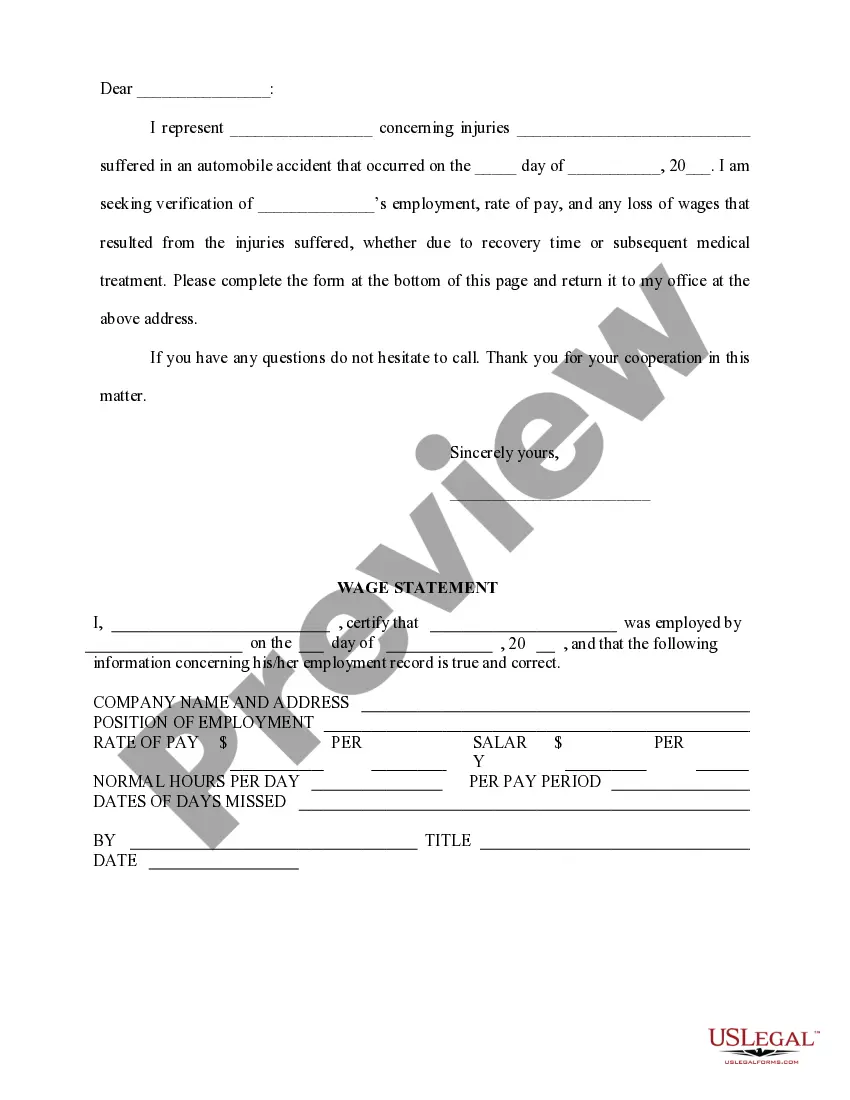

This form is intended to assist the attorney in case preparation by providing the client with a form to be used in documenting all expenses and lost wages associated with the client's claim.

Nevada Wage and Income Loss Statement

State:

Multi-State

Control #:

US-PI-0009

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Wage And Income Loss Statement?

US Legal Forms - among the biggest libraries of legal varieties in America - gives a variety of legal file templates you may obtain or printing. While using website, you can get a huge number of varieties for business and personal purposes, categorized by types, suggests, or keywords.You can find the newest variations of varieties such as the Nevada Wage and Income Loss Statement within minutes.

If you already possess a subscription, log in and obtain Nevada Wage and Income Loss Statement in the US Legal Forms catalogue. The Acquire key can look on each and every develop you perspective. You get access to all formerly saved varieties within the My Forms tab of the profile.

If you would like use US Legal Forms the very first time, allow me to share basic recommendations to obtain started off:

- Make sure you have selected the right develop to your area/region. Go through the Preview key to analyze the form`s content material. Browse the develop description to ensure that you have chosen the proper develop.

- In the event the develop does not match your needs, make use of the Look for area at the top of the screen to discover the one which does.

- In case you are satisfied with the shape, validate your decision by clicking on the Buy now key. Then, pick the prices prepare you favor and offer your accreditations to sign up for an profile.

- Approach the transaction. Utilize your Visa or Mastercard or PayPal profile to finish the transaction.

- Choose the file format and obtain the shape in your device.

- Make alterations. Fill out, edit and printing and signal the saved Nevada Wage and Income Loss Statement.

Each template you added to your money does not have an expiry particular date and it is yours for a long time. So, if you would like obtain or printing another copy, just proceed to the My Forms portion and then click around the develop you require.

Obtain access to the Nevada Wage and Income Loss Statement with US Legal Forms, by far the most extensive catalogue of legal file templates. Use a huge number of professional and state-particular templates that meet up with your business or personal demands and needs.

Form popularity

FAQ

Instead, employers are required to provide reasonable accommodations for the disability. Nevada law also prohibits employers from firing employees solely because they have filed a workers' compensation claim. Offering light duty is one way to comply with these rules.

Unless excluded by statute, it is mandatory for an employer who has one or more employees to provide workers' compensation insurance coverage. Some employees are excluded by NRS 616A. 110 due to unique criteria.

First, ask the employer for what you are owed. Then, if you do not receive payment, you may file a complaint with the Office of the Labor Commissioner in Las Vegas or Carson City. For a copy of the wage claim form, click here.

When an employee is discharged in Nevada, the law say that their employer must pay the full final paycheck immediately. This must include all unpaid wages and compensation that the employee has earned. Employers have a three day period after an employee is discharged before they will be penalized for late payment.

Workers' Compensation Benefits May Include The Following: Coverage of Medical Treatment; Compensation for Lost Wages (TTD); Permanent Partial Disability (PPD); Permanent Total Disability (PTD);

6 Injured Employee's Request for Compensation (7/99)

Money an injured worker receives when he or she is no longer able to work at all due to the work-related injury. This amount is usually paid to the injured worker for the remainder of their life. Nevada allows an injured worker to reopen their workers' compensation claim at any point, for life.

Filing A Workers' Compensation Claim The C-4 form is titled ?Employee's Claim for Compensation/Report of Initial Treatment?. The physician fills out their part of the form, and sends a copy to your employer and the insurer. Be sure to get a copy for your records.