Nevada Determining Self-Employed Independent Contractor Status

Description

How to fill out Determining Self-Employed Independent Contractor Status?

US Legal Forms - one of the most prominent collections of legal documents in the United States - offers a diverse selection of legal paperwork templates that you can download or print.

By utilizing the website, you can discover thousands of forms for commercial and personal purposes, organized by categories, states, or keywords. You can obtain the latest versions of documents like the Nevada Determination of Self-Employed Independent Contractor Status in moments.

If you already possess a membership, Log In and download the Nevada Determination of Self-Employed Independent Contractor Status from the US Legal Forms collection. The Download button will appear on every form you view. You have access to all previously downloaded forms in the My documents section of your account.

If you are satisfied with the form, confirm your selection by clicking the Purchase now button. Then, select the pricing plan you prefer and provide your information to register for an account.

Complete the purchase. Use a Visa or Mastercard, or a PayPal account to finalize the transaction. Choose the format and download the form to your device. Edit. Fill in, modify, and print and sign the downloaded Nevada Determination of Self-Employed Independent Contractor Status. Each template you add to your account has no expiry date and is yours indefinitely. Therefore, if you wish to download or print another copy, just go to the My documents section and click on the form you require. Access the Nevada Determination of Self-Employed Independent Contractor Status with US Legal Forms, one of the largest libraries of legal document templates. Utilize a wide variety of professional and state-specific templates that fulfill your business or personal needs and requirements.

- If you are using US Legal Forms for the first time, here are straightforward instructions to get started.

- Make sure you have selected the appropriate form for your state/region.

- Click the Review button to evaluate the form's content.

- Check the form details to ensure you have chosen the correct form.

- If the form does not meet your requirements, use the Search box at the top of the page to find one that does.

Form popularity

FAQ

Am I required to have a State Business License? Yes. Unless statutorily exempted, sole proprietors doing business in Nevada must maintain a State Business License. Sole proprietors may submit their State Business License application online at , by mail, or in-person.

Four ways to verify your income as an independent contractorIncome-verification letter. The most reliable method for proving earnings for independent contractors is a letter from a current or former employer describing your working arrangement.Contracts and agreements.Invoices.Bank statements and Pay stubs.

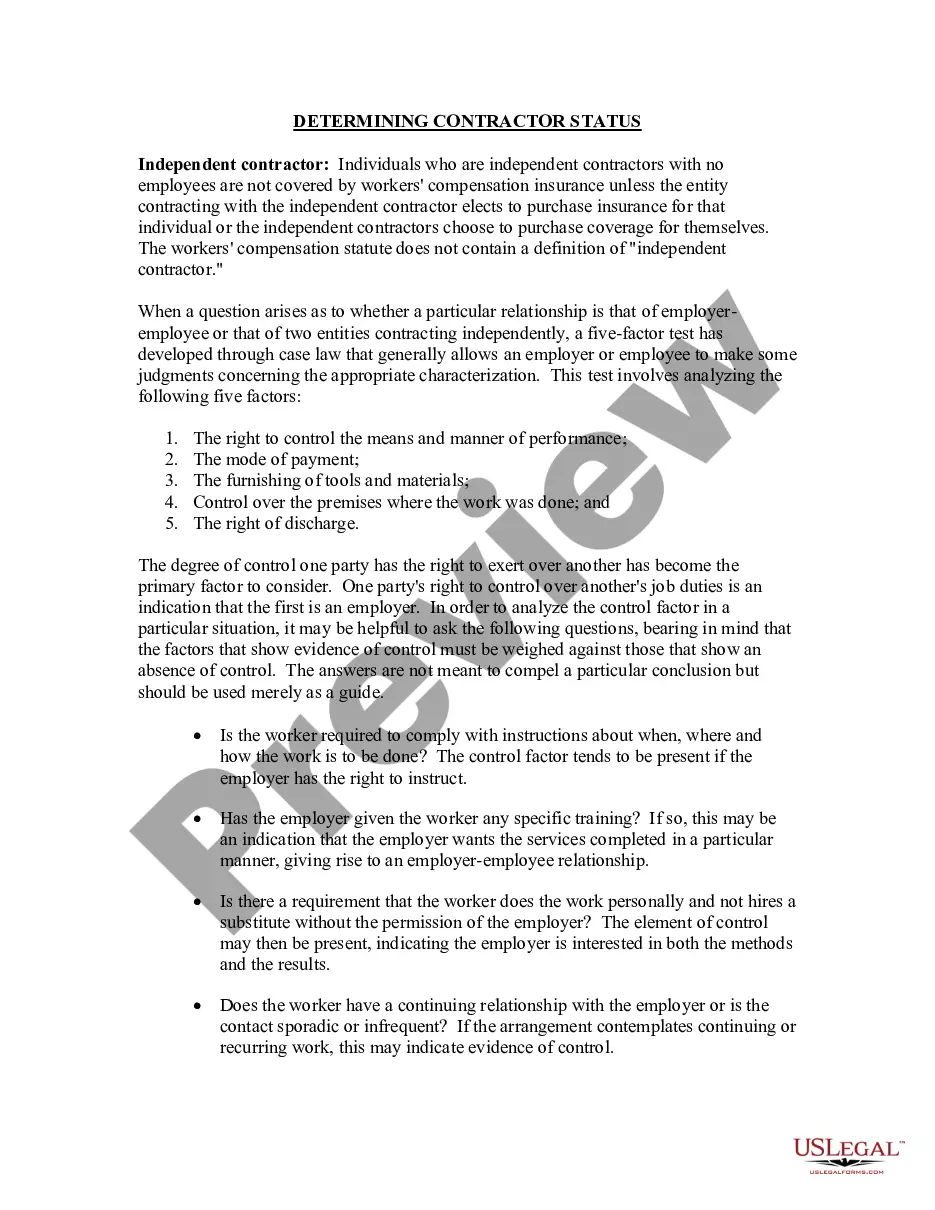

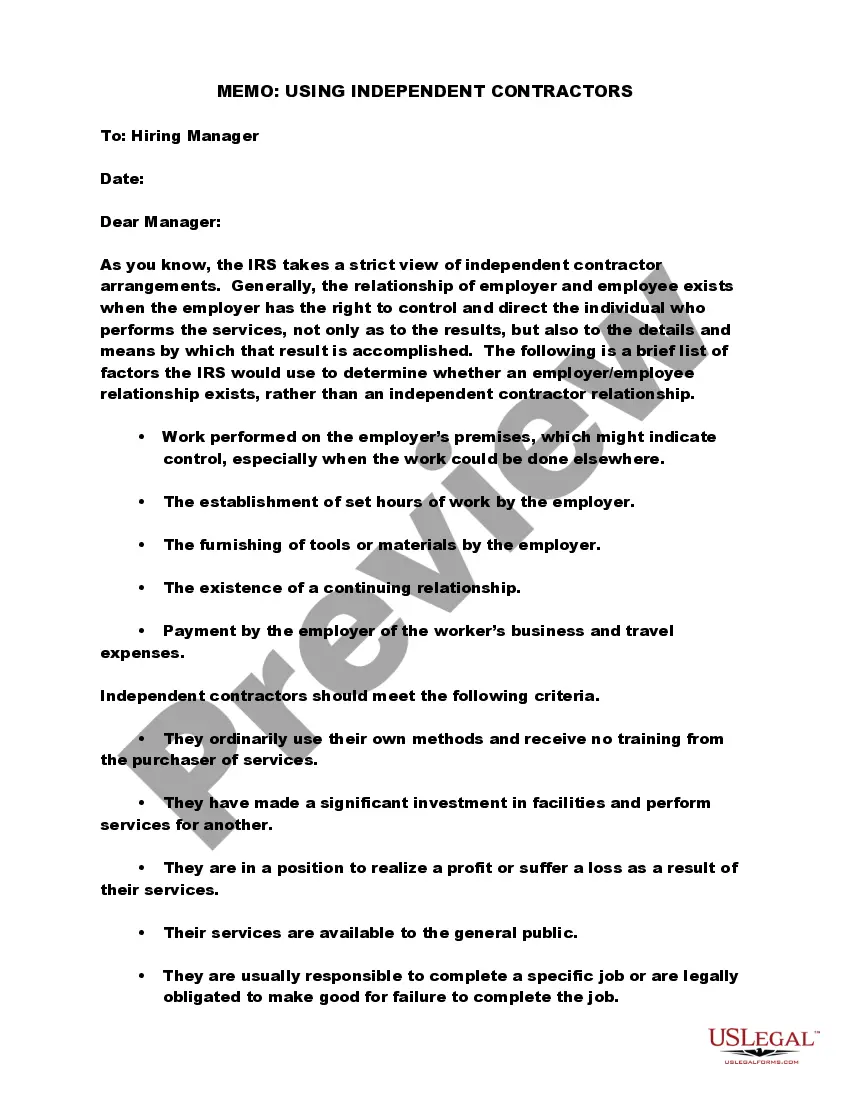

For the independent contractor, the company does not withhold taxes. Employment and labor laws also do not apply to independent contractors. To determine whether a person is an employee or an independent contractor, the company weighs factors to identify the degree of control it has in the relationship with the person.

What Is an Independent Contractor? An independent contractor is a self-employed person or entity contracted to perform work foror provide services toanother entity as a nonemployee. As a result, independent contractors must pay their own Social Security and Medicare taxes.

The general rule is that an individual is an independent contractor if the payer has the right to control or direct only the result of the work and not what will be done and how it will be done. If you are an independent contractor, then you are self-employed.

How Do I Become An Independent Contractor In Nevada? According to a 2015 state law, workers are presumed to be independent contractors instead of employees if they have insurance or an occupational license, are bonded, have a Social Security number, or have filed self-employment taxes.

Under the NIIA, an independent contractor is defined as follows: Any person who renders service for a specified recompense for a specified result, under the control of the person's principal as to the result of the person's work only and not as to the means by which such result is accomplished.

The major difference between those workers and Independent Contractors is that the contractors are actually W-2 employees, but they are employed by a staffing agency or a back-office service provider such as FoxHire instead of by the company they are performing work for.

Becoming an independent contractor is one of the many ways to be classified as self-employed. By definition, an independent contractor provides work or services on a contractual basis, whereas, self-employment is simply the act of earning money without operating within an employee-employer relationship.

These factors are: (1) the kind of occupation, with reference to whether the work usually is done under the direction of a supervisor or is done by a specialist without supervision; (2) the skill required in the particular occupation; (3) whether the employer or the individual in question furnishes the equipment used