existing Mortgage to New Mortgage. Each and every legitimate file format you buy is yours permanently. To acquire an additional copy for any bought develop, visit the My Forms tab and click on the corresponding button.

Should you use the US Legal Forms website the very first time, adhere to the easy instructions listed below:

- Initial, be sure that you have selected the best file format for that area/city that you pick. Look at the develop explanation to ensure you have selected the correct develop. If available, take advantage of the Preview button to check throughout the file format as well.

- In order to find an additional model of your develop, take advantage of the Look for field to get the format that suits you and needs.

- Once you have found the format you would like, click Get now to carry on.

- Choose the pricing prepare you would like, type your credentials, and register for a free account on US Legal Forms.

- Comprehensive the transaction. You may use your Visa or Mastercard or PayPal account to fund the legitimate develop.

- Choose the file format of your file and download it in your gadget.

- Make modifications in your file if required. You can total, edit and sign and print out Nevada Subordination Agreement Subordinating Existing Mortgage to New Mortgage.

Obtain and print out a huge number of file templates using the US Legal Forms site, which provides the biggest selection of legitimate types. Use specialist and condition-specific templates to take on your organization or personal demands.