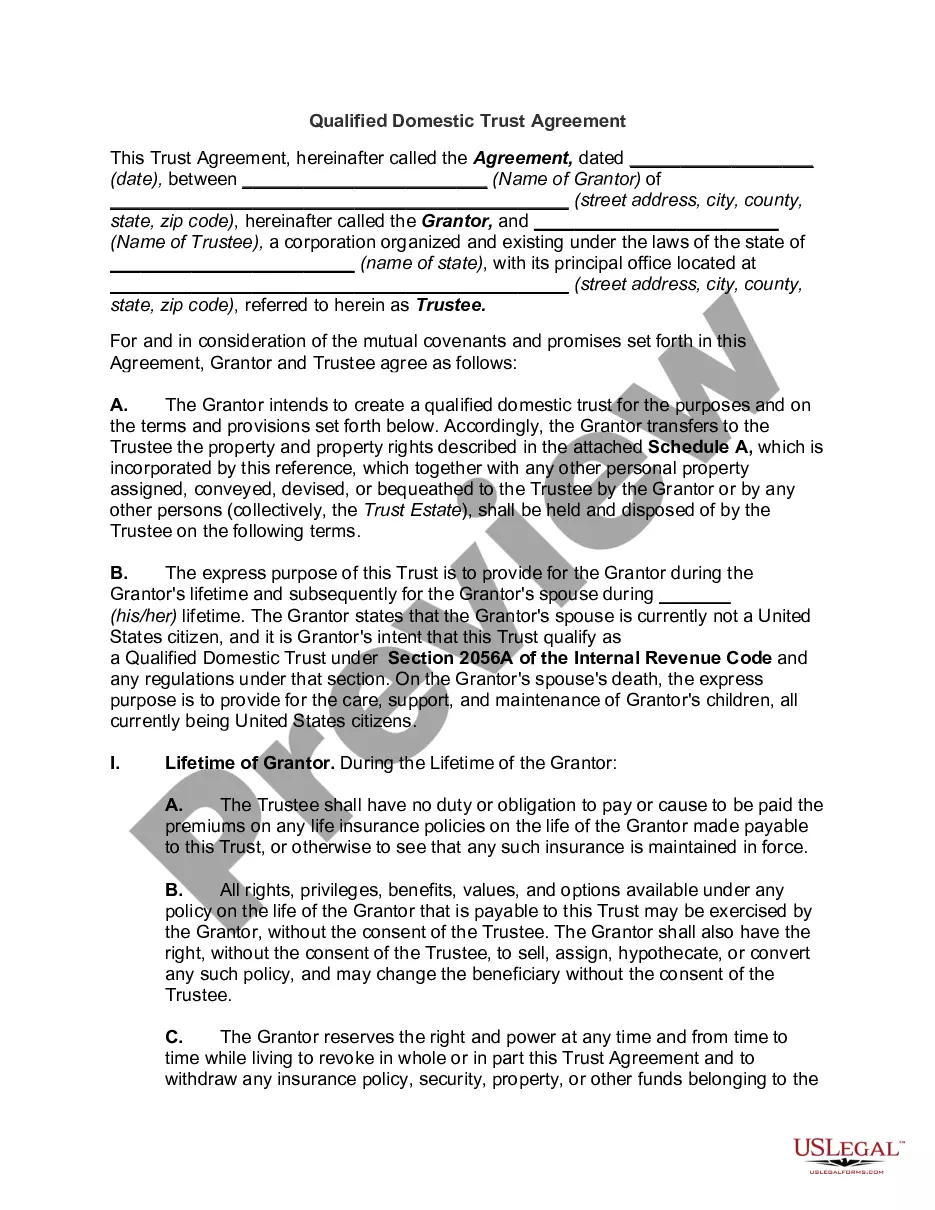

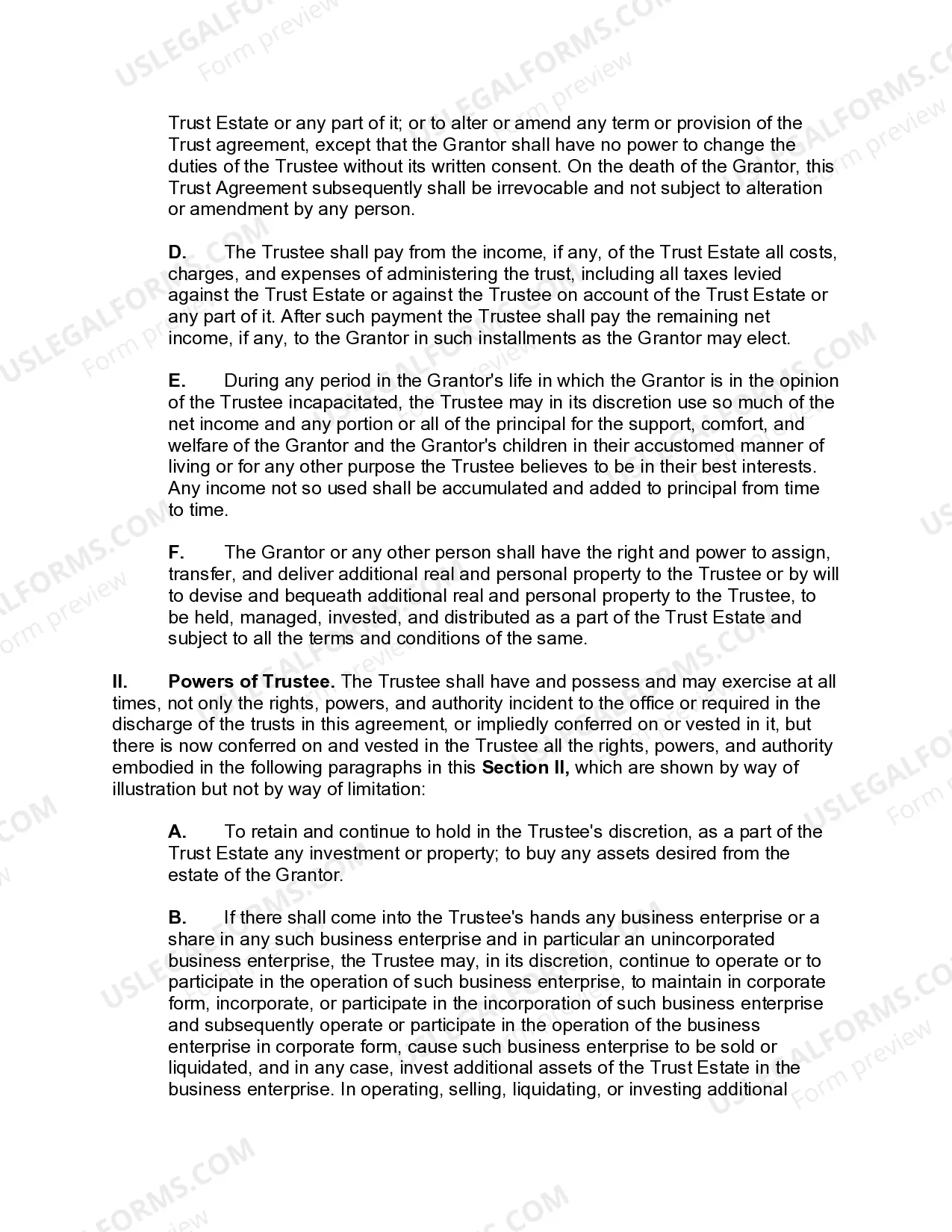

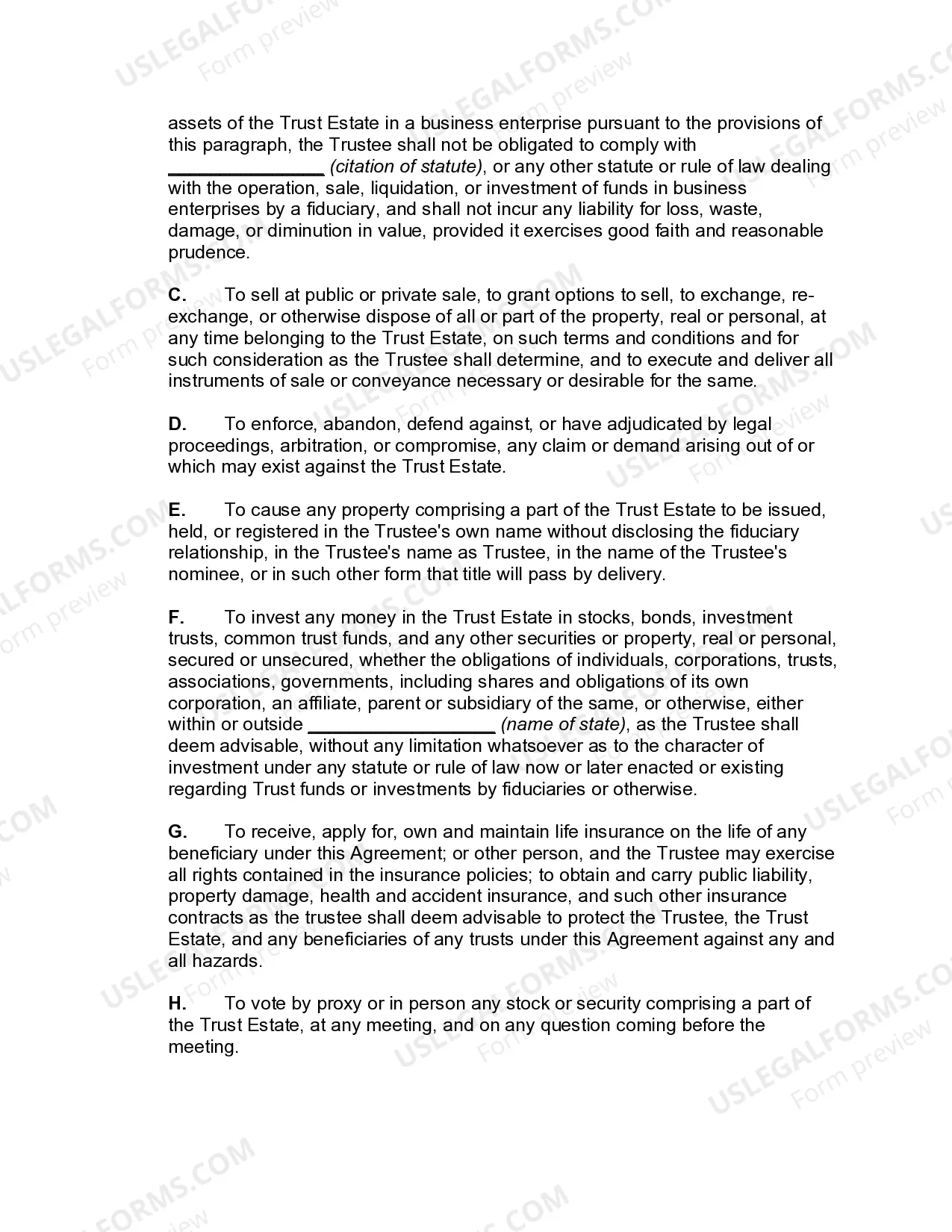

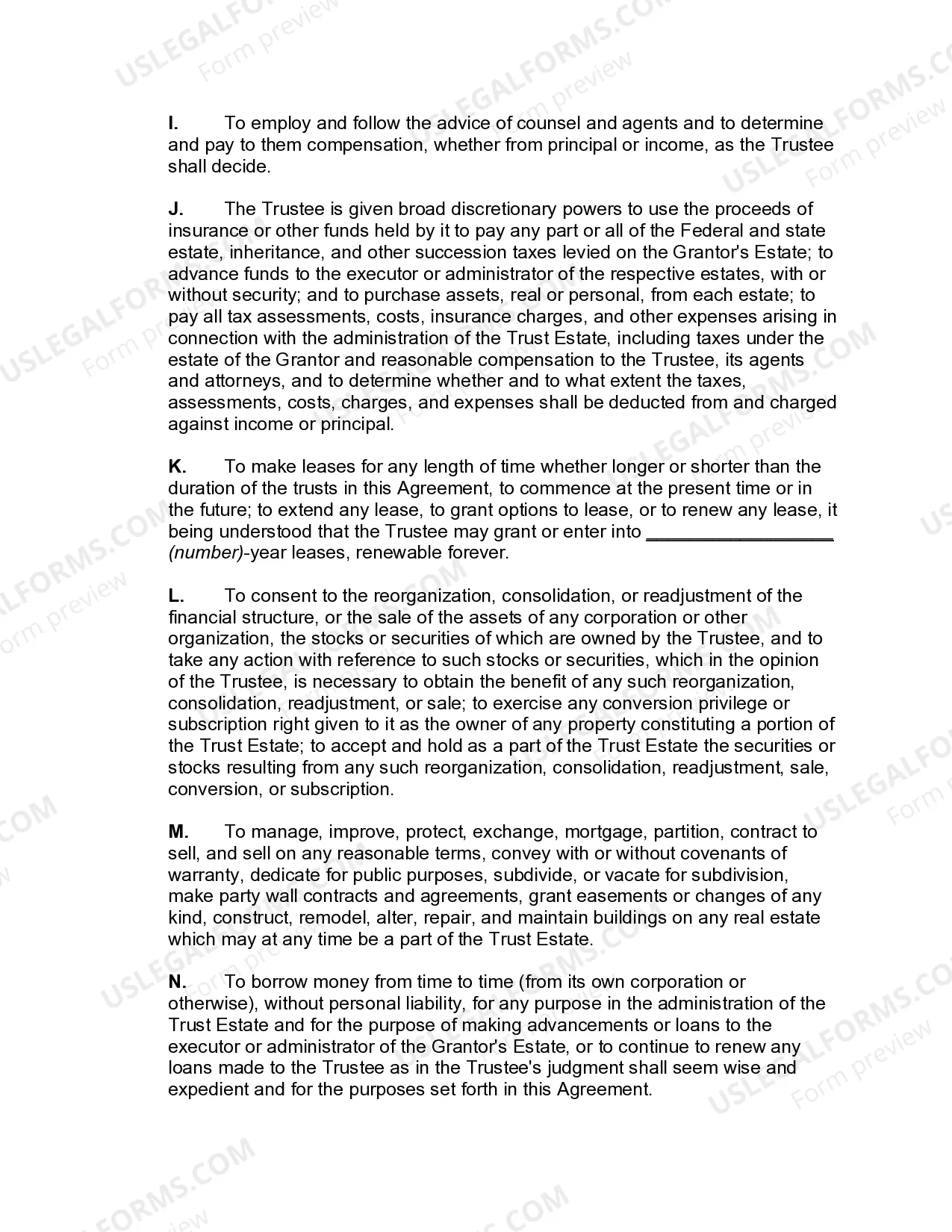

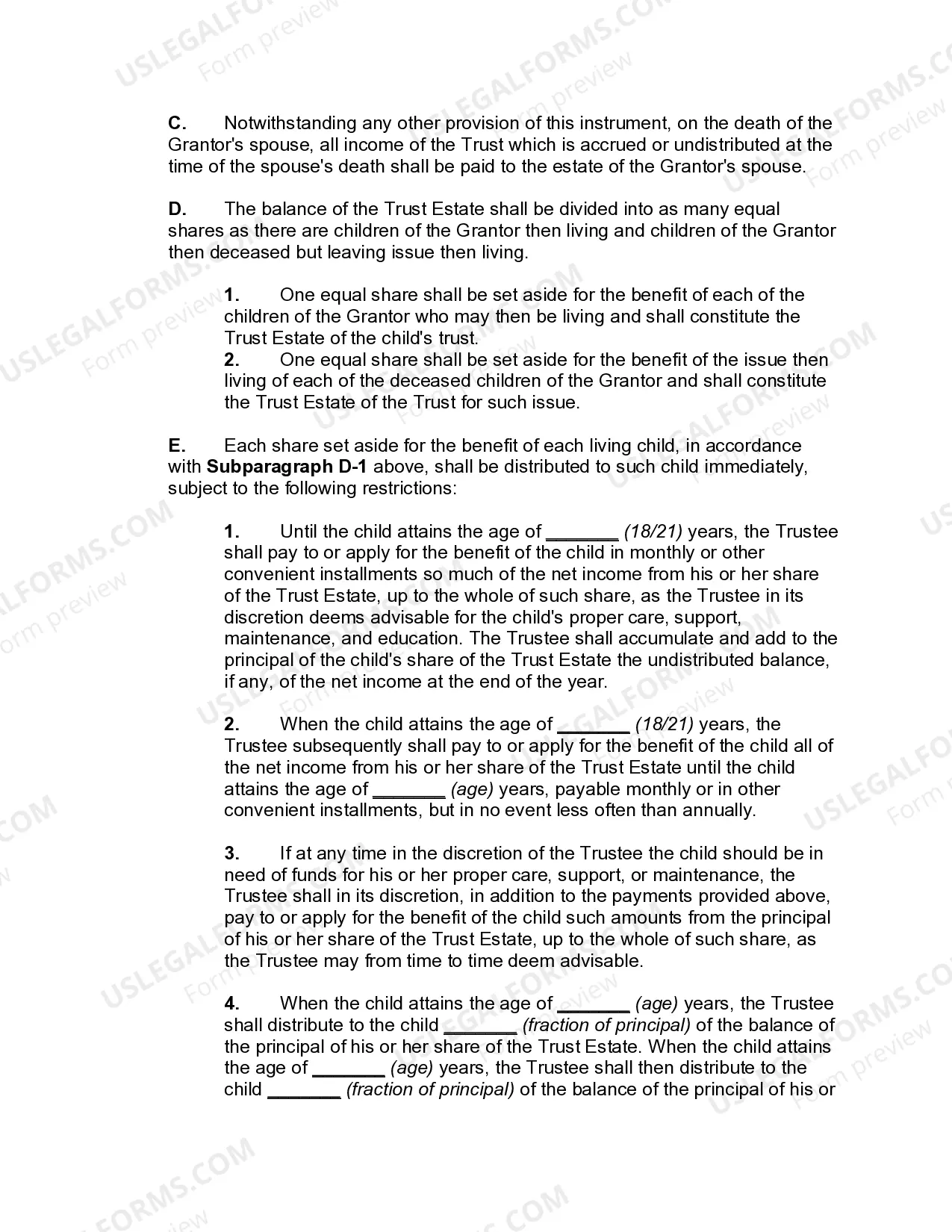

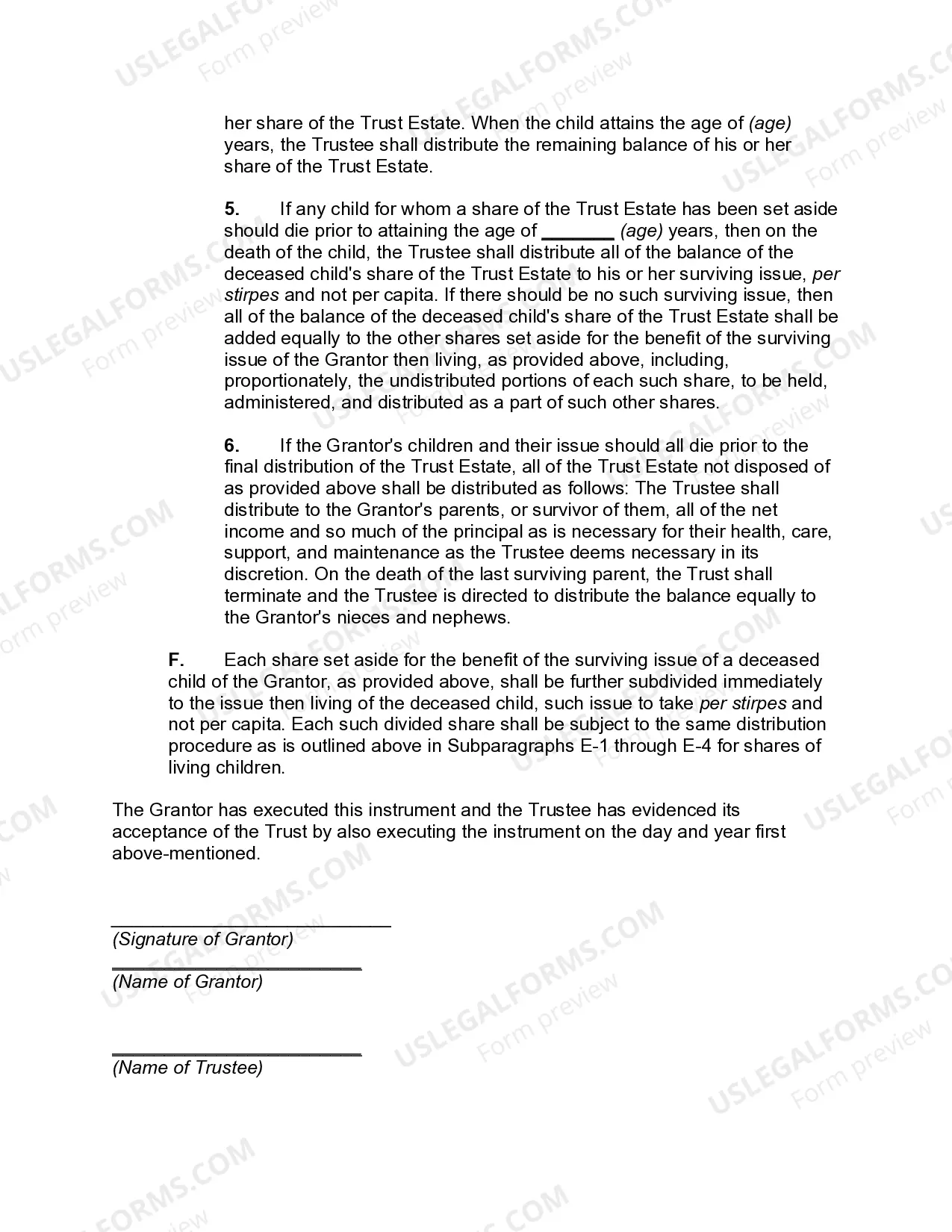

A Nevada Qualified Domestic Trust Agreement (DOT) is a legal document that allows non-U.S. citizen spouses to benefit from an estate plan set up by their U.S. citizen spouses. This agreement ensures that the non-U.S. citizen surviving spouse can continue to receive income from the estate without triggering excessive estate taxes. A DOT is necessary because non-U.S. citizen spouses are subject to estate tax laws that differ from those applied to U.S. citizens. Without a DOT, the estate tax would be due immediately upon the death of the U.S. citizen spouse, potentially causing significant financial hardship for the surviving spouse. By establishing a Nevada DOT, the U.S. citizen spouse sets aside assets for the benefit of the non-citizen spouse in a qualified trust. This trust must meet certain requirements dictated by the Internal Revenue Service (IRS) to achieve DOT status. One of the primary requirements is that the DOT must have at least one U.S. trustee who is responsible for overseeing the administration of the trust. One of the main advantages of a Nevada DOT is that it allows for the deferral of estate taxes until distributions are made to the non-U.S. citizen surviving spouse. This deferral provides financial flexibility for the surviving spouse and helps to ensure a stable income stream for their well-being. There are two main types of Nevada DOT agreements based on the potential for distribution to the non-citizen surviving spouse: 1. Immediate Distribution DOT: This agreement allows for distributions of both income and principal to the non-U.S. citizen spouse immediately, subject to certain limitations and requirements set by the IRS. 2. Income-Only Distribution DOT: This agreement restricts distributions to the non-U.S. citizen spouse to income only. Any principal distributions from the trust will trigger estate tax liability. This type of DOT is often utilized when the estate is larger or when the spouse has substantial income needs. In conclusion, a Nevada Qualified Domestic Trust Agreement (DOT) is a crucial tool in estate planning for U.S. citizens with non-U.S. citizen spouses. It provides a tax-efficient way to ensure financial security for the non-U.S. citizen surviving spouse while meeting the requirements set by the IRS. By establishing a DOT, one can minimize the potential impact of estate taxes and facilitate a smooth transfer of assets to the surviving spouse.

Nevada Qualified Domestic Trust Agreement

Description

How to fill out Nevada Qualified Domestic Trust Agreement?

If you wish to full, acquire, or produce legitimate document web templates, use US Legal Forms, the greatest collection of legitimate forms, which can be found online. Utilize the site`s basic and convenient look for to obtain the paperwork you require. A variety of web templates for business and specific reasons are sorted by groups and says, or keywords and phrases. Use US Legal Forms to obtain the Nevada Qualified Domestic Trust Agreement with a number of click throughs.

In case you are previously a US Legal Forms customer, log in to the profile and then click the Obtain key to get the Nevada Qualified Domestic Trust Agreement. You can also gain access to forms you earlier delivered electronically from the My Forms tab of the profile.

If you are using US Legal Forms initially, follow the instructions under:

- Step 1. Be sure you have chosen the form to the correct town/region.

- Step 2. Utilize the Preview option to examine the form`s content material. Never forget to read the information.

- Step 3. In case you are unsatisfied with the kind, use the Search field near the top of the screen to discover other versions in the legitimate kind web template.

- Step 4. When you have located the form you require, select the Purchase now key. Opt for the rates prepare you prefer and add your qualifications to register on an profile.

- Step 5. Method the deal. You can use your bank card or PayPal profile to finish the deal.

- Step 6. Choose the structure in the legitimate kind and acquire it on the system.

- Step 7. Complete, revise and produce or signal the Nevada Qualified Domestic Trust Agreement.

Each and every legitimate document web template you get is your own permanently. You possess acces to every single kind you delivered electronically in your acccount. Click the My Forms portion and pick a kind to produce or acquire yet again.

Contend and acquire, and produce the Nevada Qualified Domestic Trust Agreement with US Legal Forms. There are millions of expert and condition-specific forms you can utilize for your personal business or specific needs.