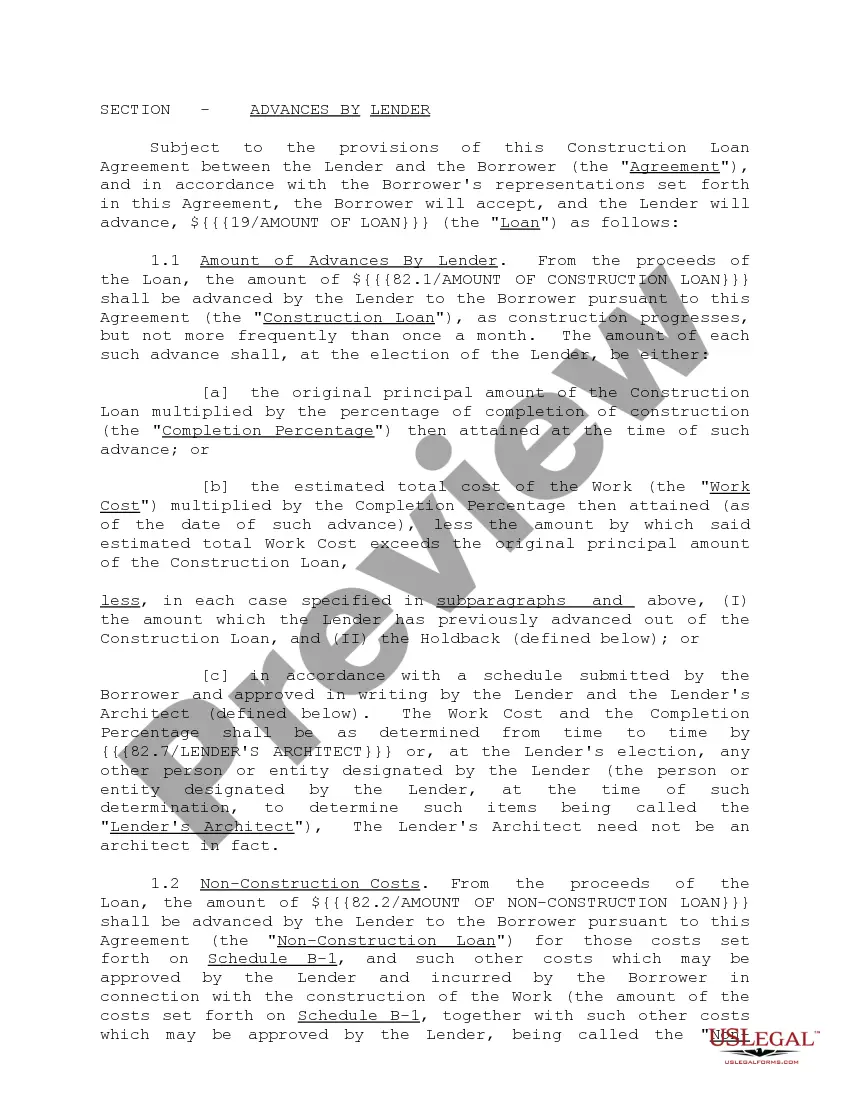

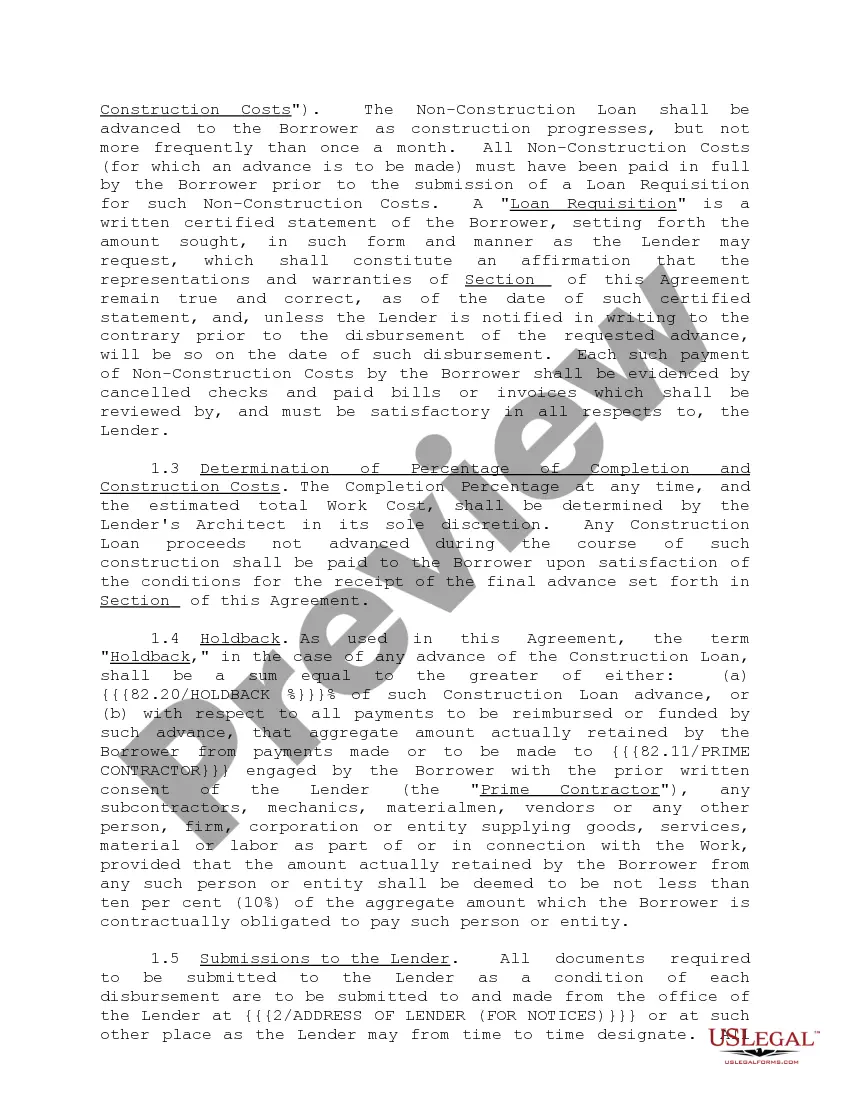

"Construction Loan Agreements and Variations" is a American Lawyer Media form. This form is to be used as a construction loan agreement.

Nevada Construction Loan Agreements and Variations refer to legally binding contracts specifically designed for individuals or companies involved in construction projects in the state of Nevada. These agreements are usually established between a lender, such as a bank or a financial institution, and a borrower who seeks funding for the construction of a property. One common type of Nevada Construction Loan Agreement is the Construction-Permanent Loan Agreement. This agreement combines both the construction loan and the permanent mortgage into a single loan process, making it more convenient for borrowers. It allows the borrower to only go through one application and approval process, eliminating the need for refinancing after construction is complete. Another variation of Nevada Construction Loan Agreements is the Single-Close Construction Loan Agreement. This agreement also combines the construction loan and the permanent financing into a single loan, but it involves only one set of closing costs, reducing the overall expenses for the borrower. Furthermore, there is the Construction-Only Loan Agreement, which focuses solely on the financing of the construction phase rather than including permanent financing. This type of agreement is suitable for borrowers who already have secure plans for permanent financing in place for their construction project. Nevada Construction Loan Agreements typically include various key terms and conditions such as loan amount, interest rate, repayment terms, loan disbursement schedule, construction milestones, draw procedures, and potential penalties for delays or defaults. These agreements also establish the responsibilities and obligations of both the borrower and the lender throughout the construction process. In order to secure a Nevada Construction Loan Agreement, borrowers are usually required to provide a detailed construction plan, cost estimations, project timelines, and other relevant documents. Lenders assess these factors to determine the viability and financial feasibility of the project. Nevada Construction Loan Agreements offer flexibility and tailored financing options to meet the unique requirements of construction projects. While the mentioned types are commonly seen in Nevada, variations might exist based on the specific needs and preferences of the borrower and lender. It is important for individuals or entities engaging in construction projects in Nevada to carefully review and negotiate the terms of the construction loan agreement to ensure a smooth and successful construction process.Nevada Construction Loan Agreements and Variations refer to legally binding contracts specifically designed for individuals or companies involved in construction projects in the state of Nevada. These agreements are usually established between a lender, such as a bank or a financial institution, and a borrower who seeks funding for the construction of a property. One common type of Nevada Construction Loan Agreement is the Construction-Permanent Loan Agreement. This agreement combines both the construction loan and the permanent mortgage into a single loan process, making it more convenient for borrowers. It allows the borrower to only go through one application and approval process, eliminating the need for refinancing after construction is complete. Another variation of Nevada Construction Loan Agreements is the Single-Close Construction Loan Agreement. This agreement also combines the construction loan and the permanent financing into a single loan, but it involves only one set of closing costs, reducing the overall expenses for the borrower. Furthermore, there is the Construction-Only Loan Agreement, which focuses solely on the financing of the construction phase rather than including permanent financing. This type of agreement is suitable for borrowers who already have secure plans for permanent financing in place for their construction project. Nevada Construction Loan Agreements typically include various key terms and conditions such as loan amount, interest rate, repayment terms, loan disbursement schedule, construction milestones, draw procedures, and potential penalties for delays or defaults. These agreements also establish the responsibilities and obligations of both the borrower and the lender throughout the construction process. In order to secure a Nevada Construction Loan Agreement, borrowers are usually required to provide a detailed construction plan, cost estimations, project timelines, and other relevant documents. Lenders assess these factors to determine the viability and financial feasibility of the project. Nevada Construction Loan Agreements offer flexibility and tailored financing options to meet the unique requirements of construction projects. While the mentioned types are commonly seen in Nevada, variations might exist based on the specific needs and preferences of the borrower and lender. It is important for individuals or entities engaging in construction projects in Nevada to carefully review and negotiate the terms of the construction loan agreement to ensure a smooth and successful construction process.